Dollar General 2004 Annual Report Download - page 24

Download and view the complete annual report

Please find page 24 of the 2004 Dollar General annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

|

|

22

Management’s Discussion and Analysis of Financial Condition

and Results of Operations (continued)

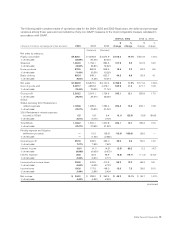

proceeds from the exercise of stock options during

2004 and 2003 of $34.1 million and $49.5 million,

respectively. The use of cash in 2002 primarily reflects

the net repayment of $397.1 million in outstanding debt

and the payment of $42.6 million of cash dividends.

The net repayment of debt in 2002 was undertaken to

strengthen the Company’s financial position and was

accomplished by utilizing cash flow from operations

and existing cash balances.

Critical Accounting Policies and Estimates

The preparation of financial statements in accordance

with GAAP requires management to make estimates and

assumptions that affect reported amounts and related dis-

closures. Management considers an accounting estimate

to be critical if:

■ it requires assumptions to be made that were uncertain

at the time the estimate was made; and

■ changes in the estimate or different estimates that

could have been selected could have a material effect

on the Company’s results of operations or financial

condition.

Management has discussed the development and selec-

tion of its critical accounting estimates with the Audit

Committee of the Company’s Board of Directors and the

Audit Committee has reviewed the disclosures presented

below relating to them.

In addition to the estimates presented below, there are

other items within the Company’s financial statements

that require estimation, but are not deemed critical as

defined above. The Company believes these estimates

are reasonable and appropriate. However, if actual expe-

rience differs from the assumptions and other consider-

ations used, the resulting changes could have a material

effect on the financial statements taken as a whole.

Merchandise Inventories. Merchandise inventories

are stated at the lower of cost or market with cost deter-

mined using the retail last-in, first-out (“LIFO”) method.

Under the Company’s retail inventory method (“RIM”),

the calculation of gross profit and the resulting valuation

of inventories at cost are computed by applying a calcu-

lated cost-to-retail inventory ratio to the retail value of

sales. The RIM is an averaging method that has been

widely used in the retail industry due to its practicality.

Also, it is recognized that the use of the RIM will result in

valuing inventories at the lower of cost or market if mark-

downs are currently taken as a reduction of the retail

value of inventories.

Inherent in the RIM calculation are certain significant

management judgments and estimates including, among

others, initial markups, markdowns, and shrinkage, which

significantly impact the gross profit calculation as well as

the ending inventory valuation at cost. These significant

estimates, coupled with the fact that the RIM is an aver-

aging process, can, under certain circumstances, produce

distorted cost figures. Factors that can lead to distortion

in the calculation of the inventory balance include:

■ applying the RIM to a group of products that is not

fairly uniform in terms of its cost and selling price

relationship and turnover;

■ applying the RIM to transactions over a period of time

that include different rates of gross profit, such as

those relating to seasonal merchandise;

■ inaccurate estimates of inventory shrinkage between

the date of the last physical inventory at a store and

the financial statement date; and

■ inaccurate estimates of lower of cost or market

(“LCM”) and/or LIFO reserves.

To reduce the potential of such distortions in the valua-

tion of inventory, the Company’s RIM calculation through

the end of 2004 utilized 10 departments in which fairly

homogenous classes of merchandise inventories having

similar gross margins were grouped. In 2005, in order to

further refine its RIM calculation, the Company expanded

the number of departments it utilizes for its gross margin

calculation from 10 to 23. The impact of this change on

the Company’s future consolidated financial statements

is not currently expected to be material to a given fiscal

year, although a given quarter could be impacted based

on the mix of sales in the quarter. Other factors that

reduce potential distortion include the use of historical

experience in estimating the shrink provision (see discus-

sion below) and the utilization of an independent statisti-

cian to assist in the LIFO sampling process and index

formulation. Also, on an ongoing basis, the Company

reviews and evaluates the salability of its inventory and

records LCM reserves, if necessary.

The Company calculates its shrink provision based on

actual physical inventory results during the fiscal period

and an accrual for estimated shrink occurring subsequent

to a physical inventory through the end of the fiscal report-

ing period. This accrual is calculated as a percentage of

sales and is determined by dividing the book-to-physical

inventory adjustments recorded during the previous twelve

months by the related sales for the same period for

each store. Beginning in 2003, in an effort to improve