Westjet 2009 Annual Report Download - page 45

Download and view the complete annual report

Please find page 45 of the 2009 Westjet annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

|

|

WestJet 2009 Annual Report 15

establishes maximum hedging limits based on time horizon;

however, it does not include a minimum hedging requirement.

Management continuously reviews and adjusts its strategy based

on market conditions and competitors’ positions. During the year

ended December 31, 2009, we did not enter into any new fuel

derivatives. Jet fuel is not traded on an organized North American

futures exchange, and there are limited opportunities to hedge

directly in jet fuel through the over-the-counter market. However,

fi nancial derivatives in other crude-oil-based commodities that

are traded directly on organized exchanges, such as crude oil

and heating oil, are also useful in decreasing the risk of volatile

fuel prices.

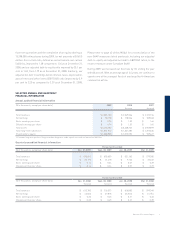

As at December 31, 2009, we had a mixture of fixed swap

agreements and costless collar structures in Canadian-dollar

WTI crude oil derivative contracts to hedge approximately 14 per

cent (December 31, 2008 – 14 per cent) of our anticipated jet

fuel requirements for 2010. The following table outlines, as at

December 31, 2009, the notional volumes per barrel (bbl.) and

the weighted average strike price for fi xed swap agreements,

and the weighted average call and put prices for costless

collar structures.

of effectiveness; accordingly, changes in time value are

recognized in non-operating income (expense) during the period

the change occurs. As a result, a signifi cant portion of the change

in fair value of our options may be recorded as ineffective.

Ineffectiveness is inherent in hedging jet fuel with derivative

instruments in other commodities, such as crude oil, particularly

given the signifi cant volatility observed in the market on crude

oil and related products. Due to this volatility, we are unable to

predict the amount of ineffectiveness for each period. This may

result in increased volatility in our results.

If the hedging relationship ceases to qualify for cash fl ow hedge

accounting, any change in fair value of the instrument from the

point it ceases to qualify is recorded in non-operating income

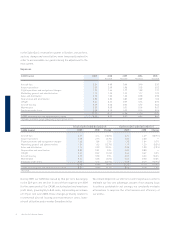

Aircraft fuel

During the year ended December 31, 2009, we experienced

substantial relief from the elevated fuel prices that negatively

impacted our CASM during the same period in 2008. The average

market price for jet fuel was US $81 per barrel in 2009 versus US

$134 per barrel in 2008, representing a decline of 39.6 per cent.

We saw a corresponding decrease in our fuel costs per ASM of

30.9 per cent to 3.24 cents in 2009, as compared to 4.69 cents

in 2008. These favourable changes resulted from reductions in

both US-dollar WTI crude oil prices and refi ning costs. This was

offset partially by the devaluation of the Canadian dollar versus

the US dollar, incremental costs incurred to transport fuel into

the Prairie provinces and the impact of realized losses on the

settlement of fuel-derivative contracts. Although market prices

have subsided from their previous levels, fuel remains our most

signifi cant cost, representing approximately 28 per cent of total

operating costs for the year ended December 31, 2009, down

from approximately 36 per cent for 2008.

Under our fuel price risk management policy, we are permitted to

hedge a portion of our future anticipated jet fuel purchases for up

to 36 months, as approved by our Board of Directors. The policy

Upon proper qualifi cation, we account for our fuel derivatives

as cash fl ow hedges. Under cash fl ow hedge accounting, the

effective portion of the change in the fair value of the hedging

instrument is recognized in accumulated other comprehensive

loss (AOCL), while the ineffective portion is recognized in non-

operating income (expense). Upon maturity of the derivative

instrument, the effective gains and losses previously recognized

in AOCL are recorded in net earnings as a component of aircraft

fuel expense.

Our policy for our fuel derivatives is to measure effectiveness

based on the change in the intrinsic value of the fuel derivatives

versus the change in the intrinsic value of the anticipated jet fuel

purchase. We elect to exclude time value from the measurement

Year Instrument

Notional volumes

(bbl.)

WTI average strike

price (CAD$/bbl.)

WTI average call

price (CAD$/bbl.)

WTI average put

price (CAD$/bbl.)

2010 Swaps 381,000 103.09 — —

Costless collars 483,000 — 111.21 77.94