TCF Bank 2014 Annual Report Download - page 54

Download and view the complete annual report

Please find page 54 of the 2014 TCF Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

|

|

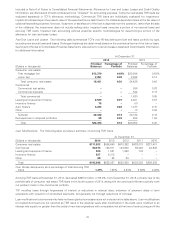

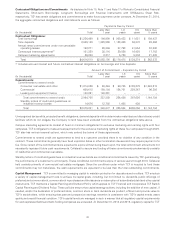

ALCO and the Finance Committee of the TCF Financial Board of Directors have adopted a Holding Company Investment and

Liquidity Management Policy, which establishes the minimum amount of cash or liquid investments TCF Financial will hold. See

‘‘Item 7A. Quantitative and Qualitative Disclosures about Market Risk’’ for more information. TCF Financial had cash and liquid

investments of $71.8 million and $62.8 million at December 31, 2014 and 2013, respectively.

Deposits are the primary source of TCF’s funds for use in lending and for other general business purposes. In addition to

deposits, TCF derives funds from loan and lease repayments, loan sales and borrowings. Lending activities, such as loan

originations and purchases and equipment purchases for lease financing, are the primary uses of TCF’s funds. Deposit inflows

and outflows are significantly influenced by general interest rates, money market conditions, competition for funds, customer

service and other factors. TCF’s deposit inflows and outflows have been and will continue to be affected by these factors.

Borrowings may be used to compensate for reductions in normal sources of funds, such as deposit inflows at less than projected

levels, net deposit outflows or to fund balance sheet growth. Historically, TCF has borrowed primarily from the FHLB of Des

Moines, institutional sources under repurchase agreements and other sources.

The primary source of funding for TCF Commercial Finance Canada, Inc. (‘‘TCFCFC’’) is a line of credit with TCF Bank. Primarily

for contingency purposes, TCFCFC maintains a $20.0 million Canadian dollar-denominated line of credit facility with a

counterparty, which is guaranteed by TCF Bank and was unused at both December 31, 2014 and 2013.

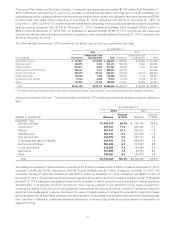

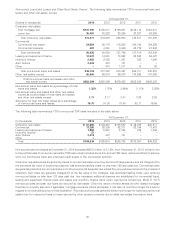

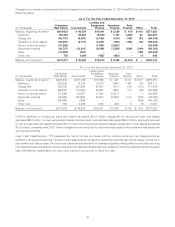

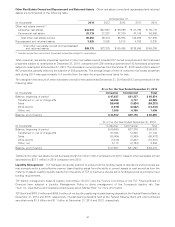

Deposits Deposits totaled $15.4 billion at December 31, 2014, an increase of $1.0 billion, or 7.0%, from December 31, 2013,

primarily due to promotions for money market accounts and certificates of deposit.

Checking, savings and money market deposits are an important source of low interest cost funds for TCF. These deposits totaled

$12.4 billion at December 31, 2014, an increase of $0.4 billion from December 31, 2013, and comprised 80.3% of total deposits

at December 31, 2014, compared with 83.2% of total deposits at December 31, 2013. The average balance of these forms of

deposits during 2014 was $12.1 billion, an increase of $0.3 billion from the $11.8 billion average balance for 2013.

Certificates of deposit totaled $3.0 billion at December 31, 2014, compared with $2.4 billion at December 31, 2013.

Non-interest bearing checking represented 18.3% of total deposits at both December 31, 2014 and 2013. TCF’s weighted-

average rate for deposits, including non-interest bearing deposits, was 0.26% at both December 31, 2014 and 2013.

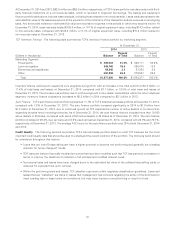

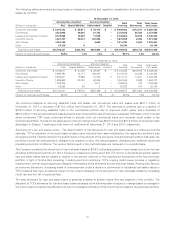

Borrowings Borrowings totaled $1.2 billion and $1.5 billion at December 31, 2014 and 2013, respectively. The weighted-

average rate on long-term borrowings was 1.63% and 1.41% at December 31, 2014 and 2013, respectively. Historically, TCF has

borrowed primarily from the FHLB of Des Moines, institutional sources under repurchase agreements and other sources. At

December 31, 2014, TCF had $2.6 billion of unused, secured borrowing capacity at the FHLB of Des Moines.

On March 17, 2014, TCF Bank redeemed the aggregate principal amount of $50.0 million of subordinated notes due 2015, since

the notes no longer qualified for treatment as Tier 2 or supplementary capital prior to redemption.

See Note 11 of Notes to Consolidated Financial Statements, Long-term Borrowings, for additional information regarding TCF’s

long-term borrowings.

41