Chevron 2011 Annual Report Download - page 13

Download and view the complete annual report

Please find page 13 of the 2011 Chevron annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

|

|

Chevron Corporation 2011 Annual Report 11

may be caused by military conicts, civil unrest or politi-

cal uncertainty. Any of these factors could also inhibit the

company’s production capacity in an aected region. e

company monitors developments closely in the countries in

which it operates and holds investments, and seeks to manage

risks in operating its facilities and businesses. e longer-term

trend in earnings for the upstream segment is also a func-

tion of other factors, including the company’s ability to nd

or acquire and eciently produce crude oil and natural gas,

changes in scal terms of contracts, and changes in tax laws

and regulations.

e company continues to actively manage its schedule

of work, contracting, procurement and supply-chain activities

to eectively manage costs. However, price levels for capital

and exploratory costs and operating expenses associated with

the production of crude oil and natural gas can be subject

to external factors beyond the company’s control. External

factors include not only the general level of ination, but

also commodity prices and prices charged by the industry’s

material and service providers, which can be aected by the

volatility of the industry’s own supply-and-demand condi-

tions for such materials and services. Capital and exploratory

expenditures and operating expenses can also be aected by

damage to production facilities caused by severe weather or

civil unrest.

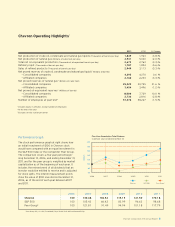

e chart above shows the trend in benchmark prices

for West Texas Intermediate (WTI) crude oil, Brent crude

oil and U.S. Henry Hub natural gas. e WTI price aver-

aged $95 per barrel for the full-year 2011, compared to $79

in 2010. As of mid-February 2012, the WTI price was about

$99 per barrel. e Brent price averaged $111 per barrel for

the full-year 2011, compared to $80 in 2010. As of mid-

February 2012, the Brent price was about $118 per barrel.

e majority of the company’s equity crude production is

priced based on the Brent benchmark. WTI traded at a dis-

count to Brent throughout 2011 due to excess crude supply

in the U.S. Midcontinent market. e discount narrowed in

fourth quarter 2011 as crude inventories declined.

A dierential in crude oil prices exists between high

quality (high-gravity, low-sulfur) crudes and those of lower

quality (low-gravity, high-sulfur). e amount of the dif-

ferential in any period is associated with the supply of heavy

crude available versus the demand, which is a function of

the capacity of reneries that are able to process this lower

quality feedstock into light products (motor gasoline, jet fuel,

aviation gasoline and diesel fuel). e dierential widened

during 2011 primarily due to rising diesel prices and lower

availability of light, sweet crude oil due to supply disruptions

in Libya.

Chevron produces or shares in the production of heavy

crude oil in California, Chad, Indonesia, the Partitioned

Zone between Saudi Arabia and Kuwait, Venezuela and in

certain elds in Angola, China and the United Kingdom

sector of the North Sea. (See page 18 for the company’s

average U.S. and international crude oil realizations.)

In contrast to price movements in the global market

for crude oil, price changes for natural gas in many regional

markets are more closely aligned with supply-and-demand

conditions in those markets. In the United States, prices

at Henry Hub averaged about $4.00 per thousand cubic

feet (MCF) during 2011, compared with about $4.50 dur-

ing 2010. As of mid-February 2012, the Henry Hub spot

price was about $2.50 per MCF. Fluctuations in the price

for natural gas in the United States are closely associated

with customer demand relative to the volumes produced in

North America.

Outside the United States, price changes for natural gas

depend on a wide range of supply, demand and regulatory

circumstances. In some locations, Chevron is investing in

long-term projects to install infrastructure to produce and

liquefy natural gas for transport by tanker to other markets.

International natural gas realizations averaged about $5.40 per

MCF during 2011, compared with about $4.60 per MCF dur-

ing 2010. (See page 18 for the company’s average natural gas

realizations for the U.S. and international regions.)

WTI Crude Oil, Brent Crude Oil and Henry Hub Natural Gas Spot Prices —

Quarterly Average

0

60

150

120

90

30

0

10

25

20

15

5

1Q 2Q 3Q 4Q 1Q 1Q2Q 2Q3Q 3Q4Q 4Q

WTI/Brent

$/bbl

HH

$/mcf

2009 2010 2011

Brent

WTI

HH

0

6000

5000

4000

1000

2000

3000

Net natural gas production

decreased 2 percent in 2011

mainly due to field declines in the

United States, Denmark and the

United Kingdom. Partially offsetting

the declines were increases in

Bangladesh, Nigeria and new

Marcellus Shale production.

* Includes equity in affiliates.

Net Natural Gas Production*

Millions of cubic feet per day

United States

International

0807 09 10 11

4,941

0

2000

1500

1000

500

Net Liquids Production*

Thousands of barrels per day

United States

International

Net liquids production decreased

4 percent in 2011 mainly due to field

declines and maintenance-related

downtime in the United States and

lower entitlement volumes in

Indonesia and Kazakhstan.

* Includes equity in affiliates.

0807 09 10 11

1,849