Dollar General 2004 Annual Report Download - page 30

Download and view the complete annual report

Please find page 30 of the 2004 Dollar General annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

|

|

28

Quantitative and Qualitative Disclosures About Market Risk

Financial Risk Management

The Company is exposed to market risk primarily from

adverse changes in interest rates. To minimize such risk,

the Company may periodically use financial instruments,

including derivatives. As a matter of policy, the Company

does not buy or sell financial instruments for speculative

or trading purposes and all financial instrument transac-

tions must be authorized and executed pursuant to

approval by the Board of Directors. All financial instrument

positions taken by the Company are used to reduce risk

by hedging an underlying economic exposure. Because

of high correlation between the financial instrument and

the underlying exposure being hedged, fluctuations in the

value of the financial instruments are generally offset by

reciprocal changes in the value of the underlying economic

exposure. The financial instruments used by the Company

are straightforward instruments with liquid markets.

The Company has cash flow exposure relating to variable

interest rates associated with its revolving line of credit,

and may periodically seek to manage this risk through the

use of interest rate derivatives. The primary interest rate

exposure on variable rate obligations is based on the

London Interbank Offered Rate (“LIBOR”).

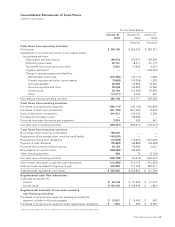

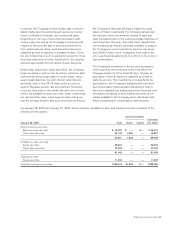

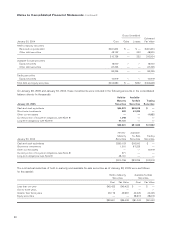

At January 28, 2005 and January 30, 2004, the fair value

of the Company’s debt, excluding capital lease obligations,

was approximately $278.7 million and $265.4 million,

respectively (net of the fair value of a note receivable on

the South Boston, Virginia DC of approximately $50.0 mil-

lion and $48.9 million, respectively, as further discussed in

Note 8 to the Consolidated Financial Statements), based

upon the estimated market value of the debt at those

dates. Such fair value exceeded the carrying values of

the debt at January 28, 2005 and January 30, 2004 by

approximately $35.5 million and $21.7 million, respectively.

At February 1, 2002, the Company was party to an

interest rate swap agreement with a notional amount of

$100 million. The Company designated this agreement

as a hedge of its floating rate commitments relating to a

portion of certain synthetic lease agreements that existed

at that time. Under the terms of the agreement, the

Company paid a fixed rate of 5.60% and received a

floating rate (LIBOR) on the $100 million notional amount

through September 1, 2002. The fair value of the interest

rate swap agreement was $(2.6) million at February 1,

2002. The counterparty to the Company’s interest rate

swap agreement was a major financial institution. The

interest rate swap agreement expired on September 1,

2002. As of January 28, 2005, the Company was not

party to any interest rate derivatives.

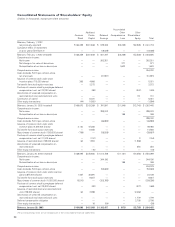

In 2002, as required by SFAS No. 133, the Company

recorded the fair value of the interest rate swap in the

balance sheet, with the offsetting, effective portion of

the change in fair value recorded in Other comprehensive

loss, a separate component of Shareholders’ equity in

the Consolidated Financial Statements. Amounts

recorded in Other comprehensive loss were reclassified

into earnings, as an adjustment to interest expense, in

the same period during which the hedged synthetic

lease agreements affected earnings.

Based upon the Company’s variable rate borrowing

levels, a 1% adverse change in interest rates would have

resulted in a pre-tax reduction of earnings and cash flows

of less than $0.1 million and approximately $1.7 million in

2004 and 2002, respectively, including the effects of

interest rate swaps in 2002. In 2003, the Company had

no outstanding variable rate borrowings. Based upon the

Company’s outstanding indebtedness at January 28,

2005 and January 30, 2004, a 1% reduction in interest

rates would have resulted in an increase in the fair value

of the Company’s fixed rate debt of approximately $10.5

million and $14.8 million, respectively.