Starwood 2015 Annual Report Download - page 30

Download and view the complete annual report

Please find page 30 of the 2015 Starwood annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

|

|

Table of Contents

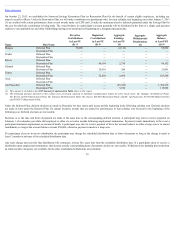

When establishing target compensation levels for 2015, the Compensation Committee reviewed peer group data on payments to named executive officers as

reported in proxy statements available as of February 2015 as provided by Meridian. As outlined in the section entitled Design and Operation of Starwood’s 2015

Executive Compensation Program below in this report, we broadly target total compensation opportunities at the median (50th percentile) of the market for target

performance levels; however, we also review the range of values around the median, including out to the 25th and 75th percentiles. Despite these initial actions, we

believe that benchmarking alone does not provide a complete basis for establishing compensation levels or design practices under our programs. As a result, actual

individual compensation may be above or below our targeted levels based on Company and individual performance, key responsibilities, unique market demands,

and experience level, as analyzed each year and as further described above.

Tax Considerations

Section 162(m) of the Code (or Section 162(m)) generally disallows a federal income tax deduction to public companies for compensation in excess of $1,000,000

paid to the Chief Executive Officer and to each of the three other most highly compensated executive officers (other than, generally, the Chief Financial Officer) in

any taxable year. Qualified performance-based compensation (as defined under Section 162(m) and applicable regulations) is not subject to the deduction limit if

certain requirements are met. Although the Compensation Committee may take actions intended to limit the impact of Section 162(m), the Compensation

Committee also believes that the tax deduction is only one of several relevant considerations in setting named executive officer compensation. The Compensation

Committee believes that the tax deduction limitation should not be permitted to compromise our ability to design and maintain named executive officer

compensation arrangements that will attract and retain the executive talent to allow us to compete successfully in our industry. Accordingly, achieving the desired

flexibility in the design and delivery of compensation may result in compensation that in certain cases is not deductible for federal income tax purposes.

Share Ownership Guidelines

We have adopted share ownership guidelines for our executive officers, including the named executive officers. Pursuant to the guidelines, the covered named

executive officers, including our former President and Chief Executive Officer and our former Interim Chief Executive Officer, are (or were) required to hold a

number of shares having a market value equal to or greater than a multiple of each executive’s base salary. For Messrs. van Paasschen and Aron, the multiple was

six times base salary, for Mr. Mangas (effective as of his assumption of the role of Chief Executive Officer), the multiple is six times base salary, for Mr. Rivera,

Division President, the multiple is three times base salary, and for the other covered named executive officers (including Mr. Mangas prior to December 31, 2015),

the multiple is four times base salary. Mr. Schnaid is not subject to the share ownership guidelines. This multiple is reduced by one times base salary, however, for

executives that are retirement eligible. A retention requirement of 35% is applied to restricted shares upon vesting (net shares after tax withholding) and shares

obtained from option exercises until the executive meets the target, or if an executive falls out of compliance. Shares owned, stock equivalents (vested/unvested

restricted stock units) and unvested restricted stock (pre-tax) count towards meeting ownership targets. However, unexercised stock options and unearned

performance-based equity do not count towards meeting the target. Covered named executive officers have five years from the date of hire or, if later, the date they

first become subject to the policy, to meet the ownership requirements. All named executive officers subject to ownership requirements, with the exception of

Mr. Mangas (due to his recent employment with us and the increase to his base salary multiple in connection with his promotion to Chief Executive Officer), were

in compliance with share ownership guidelines as of December 31, 2015.

Equity Grant Practices

Timing of Equity Grants. For 2015, the Compensation Committee made annual equity compensation grants on February 27, 2015 to named executive officers who

were serving at the beginning of 2015. The grant date

28