Foot Locker 2006 Annual Report Download - page 31

Download and view the complete annual report

Please find page 31 of the 2006 Foot Locker annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

|

|

15

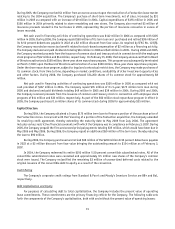

During 2005, the Company received $1 million from an escrow account upon the resolution of a Footaction lease matter

relating to the 2004 acquisition. The Company’s purchase of short-term investments, net of sales, increased by $31

million in 2005 as compared with an increase of $9 million in 2004. Capital expenditures of $155 million in 2005 and

$156 million in 2004 primarily related to store remodeling and new stores. The Company also received $3 million of

insurance proceeds related to the hurricanes in 2005, representing the portion of insurance recoveries in excess of

losses recorded.

Net cash used in financing activities of continuing operations was $142 million in 2006 as compared with $105

million in 2005. During 2006, the Company repaid $50 million of its term loan and purchased and retired $38 million of

its 8.50 percent debentures payable in 2022 at a $2 million discount from face value. As required by SFAS No. 123(R),

the Company recorded an excess tax benefit related to stock-based compensation of $2 million as a financing activity.

The Company declared and paid dividends totaling $61 million in 2006 and $49 million in 2005. During 2006 and 2005,

the Company received proceeds from the issuance of common stock and treasury stock in connection with the employee

stock programs of $12 million and $14 million, respectively. On February 15, 2006, the Company announced that its Board

of Directors authorized a $150 million, three-year share repurchase program. This program was subsequently terminated

on March 7, 2007, upon the Board of Directors authorization of a new $300 million, three-year share repurchase program.

Under the share repurchase program, subject to legal and contractual restrictions, the Company may make purchases of

its common stock, from time to time, depending on market conditions, availability of other investment opportunities

and other factors. During 2006, the Company purchased 334,200 shares of its common stock for approximately $8

million.

Net cash used in financing activities of continuing operations was $105 million in 2005 as compared with net

cash provided of $167 million in 2004. The Company repaid $35 million of its 5-year, $175 million term loan during

2005 and declared and paid dividends totaling $49 million in 2005 and $39 million in 2004. During 2005 and 2004,

the Company received proceeds from the issuance of common and treasury stock in connection with employee stock

programs of $14 million and $33 million, respectively. As part of the $50 million stock repurchase program in effect in

2005, the Company purchased 1.6 million shares of its common stock during 2005 for approximately $35 million.

Capital Structure

During 2004, the Company obtained a 5-year, $175 million term loan to finance a portion of the purchase price of

the Footaction stores. Concurrent with the financing of a portion of the Footaction acquisition, the Company amended

its revolving credit agreement, thereby extending the maturity date to May 2009 from July 2006. The agreement

includes various restrictive financial covenants with which the Company was in compliance on February 3, 2007. During

2005, the Company prepaid the first and second principal payments totaling $35 million, which would have been due in

May 2005 and May 2006. During 2006, the Company repaid an additional $50 million of the term loan, thereby reducing

the loan to $90 million.

During 2006, the Company purchased and retired $38 million of the $200 million 8.50 percent debentures payable

in 2022 at a $2 million discount from face value bringing the outstanding amount to $134 million as of February 3,

2007.

In 2004, the Company redeemed its entire $150 million 5.50 percent convertible subordinated notes. All of the

convertible subordinated notes were cancelled and approximately 9.5 million new shares of the Company’s common

stock were issued. The Company reclassified the remaining $3 million of unamortized deferred costs related to the

original issuance of the convertible debt to equity as a result of the conversion.

Credit Rating

The Company’s corporate credit ratings from Standard & Poor’s and Moody’s Investors Service are BB+ and Ba1,

respectively.

Debt Capitalization and Equity

For purposes of calculating debt to total capitalization, the Company includes the present value of operating

lease commitments. These commitments are the primary financing vehicle for the Company. The following table sets

forth the components of the Company’s capitalization, both with and without the present value of operating leases: