Mazda 2010 Annual Report Download - page 66

Download and view the complete annual report

Please find page 66 of the 2010 Mazda annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

-

78

|

|

64

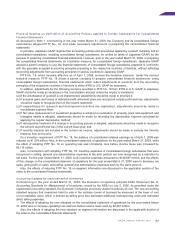

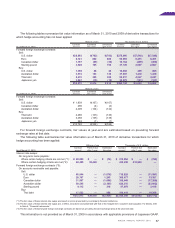

The liabilities for severance and retirement benefits as of March 31, 2010 and 2009 consisted of the following:

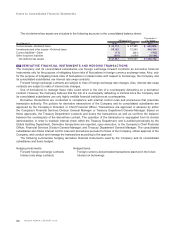

Thousands of

Millions of yen U.S. dollars

As of March 31 2010 2009 2010

Projected benefit obligation ¥ 289,069 ¥ 302,253 $ 3,108,269

Unrecognized prior service costs 17,152 19,428 184,430

Unrecognized actuarial differences (53,833) (95,144) (578,849)

Less fair value of pension assets (172,610) (143,292) (1,856,022)

Prepaid pension cost 4,775 7,676 51,344

Liability for severance and retirement benefits ¥ 84,553 ¥ 90,921 $ 909,172

Severance and retirement benefit expenses for the years ended March 31, 2010 and 2009 consisted of the

following:

Thousands of

Millions of yen U.S. dollars

For the years ended March 31 2010 2009 2010

Service costs—benefits earned during the year ¥11,344 ¥12,195 $121,979

Interest cost on projected benefit obligation 6,518 6,486 70,086

Expected return on plan assets (2,962) (5,589) (31,849)

Amortization of prior service costs (2,423) (2,232) (26,054)

Amortization of actuarial differences 10,156 8,030 109,204

Severance and retirement benefit expenses ¥22,633 ¥18,890 $243,366

The discount rates and the rates of expected return on plan assets were primarily 2.1% and 1.5%, respectively, for

the year ended March 31, 2010. The respective rates were primarily 2.0% and 3.0% for the year ended March 31, 2009.

For both the years ended March 31, 2010 and 2009, the estimated amount of all retirement benefits to be paid at

the future retirement dates is allocated equally to each service year using the estimated number of total service years.

For the years ended March 31, 2010 and 2009, accrued pension costs related to defined contribution plans

amounted to ¥1,940 million ($20,860 thousand) and ¥2,079 million, respectively.

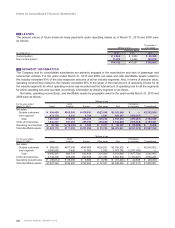

Contingent liabilities as of March 31, 2010 were as follows:

Thousands of

Millions of yen U.S. dollars

Factoring of receivables with recourse ¥ 340 $ 3,656

Guarantees of loans and similar agreements 11,854 127,462

Under Japanese laws and regulations, the entire amount paid for new shares is required to be designated as common

stock. However, a company may, by a resolution of the Board of Directors, designate an amount not exceeding one

half of the price of the new shares as additional paid-in capital, which is included in capital surplus.

Under the Corporate Law (“the Law”), in cases where dividend distribution of surplus is made, the smaller of an

amount equal to 10% of the dividend or the excess, if any, of 25% of common stock over the total of additional paid-in

capital and legal earnings reserve, must be set aside as additional paid-in capital or legal earnings reserve. Legal

earnings reserve is included in retained earnings in the accompanying consolidated balance sheets. Legal earnings

reserve and additional paid-in capital could be used to eliminate or reduce a deficit or could be capitalized by a

resolution of the shareholder’s meeting. Additional paid-in capital and legal earnings reserve may not be distributed as

dividends. Under the Law, all additional paid-in capital and legal earnings reserve may be transferred to other capital

surplus and retained earnings, respectively, which are potentially available for dividends. The maximum amount

that the Company can distribute as dividends is calculated based on the non-consolidated financial statements of

the Company in accordance with the Law. Cash dividends charged to retained earnings during the fiscal year were

year-end cash dividends for the preceding fiscal year and interim cash dividends for the current fiscal year.