Macy's 2015 Annual Report Download - page 36

Download and view the complete annual report

Please find page 36 of the 2015 Macy's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

|

|

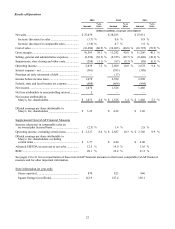

31

Income Taxes

Income taxes are estimated based on the tax statutes, regulations and case law of the various jurisdictions in which

the Company operates. Deferred income tax assets and liabilities are recognized for the future tax consequences

attributable to differences between the financial statement carrying amounts of existing assets and liabilities and their

respective tax bases, and net operating loss and tax credit carryforwards. Deferred income tax assets and liabilities are

measured using enacted tax rates expected to apply to taxable income in the years in which those temporary differences are

expected to be recovered or settled. Deferred income tax assets are evaluated for recoverability based on all available

evidence, including past operating results, estimates of future taxable income, and the feasibility of tax planning strategies.

Deferred income tax assets are reduced by a valuation allowance when it is more likely than not that some portion of the

deferred income tax assets will not be realized.

Uncertain tax positions are recognized if the weight of available evidence indicates that it is more likely than not that

the tax position will be sustained on examination, including resolution of any related appeals or litigation processes, based

on the technical merits of the position. Uncertain tax positions meeting the more-likely-than-not recognition threshold are

then measured to determine the amount of benefit eligible for recognition in the financial statements. Each uncertain tax

position is measured at the largest amount of benefit that is more likely than not to be realized upon ultimate settlement.

Uncertain tax positions are evaluated and adjusted as appropriate, while taking into account the progress of audits of

various taxing jurisdictions. The Company does not anticipate that resolution of these matters will have a material impact

on the Company's consolidated financial position, results of operations or cash flows.

Significant judgment is required in evaluating the Company's uncertain tax positions, provision for income taxes, and

any valuation allowance recorded against deferred tax assets. Although the Company believes that its judgments are

reasonable, no assurance can be given that the final tax outcome of these matters will not be different from that which is

reflected in the Company's historical income provisions and accruals.

Self-Insurance Reserves

The Company, through its insurance subsidiary, is self-insured for workers' compensation and general liability claims

up to certain maximum liability amounts. Although the amounts accrued are actuarially determined by third parties based

on analysis of historical trends of losses, settlements, litigation costs and other factors, the amounts the Company will

ultimately disburse could differ from such accrued amounts.

Pension and Supplementary Retirement Plans

The Company has a funded defined benefit pension plan (the “Pension Plan”) and an unfunded defined benefit

supplementary retirement plan (the “SERP”). The Company accounts for these plans in accordance with ASC Topic 715,

“Compensation - Retirement Benefits.” Under ASC Topic 715, an employer recognizes the funded status of a defined

benefit postretirement plan as an asset or liability on the balance sheet and recognizes changes in that funded status in the

year in which the changes occur through comprehensive income. Additionally, pension expense is generally recognized on

an accrual basis over the average remaining lifetime of participants. The pension expense calculation is generally

independent of funding decisions or requirements.

The Pension Protection Act of 2006 provides the funding requirements for the Pension Plan which are different from

the employer's accounting for the plan as outlined in ASC Topic 715. No funding contributions were required, and the

Company made no funding contributions to the Pension Plan in 2015. As of the date of this report, the Company does not

anticipate making funding contributions to the Pension Plan in 2016. Management believes that, with respect to the

Company's current operations, cash on hand and funds from operations, together with available borrowing under its credit

facility and other capital resources, will be sufficient to cover the Company's Pension Plan cash requirements in both the

near term and also over the longer term.

At January 30, 2016, the Company had unrecognized actuarial losses of $1,451 million for the Pension Plan and

$261 million for the SERP. The unrecognized losses for the Pension Plan and the SERP will be recognized as a component

of pension expense in future years in accordance with ASC Topic 715, and is expected to impact 2016 Pension and SERP

net periodic benefit costs by approximately $39 million. The Company generally amortizes unrecognized gains and losses

on a straight-line basis over the average remaining lifetime of participants using the corridor approach. In addition,

approximately $135 million of net actuarial losses are also expected to be recognized in 2016 as part of a non-cash

settlement charge, resulting from an anticipated increase in lump sum distributions associated with store closings, a

voluntary separation program and organizational restructuring and small balance force outs, in addition to annual

distribution activity.