Royal Caribbean Cruise Lines 2012 Annual Report Download - page 17

Download and view the complete annual report

Please find page 17 of the 2012 Royal Caribbean Cruise Lines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

|

|

13

result of the effects of the Costa Concordia incident

and the continued instability in the European eco-

nomic landscape. However, we continue to believe in

the long term growth potential of this market. We

estimate that Europe was served by 102 ships with

approximately 108,000 berths at the beginning of

2008 and by 117 ships with approximately 156,000

berths at the end of 2012. There are approximately

9 ships with an estimated 25,000 berths that are

expected to be placed in service in the European

cruise market between 2013 and 2017.

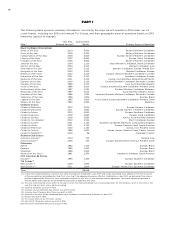

The following table details the growth in the global, North American and European cruise markets in terms of

cruise guests and estimated weighted-average berths over the past five years:

Year

Global

Cruise Guests(1)

Weighted-Average

Supply of Berths

Marketed Globally(1)

North American

Cruise Guests(2)

Weighted-Average

Supply of Berths

Marketed in

North America(1)

European

Cruise Guests

Weighted-Average

Supply of Berths

Marketed in

Europe(1)

() Source: Our estimates of the number of global cruise guests, and the weighted-average supply of berths marketed globally, in North America

and Europe are based on a combination of data that we obtain from various publicly available cruise industry trade information sources

including Seatrade Insider and Cruise Line International Association (“CLIA”). In addition, our estimates incorporate our own statistical analysis

utilizing the same publicly available cruise industry data as a base.

() Source: Cruise Line International Association based on cruise guests carried for at least two consecutive nights for years 2008 through 2011.

Year 2012 amounts represent our estimates (see number 1 above).

() Source: CLIA Europe, formerly European Cruise Council, for years 2008 through 2011. Year 2012 amounts represent our estimates (see number

1 above).

Other Markets

In addition to expected industry growth in North

America and Europe as discussed above, we expect

the Asia/Pacific region to demonstrate an even higher

growth rate in the near term, although it will continue

to represent a relatively small sector compared to

North America and Europe.

COMPETITION

We compete with a number of cruise lines. Our princi-

pal competitors are Carnival Corporation & plc, which

owns, among others, Aida Cruises, Carnival Cruise

Lines, Costa Cruises, Cunard Line, Holland America

Line, Iberocruceros, P&O Cruises and Princess Cruises;

Disney Cruise Line; MSC Cruises; Norwegian Cruise

Line and Oceania Cruises. Cruise lines compete with

other vacation alternatives such as land-based resort

hotels and sightseeing destinations for consumers’

leisure time. Demand for such activities is influenced

by political and general economic conditions. Com-

panies within the vacation market are dependent on

consumer discretionary spending.

OPERATING STRATEGIES

Our principal operating strategies are to:

• protect the health, safety and security of our guests

and employees and protect the environment in

which our vessels and organization operate,

• strengthen and support our human capital in order

to better serve our global guest base and grow

our business,

• further strengthen our consumer engagement in

order to enhance our revenues,

• increase the awareness and market penetration of

our brands globally,

• focus on cost efficiency, manage our operating

expenditures and ensure adequate cash and liquid-

ity, with the overall goal of maximizing our return on

invested capital and long-term shareholder value,

• strategically invest in our fleet through the revit

alization of existing ships and the transfer of key

innovations across each brand, while prudently

expanding our fleet with the new state-of-the-art

cruise ships recently delivered and on order,

• capitalize on the portability and flexibility of our

ships by deploying them into those markets and

itineraries that provide opportunities to optimize

returns, while continuing our focus on existing

key markets,

• further enhance our technological capabilities to

service customer preferences and expectations in an

innovative manner, while supporting our strategic

focus on profitability, and

PART I