Tesco 2006 Annual Report Download - page 54

Download and view the complete annual report

Please find page 54 of the 2006 Tesco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

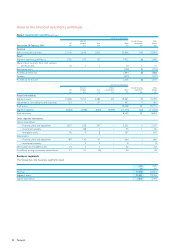

52 Tesco plc

Notes to the financial statements continued

Note 1 Accounting policies continued

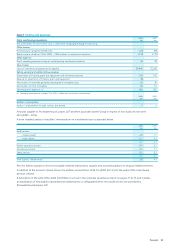

Interest differentials on derivative instruments are recognised

by adjusting net finance costs. Premia or discount on derivative

instruments is amortised over the shorter of the life of the

instrument or the underlying exposure.

Currency swap agreements are valued at closing rates of

exchange. Forward exchange contracts are valued at

discounted closing forward rates of exchange. Resulting gains

or losses are offset against foreign exchange gains or losses

on the related borrowings or, where the instrument is used to

hedge a committed future transaction, are deferred until the

transaction occurs or is extinguished.

Treatment of put option on minority interest

The Group has an agreement with the Samsung Corporation

to purchase the remaining shares of Samsung Tesco Co. Ltd.

Theseshares are expected to be purchased in three tranches

in 2007, 2011 and 2012. The purchase price will reflect the

market value of these shares at the date of acquisition.

Under IAS 32, the net present value of the expected future

payments are shown as a financial liability. At the end of

each period, the valuation of the liability is reassessed with

any changes recognised in the profit or loss for the period.

Provisions

Provisions for onerous leases are recognised when the Group

believes that the unavoidable costs of meeting the lease

obligations exceed the economic benefits expected to be

received under the lease.

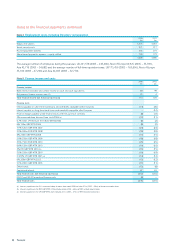

IFRSs transitional arrangements and early adoption

The rules for first-time adoption of IFRSs are set out in IFRS 1,

which requires that the Group establishes its IFRS accounting

policies for the 2005/06 reporting date and, in general, apply

these retrospectively.

The standard allows a number of optional exemptions on

transition tohelp companies simplify the move to IFRSs.

The exemptions selected by the Group are set out below:

Business Combinations (IFRS 3)

The Group has elected to apply IFRS 3 prospectively from

the date of transition to IFRSs rather than to restate previous

business combinations.

Employee Benefits (IAS 19) – Actuarial gains and losses

on defined benefit pension schemes

The Group has chosen to recognise all cumulative actuarial

gains and losses in respect of employee defined benefit plans

in full through reserves at the date of transition to IFRSs. Post-

transition, the Group is applying the rules of the amendment

to IAS 19, recognising actuarial gains and losses immediately

in the Statement of Recognised Income and Expense.

Cumulative translation differences (IAS 21)

Cumulative foreign exchange movements on translation of

foreign entities on consolidation have been set to nil as at

29 February 2004.

Financial Instruments (IAS 32 and IAS 39)

The Group opted to take advantage of the one-year exemption

for implementation of the Financial Instruments standards.

Therefore, for the 2004/05 comparatives, financial instruments

continue to be accounted for and presented in accordance with

UK GAAP. For 2005/06 financial reporting, adjustments have

been made as at 27 February 2005 to reflect the differences

between UK GAAP and IAS 32 and IAS 39 (note 33).

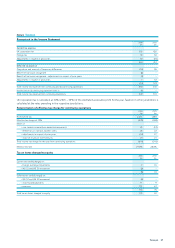

Recent accounting developments

IFRS 7 ‘Financial Instruments: Disclosures’ and amendments

toIAS 1 ‘Presentation of Financial Statements – Capital

Disclosures’ were issued in August 2005 and are effective for

accounting periods beginning on or after 1 January 2007.

Theseamendments revise and enhance previous disclosures

required by IAS 32 and IAS 30 ‘Disclosures in the Financial

Statements of Banks and Similar Financial Institutions’. These

changes are not expected to have a material effect on the

results and net assets of the Group.

Other standards, amendments and interpretations not

expected to have a significant effect on the Group include:

IFRS 6 ‘Exploration for and evaluation of mineral resources’,

amendment to IAS 39 ‘Cash flow hedge accounting of forecast

intragroup transactions’, amendment to IFRS 1, amendment

toIAS 39 and IFRS 4 ‘Insurance contracts’, IFRIC 5 ‘Rights

to interests arising from decommissioning, restoration and

environmental rehabilitation funds’ and IFRIC 7 ‘Applying the

restatement approach under IAS 29 ‘Hyperinflationary

accounting’.

Standards, amendments and interpretations still under review

as totheir effect on the Group include: Amendment to IAS 21

‘The effectof changes in foreign exchange rates: net

investment in a foreign operation’, IFRIC 4 ‘Determining

whether an arrangement contains a lease’, IFRIC 6 ‘Liabilities

arising from participating in a specific market – waste electrical

and electronic equipment’, IFRIC 8 ‘Scope of IFRS 2’ and

IFRIC 9 ‘Re-assessment of embedded derivatives’.