TCF Bank 2014 Annual Report Download - page 70

Download and view the complete annual report

Please find page 70 of the 2014 TCF Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

|

|

Notes to Consolidated Financial Statements

Note 1. Summary of Significant Accounting Policies

Basis of Presentation TCF Financial Corporation, a Delaware corporation (‘‘we,’’ ‘‘us,’’ ‘‘our,’’ ‘‘TCF’’ or the ‘‘Company’’), is a

national bank holding company based in Wayzata, Minnesota. Unless otherwise indicated, references herein to ‘‘TCF’’ include its

direct and indirect subsidiaries. Its principal subsidiary, TCF National Bank (‘‘TCF Bank’’), is headquartered in South Dakota.

References herein to ‘‘TCF Financial’’ refer to TCF Financial Corporation on an unconsolidated basis. All significant intercompany

accounts and transactions have been eliminated in consolidation.

Certain reclassifications have been made to prior period financial statements to conform to the current period presentation.

The preparation of financial statements in conformity with U.S. generally accepted accounting principles (‘‘GAAP’’) requires

management to make estimates and assumptions that affect the reported amounts of assets and liabilities, disclosure of

contingent assets and liabilities at the date of the financial statements and the reported amount of revenues and expenses during

the reporting period. These estimates are based on information available to management at the time the estimates are made.

Actual results could differ from those estimates.

Critical Accounting Policies

Critical Accounting Estimates Critical accounting estimates occur in certain accounting policies and procedures and are

particularly susceptible to significant change. Policies that contain critical accounting estimates include the determination of the

allowance for loan and lease losses, lease financing and income taxes.

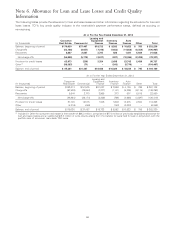

Allowance for Loan and Lease Losses The allowance for loan and lease losses is maintained at a level appropriate to provide for

probable loan and lease losses incurred in the portfolio as of the balance sheet date, including known or anticipated problem

loans and leases, as well as for loans and leases which are not currently known to require specific allowances. Loans classified as

troubled debt restructuring (‘‘TDR’’) loans are considered impaired loans. TCF individually evaluates impairment on all impaired

commercial and inventory finance loans, certain large impaired equipment finance loans and leases, large consumer real estate

TDR loans, auto finance TDR loans and all non-accrual Winthrop Resources Corporation (‘‘Winthrop’’) leases. All other loans and

leases are evaluated collectively for impairment. See Note 6, Allowance for Loan and Lease Losses and Credit Quality

Information, for a definition of impaired loans.

Loan impairment on consumer real estate TDR loans is a key component of the allowance for loan and lease losses. Impairment

is generally based upon the present value of the expected future cash flows discounted at the loan’s initial effective interest rate,

unless the loans are collateral dependent, in which case loan impairment is based upon the fair value of the collateral less selling

expenses. See Note 6, Allowance for Loan and Lease Losses and Credit Quality Information, for further information on the

determination of the allowance for losses on accruing consumer real estate TDR loans.

Loan impairment on commercial, equipment finance and inventory finance loans is generally based upon the present value of the

expected future cash flows discounted at the loan’s initial effective interest rate, unless the loans are collateral dependent, in

which case loan impairment is based upon the fair value of collateral less estimated selling costs; however, if payment or

satisfaction of the loan is dependent on the operation, rather than the sale of the collateral, the impairment does not include

selling costs.

The impairment for all other loans and leases is evaluated collectively by various characteristics. The collective evaluation of

incurred losses in these portfolios is based upon their historical loss rates multiplied by the respective loss emergence period.

Factors utilized in the determination of the amount of the allowance include historical trends in loss rates, the portfolio’s overall

risk characteristics, changes in its character or size, risk rating migration, delinquencies, collateral values and prevailing economic

conditions.

Loans and leases are charged off to the extent they are deemed to be uncollectible. Charge-offs related to confirmed losses are

utilized in the historical data in calculating the allowance for loan and lease losses. Consumer real estate loans are charged off to

the estimated fair value of underlying collateral, less estimated selling costs, no later than 150 days past due. Additional review of

the fair value, less estimated costs to sell, compared with the recorded value occurs upon foreclosure and additional charge-offs

are recorded if necessary. Auto finance loans are generally charged off to the estimated fair value of underlying collateral, less

estimated selling costs, if repossession is reasonably assured and in process. Otherwise, auto finance loans are charged off in

full no later than 120 days past due. Deposit account overdrafts, which are included within other loans, are charged off at or

57