Mazda 2010 Annual Report Download - page 63

Download and view the complete annual report

Please find page 63 of the 2010 Mazda annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

-

75

-

76

-

77

-

78

|

|

61

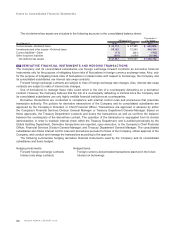

For notes on securities by classification, refer to “Securities” under Note 2, “Significant Accounting Policies,” and

Note 5, “Securities.”

3) Long-term loans receivable

Long-term loans receivable consist of variable interest loans. As such, the interest rates on these loans reflect the

market rates of interest within short periods of time. Also, the credit standings of borrowers of these loans have not

changed significantly since the execution of these loans. Accordingly, the carrying values are used as the fair values

of these loans receivable.

For loans receivable at a high risk, the fair value is calculated mainly based on amounts estimated to be collectible

through collateral and guarantees.

Liabilities

1) Trade notes and accounts payable, 2) Other accounts payable, and 3) Short-term loans payable

These payables are settled within short periods of time. Hence, their carrying values approximate their fair values.

Accordingly, carrying values are used as the fair values of these payables.

4) Long-term debt

a) Bonds payable

The fair value of bonds issued by the Company and its consolidated subsidiaries is based on the market price

where such a price is available. Otherwise, the sum of the present value of principal and interest payments is

used as the fair value of bonds payable. The discount rates used in computing the present value reflect the time

to maturity of the bonds as well as credit risk.

b) Long-term loans payable and c) Lease obligations

The fair value of these liabilities is calculated by the sum of the principal and interest payments discounted to

present value, using the imputed interest rate that would be required to newly execute a similar borrowing or

lease transaction.

For some long-term loans payable with variable interest rates, interest rate swaps are used as a hedge

against interest rate fluctuations. When such interest rate swaps meet certain hedging criteria, the net amount

to be paid or received under the interest rate swap contract is added to or deducted from the interest on the

long-term loans payable. In such cases, the resulting net interest on the long-term loans payable is used in

calculating the present value. (Refer to “Derivatives and hedge accounting” under Note 2 “Significant Accounting

Policies.”)

Derivative instruments

Refer to Note 15, “Derivative Financial Instruments and Hedging Transactions.”

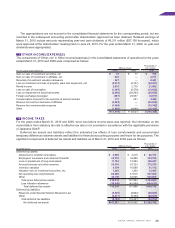

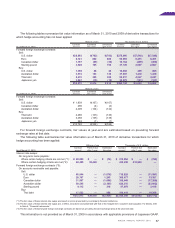

As of March 31, 2010, scheduled amounts of redemption of securities with maturities and receivables were as

follows:

Millions of yen Thousands of U.S. dollars

Within

1 year

Over 1 year,

within

5 years

Over 5 years,

within

10 years

Over

10 years

Within

1 year

Over 1 year,

within

5 years

Over 5 years,

within

10 years

Over

10 years

Trade notes and accounts receivable ¥170,645 ¥1,844 ¥ — ¥ — $1,834,892 $19,828 $ — $ —

Short-term investments and

investment securities

Available-for-sale securities with

maturities 20,000 — — — 215,054 — — —

Long-term loans receivable 158 4,369 537 907 1,699 46,978 5,774 9,753

¥190,803 ¥6,213 ¥537 ¥907 $2,051,645 $66,806 $5,774 $9,753

For the schedule of repayment of long-term debt after the consolidated balance sheet date, refer to Note 9, “Short-

Term Debt and Long-Term Debt.”