Chevron 2011 Annual Report Download - page 83

Download and view the complete annual report

Please find page 83 of the 2011 Chevron annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92

|

|

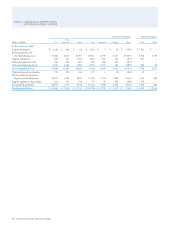

Table V Reserve Quantity Information – Continued

Net Proved Reserves of Natural Gas

Total

Consolidated Companies

Aliated Companies Consolidated

Other

and Aliated

Billions of cubic feet (BCF) U.S. Americas1 Africa Asia Australia Europe Total TCO Other2 Companies

Reserves at January 1, 2009 3,150 2,368 3,056 7,996 1,962 490 19,022 3,175 878 23,075

Changes attributable to:

Revisions 39 (126) 4 493 166 (7) 569 (237) 193 525

Improved recovery – – – – – – – – – –

Extensions and discoveries 53 1 3 54 4,276 – 4,387 – – 4,387

Purchases – – – – – – – – – –

Sales (33) (84) – – – – (117) – – (117)

Production3 (511) (174) (42) (683) (159) (139) (1,708) (105) (8) (1,821)

Reserves at December 31, 20094 2,698 1,985 3,021 7,860 6,245 344 22,153 2,833 1,063 26,049

Changes attributable to:

Revisions 220 4 (20) (31) (22) 46 197 (324) 56 (71)

Improved recovery 1 1 – – – – 2 – – 2

Extensions and discoveries 36 4 – 59 – 11 110 – – 110

Purchases 3 – – 4 – – 7 – – 7

Sales (7) – – – – – (7) – – (7)

Production3 (479) (179) (57) (699) (167) (126) (1,707) (123) (9) (1,839)

Reserves at December 31, 20104 2,472 1,815 2,944 7,193 6,056 275 20,755 2,386 1,110 24,251

Changes attributable to:

Revisions 217 (4) 39 196 (107) 74 415 (21) 103 497

Improved recovery – 1 – – – – 1 – – 1

Extensions and discoveries 287 13 290 46 4,035 9 4,680 – – 4,680

Purchases 1,231 – – 2 – – 1,233 – – 1,233

Sales (95) – – (2) (77) – (174) – – (174)

Production3 (466) (161) (77) (714) (163) (100) (1,681) (114) (10) (1,805)

Reserves at December 31, 20114 3,646 1,664 3,196 6,721 9,744 258 25,229 2,251 1,203 28,683

1 Ending reserve balances in North America and South America were 19, 21, 23 and 1,645, 1,794, 1,962 in 2011, 2010 and 2009, respectively.

2 Ending reserve balances in Africa and South America were 1,016, 953, 898 and 187, 157, 165 in 2011, 2010 and 2009, respectively.

3 Total “as sold” volumes are 4.4 BCF, 4.5 BCF and 4.5 BCF for 2011, 2010 and 2009, respectively.

4 Includes reserve quantities related to production-sharing contracts (PSC) (refer to page 8 for the denition of a PSC). PSC-related reserve quantities are 21 percent,

29 percent and 31 percent for consolidated companies for 2011, 2010 and 2009, respectively.

Noteworthy amounts in the categories of natural gas

proved-reserve changes for 2009 through 2011 are dis-

cussed below:

Revisions In 2009, net revisions increased reserves

569 BCF for consolidated companies and decreased reserves

44 BCF for aliated companies. For consolidated companies,

net increases were 493 BCF in Asia, primarily as a result of

reservoir studies in Bangladesh and development drilling in

ailand. ese results were partially oset by a downward

revision due to the impact of higher prices on production-

sharing contracts in Myanmar. In Australia, the 166 BCF

increase in reserves resulted from improved reservoir per-

formance and compression. In Other Americas, reserves

decreased 126 BCF, driven primarily by the eect of higher

prices on production-sharing contracts in Trinidad and

Tobago. In the United States, a net increase of 39 BCF was

the result of development drilling in the Gulf of Mexico,

partially oset by performance revisions in the California

and mid-continent areas.

For equity aliates, a downward revision of 237 BCF at

TCO was due to the eect of higher prices on royalty determi-

nation and an increase in gas injection for SGI/SGP facilities.

is decline was partially oset by performance and drilling

opportunities related to the Angola LNG project.

In 2010, net revisions increased reserves by 197 BCF for

consolidated companies, which was more than oset by a

268 BCF decrease in net revisions for aliated companies. For

consolidated companies, a net increase in the United States of

220 BCF, primarily in the mid-continent area and the Gulf of

Mexico, was the result of a number of small upward revisions

related to improved reservoir performance and drilling activ-

ity, none of which were individually signicant. e increase

was partially oset by downward revisions due to the impact

of higher prices on production-sharing contracts in Asia. For

equity aliates, a downward revision of 324 BCF at TCO was

due to the price eect on royalty determination and a change in

the variable-royalty calculation. is decline was partially oset

by the recognition of additional reserves related to the Angola

LNGproject.

Chevron Corporation 2011 Annual Report 81