Westjet 2009 Annual Report Download - page 84

Download and view the complete annual report

Please find page 84 of the 2009 Westjet annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

|

|

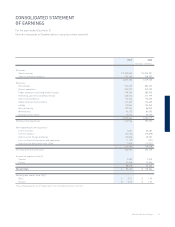

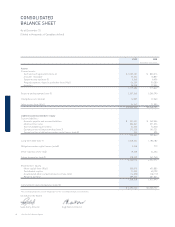

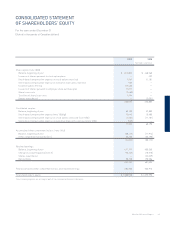

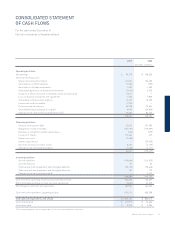

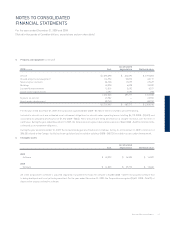

54 WestJet 2009 Annual Report

NOTES TO CONSOLIDATED

FINANCIAL STATEMENTS

For the years ended December 31, 2009 and 2008

(Stated in thousands of Canadian dollars, except share and per share data)

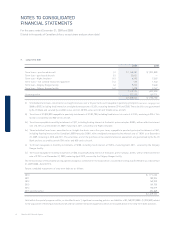

1. Summary of signifi cant accounting policies (continued)

(f) Financial instruments (continued)

The Corporation will, from time to time, use various fi nancial derivatives to reduce market risk exposure from changes in foreign exchange

rates and jet fuel prices. Derivatives, including embedded derivatives, are recorded at fair value on the balance sheet with changes in fair value

recorded in the statement of earnings unless exempted from derivative treatments as a normal purchase and sale or are clearly and closely

related embedded derivatives or as designated effective hedging instruments. The Corporation selected January 1, 2003, as its transition date for

embedded derivatives; as such only contracts entered into or substantively modifi ed after the transition date have been examined for embedded

derivatives. When fi nancial assets and liabilities are designated as part of a hedging relationship and qualify for hedge accounting, they are subject

to measurement and classifi cation requirements outlined under cash fl ow hedges. The Corporation’s policy is not to utilize derivative fi nancial

instruments for trading or speculative purposes.

The Corporation will assess at each reporting period, whether there is any objective evidence that a fi nancial asset, other than those classifi ed

as held-for-trading, is impaired.

The Corporation immediately expenses any transaction costs incurred in relation to the acquisition of fi nancial assets and liabilities.

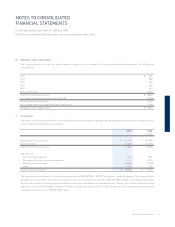

(g) Cash fl ow hedges

The Corporation uses various fi nancial derivative instruments such as forward contracts, fi xed swap agreements, costless collar structures and

option arrangements to manage fl uctuations in foreign exchange rates and jet fuel prices.

The Corporation’s derivatives that have been designated and qualify for hedge accounting are classifi ed as cash fl ow hedges. The Corporation

formally documents all relationships between hedging instruments and hedged items, as well as the risk-management objective and strategy

for undertaking the hedge transaction. This process includes linking all derivatives that are designated in a cash fl ow hedging relationship to

a specifi c fi rm commitment or forecasted transaction. The Corporation also formally assesses, both at inception and at every reporting date,

whether the derivatives that are used in hedging transactions have been highly effective in offsetting changes in cash fl ows of hedged items and

whether those derivatives may be expected to remain highly effective in future periods.

Under cash fl ow hedge accounting, the effective portion of the change in the fair value of the hedging instrument is recognized in OCI while the

ineffective portion is recognized in non-operating income (expense). Upon maturity of the fi nancial derivative instrument, the effective gains and

losses previously recognized in accumulated other comprehensive loss (AOCL) are recorded in net earnings under the same caption as the hedged

item.

If the hedging relationship ceases to qualify for cash fl ow hedge accounting, any change in fair value of the instrument from the point it ceases to

qualify is recorded in non-operating income (expense). Amounts previously recorded in AOCL will remain in AOCL until the anticipated transaction

occurs, at which time, the amount is recorded in net earnings under the same caption as the hedged item. If the transaction is no longer expected

to occur, amounts previously recorded in AOCL will be reclassifi ed to non-operating income (expense).

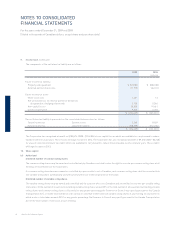

(h) Foreign currency

Monetary assets and liabilities, denominated in foreign currencies, are translated into Canadian dollars at the rate of exchange in effect at the

balance sheet date, with any resulting gain or loss being included in the consolidated statement of earnings. Non monetary assets, non-monetary

liabilities and revenues and expenses arising from transactions denominated in foreign currencies are translated into Canadian dollars at the

rates prevailing at the time of the transaction.

(i) Cash and cash equivalents

Cash and cash equivalents consist of cash and short-term investments that are highly liquid in nature and have a maturity date of one year

or less.