Nissan 2007 Annual Report Download - page 71

Download and view the complete annual report

Please find page 71 of the 2007 Nissan annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

|

|

FINANCIAL SECTION»

Nissan Annual Report 2006-2007 69

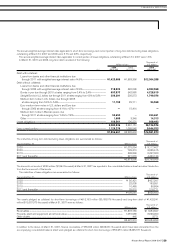

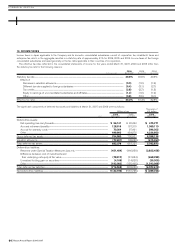

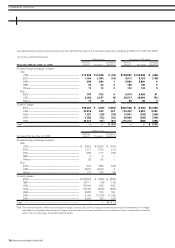

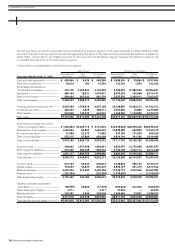

Thousands of U.S. dollars

Due in Due after one Due after five

one year or year through years through Due after

Fiscal year 2006 (As of Mar. 31, 2007) less five years ten years ten years

Debt securities........................................................................................................................................................................ $2,661 $ — $ — $ —

Corporate bonds ................................................................................................................................................................... — — 500 —

Total................................................................................................................................................................................................. $2,661 $ — $500 $ —

20. DERIVATIVE TRANSACTIONS

Hedging Policies

The Company and its consolidated subsidiaries (collectively, the

“Group”) utilize derivative transactions for the purpose of hedging

their exposure to fluctuation in foreign exchange rates, interest rates

and market prices. However, based on an internal management rule

on financial market risk (the “Rule”) approved by the Company’s

Board of Directors, they do not enter into transactions involving

derivatives for speculative purposes. The Rule prescribes that (i) the

Group’s financial market risk is to be controlled by the Company in a

centralized manner, and that (ii) no individual subsidiary can initiate a

hedge position without the prior approval of and regular reporting to

the Company.

Risk to be hedged by derivative transactions

(1) Market risk

The financial market risk to which the Group is generally exposed in

its operations and the relevant derivative transactions primarily used

for hedging are summarized as follows:

• Foreign exchange risk associated with assets and liabilities

denominated in foreign currencies: forward foreign exchange

contracts, foreign currency options, and currency swaps;

• Interest rate risk associated with sourcing funds and investing:

interest-rate swaps;

• Risk of fluctuation in stock prices: options on stocks;

• Risk of fluctuation in commodity prices (mainly for precious metals):

commodity futures contracts

(2) Credit risk

The Group is exposed to the risk that a counterparty to its financial

transactions could default and jeopardize future profits. We believe

that this risk is insignificant as the Group enters into derivative

transactions only with financial institutions which have a sound credit

profile. The Group enters into these transactions also with Renault

Finance S.A. (“RF”), a specialized financial subsidiary of the Renault

Group which, we believe, is not subject to any such material risk.

This is because RF enters into derivative transactions to cover

such derivative transactions with us only with financial institutions of

the highest caliber carefully selected by RF based on its own rating

system which takes into account each counterparty's long-term credit

rating and shareholders' equity.

(3) Legal risk

The Group is exposed to the risk of entering into a financial

agreement which may contain inappropriate terms and conditions as

well as to the risk that an existing contract may subsequently be

affected by revisions to the relevant laws and regulations.

The Company’s Legal Department and Finance Department make

every effort to minimize legal risk by reviewing any new agreements

of significance and by reviewing the related documents in a

centralized manner.

Risk Management

All strategies to manage financial market risk and risk hedge

operations of the Group are carried out pursuant to the Rule which

stipulates the Group’s basic policies for derivative transactions,

management policies, management items, procedures, criteria for the

selection of counterparties, and the reporting system, and so forth.

The Rule prescribes that (i) the Group’s financial market risk is to be

controlled by the Company in a centralized manner, and that (ii) no

individual subsidiary is permitted to initiate a hedging operation

without the prior approval of and regular reporting to the Company.

The basic hedge policy is subject to the approval of the Monthly

Hedge Policy Meeting attended by the corporate officer in charge of

Treasury Department. Execution and management of all deals are to

be conducted pursuant to the Rule.

Derivative transactions are conducted by a special section of the

Treasury Department and monitoring of contracts for such

transactions and confirming the balance of all open positions are the

responsibility of back office and risk management section.

Commodity futures contracts are to be handled also by Treasury

Department under guidelines which are to be drawn up by the MRMC

(Materials Risk Management Committee).

The MRMC is chaired by the corporate officer in charge of the

Purchasing Department and the corporate officer in charge of

Treasury Department and it will meet approximately once every six

months.

The status of derivative transactions is reported on a daily basis to

the chief officer in charge of Treasury Department and on an annual

basis to the Board of Directors.

Credit risk is monitored quantitatively with reference to Renault’s

rating system based principally on the counterparties’ long-term

credit ratings and on their shareholders’ equity.

The Finance Department sets a maximum upper limit on positions

with each of the counterparties for the Group and monitors the

balances of open positions every day.