Experian 2015 Annual Report Download - page 79

Download and view the complete annual report

Please find page 79 of the 2015 Experian annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

|

|

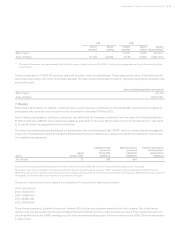

Policy on the provision of non-audit services

This policy has not changed during the year and remains appropriate for the Group. Provided that the provision of non-audit

services does not conflict with the external auditor’s statutory responsibilities and ethical guidance, they may provide the

following types of services:

Further assurance services: where the external auditor’s deep knowledge of the Group’s affairs means that they may be best placed

to carry out such work. This may include, but is not restricted to, shareholder and other circulars, regulatory reports and work in

connection with acquisitions and divestments.

Tax services: where the external auditor’s knowledge of the Group’s affairs may provide significant advantages, which other parties

would not have. Where this is not the case, the work is put out to tender.

General: in other circumstances, the external auditor may provide services provided that proposed assignments are put out to tender

and decisions to award work are taken on the basis of demonstrable competence and cost effectiveness. However, the external

auditor is specifically prohibited from performing work related to accounting records and financial statements that will ultimately be

subject to external audit; management of or significant involvement in internal audit services; any work that could compromise the

external auditor’s independence; and any other work that is prohibited by UK ethical guidance.

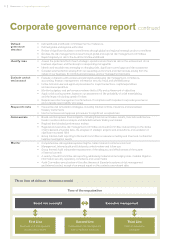

‘Fair, balanced and understandable’ – what did we do?

At its May meeting, the Committee is asked to consider, in

line with the UK Corporate Governance Code, whether, in its

opinion, the Annual Report is fair, balanced and understandable

(‘FBU’) and whether it provides the information necessary for

shareholders to assess the Group’s performance, business

model and strategy. A process to support the Audit Committee

in making this assessment was put in place in 2013, and we also

use a similar process for the Group’s half-yearly financial report.

The main elements of the process are:

• The Audit Committee was appraised of the new requirement,

introduced by the FRC in 2012, and the Board confirmed that

it required advice annually from the Committee on making the

required statement. The Committee’s terms of reference were

amended to reflect its new responsibility.

• The management team responsible for drafting the Annual

Report is briefed on the requirement, including by the

external auditor.

• A list of key ‘areas to focus on’ (see below) is circulated to the

management team, who are asked to consider these areas in

their drafting.

• Ahead of its March meeting, the Audit Committee receives:

drafts of a large number of the Strategic report components of

the Annual Report; draft governance material; a summary of the

key features of the Group financial statements; papers on the

appropriateness of accounting policies and impairment reviews;

and a paper from the external auditor.

• An internal FBU committee then considers the Annual Report.

A wide range of functions are represented on this committee,

including executives from finance, communications, investor

relations, legal and corporate secretariat. The external auditor

also supports the committee.

• In advance of its May meeting, the Audit Committee receives a

near-final draft of the Annual Report, together with a reminder

of the ‘areas to focus on’. The FBU committee’s observations

and conclusions are also relayed to the Committee.

• Following its review this year, the Audit Committee

concluded that it was appropriate to recommend to the

Board that the Annual Report 2015 was fair, balanced and

understandable, and provided the information necessary for

shareholders to assess the Group’s performance, business

model and strategy, and the FBU statement appears in the

Directors’ report.

The key areas to focus on include ensuring that:

• The overall message of the narrative reporting is consistent

with the primary financial statements.

• The overall message of the narrative reporting is appropriate,

in the context of the industry as a whole and the wider

economic environment.

• The Annual Report is consistent with messages already

communicated to investors, analysts and other stakeholders.

• The Annual Report ‘taken as a whole’ is fair, balanced

and understandable.

• The Chairman and Chief Executive Officer’s statements

include a balanced view of the Group’s performance and

prospects, and of the industry and market as a whole.

• Any summaries or highlights capture the big picture of the

Group appropriately.

• Case studies or examples are of strategic importance and

do not over-emphasise immaterial matters.

77

Governance •Corporate governance report