SkyWest Airlines 2013 Annual Report Download - page 155

Download and view the complete annual report

Please find page 155 of the 2013 SkyWest Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

|

|

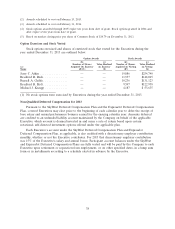

plans generally define a ‘‘change in control’’ as any of the following events: (i) the acquisition by any

person of 50% or more of the Company’s voting shares, (ii) replacement of a majority of the

Company’s directors within a two-year period under certain conditions, or (iii) shareholder approval of

a merger in which the Company is not the surviving entity, sale of substantially all of the Company’s

assets or liquidation. All shares of restricted stock previously issued under the Company’s 2006

Long-Term Incentive Plan and prior long-term incentive plans became fully vested prior to 2013;

accordingly, a change in control of the Company in 2013 would not have accelerated the vesting of

such restricted stock.

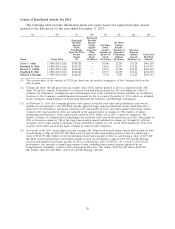

The following table shows for each Executive the intrinsic value of his unvested stock options,

unvested restricted stock units and performance units payable in cash, as of December 31, 2013, that

would have been accelerated had a change in control of the Company occurred on that date, calculated

in the case of restricted stock units and stock options, by multiplying the number of underlying shares

by the closing price of the Common Stock on the last trading day of 2013 ($14.79 per share) and, in

the case of stock options, by then subtracting the applicable option exercise price:

Early Vesting Early Vesting of Early Vesting of

Name of Stock Options Restricted Stock Units Performance Units

Jerry C. Atkin ............ $136,635 $1,003,457 $785,795

Bradford R. Rich .......... $ 87,487 $ 602,086 $488,186

Russell A. Childs .......... $ 74,465 $ 509,811 $413,199

Bradford R. Holt .......... $ 73,885 $ 509,797 $413,199

Michael J. Kraupp ......... $ 26,618 $ 216,141 $175,023

If a change in control with respect to the Company results in acceleration of vesting of an

Executive’s otherwise unvested stock options, unvested restricted stock units or performance unit

awards payable in cash, and if the value of such acceleration equals or exceeds three times the

Executive’s average W-2 compensation with the Company for the five taxable years preceding the year

of the change in control (the ‘‘Base Period Amount’’), the acceleration would result in an excess

parachute payment under Code Section 280G. An Executive would be subject to a 20% excise tax on

any such parachute payment in excess of the Base Period Amount, and the Company would be unable

to deduct the amount of the parachute payment in excess of the Base Period Amount for tax purposes.

The Company has not agreed to provide its Executives with any gross-up or reimbursement for excise

taxes imposed on excess parachute payments.

Deferred Compensation. If the employment of an Executive were terminated on December 31,

2013, the Executive would have become entitled to receive the balance in his account under the

applicable deferred compensation plan. Distribution would be made in the form of a lump sum or in

installments, and in accordance with the distributions schedule elected by the Executive under the

applicable plan. The 2013 year-end account balances under those plans are shown in column (e) in the

applicable Non-qualified Deferred Compensation Tables set forth above. An Executive’s account

balance would continue to be credited with notational investment earnings or losses through the date of

actual distribution.

41