Supercuts 2012 Annual Report Download - page 37

Download and view the complete annual report

Please find page 37 of the 2012 Supercuts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

|

|

Table of Contents

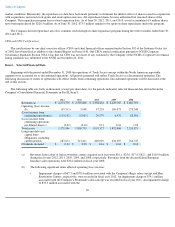

including allocation of shared or corporate balances among reporting units. Allocations are generally based on the number of salons in each

reporting unit as a percent of total company-owned salons.

The Company calculates the estimated fair value of the reporting units based on discounted future cash flows that utilize estimates in

annual revenue, gross margins, fixed expense rates, allocated corporate overhead, and long-term growth rates for determining terminal value.

The Company's estimated future cash flows also take into consideration acquisition integration and maturation. Where available and as

appropriate, comparative market multiples are used in conjunction with the results of the discounted cash flows. The Company considers its

various concepts to be reporting units when testing for goodwill impairment because that is where the goodwill resides. The Company

periodically engages third-party valuation consultants to assist in evaluation of the Company's estimated fair value calculations.

In the situations where a reporting unit's carrying value exceeds its estimated fair value, the amount of the impairment loss must be

measured. The measurement of impairment is calculated by determining the implied fair value of a reporting unit's goodwill. In calculating the

implied fair value of goodwill, the fair value of the reporting unit is allocated to all other assets and liabilities of that unit based on the relative

fair values under the assumption of a taxable transaction. The excess of the fair value of the reporting unit over the amount assigned to its assets

and liabilities is the implied fair value of goodwill. The goodwill impairment is measured as the excess of the carrying value of goodwill over

its implied fair value.

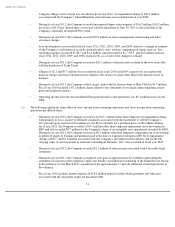

As previously disclosed, the Company concluded that it was reasonably likely that goodwill for the Regis and Hair Restoration Centers

reporting units might become impaired in future periods.

As a result of the Company's annual impairment testing of goodwill during the fourth quarter of fiscal year 2012, a $67.7 million

impairment charge was recorded within continuing operations for the excess of the carrying value of goodwill over the implied fair value of the

goodwill for the Regis salon concept. The Regis salon concept reported same-store sales of negative 4.0 percent for the ten months ended

April 30, 2012, which was unfavorable compared to the Company's budgeted same-

store sales. Visitation patterns did not rebound as quickly as

the Company originally projected. Accordingly, the Company reduced the budgeted financial projections for future years. After the impairment

charge the Regis salon concept reporting unit had $35.1 million of goodwill. The impairment was only partially deductible for tax purposes

resulting in a tax benefit of $12.5 million.

During the three months ended December 31, 2011 the Company updated the projections for the Hair Restoration Centers reporting unit

used in the fiscal 2011 annual impairment test to reflect the impact of recent industry developments, including a slow down in revenue growth

and increasing supply costs. The Company determined there was a triggering event as it was more likely than not that the fair value of the Hair

Restoration Centers was below carrying value and performed an interim impairment test of goodwill during the three months ended

December 31, 2011.

As a result of the Company's interim impairment test of goodwill related to the Hair Restoration Centers reporting unit during the second

quarter of fiscal year 2012, a $78.4 million impairment charge was recorded within continuing operations for the excess of the carrying value of

goodwill over the implied fair value of the goodwill for the Hair Restorations Centers reporting unit. After the impairment charge the Hair

Restoration Centers reporting unit had $74.4 million of goodwill. The impairment was only partially deductible for tax purposes resulting in a

tax benefit of $5.9 million. See further discussion on the effective tax rate for the twelve months ended June 30, 2012 within Note 12 to the

Consolidated Financial Statements.

35