Kohl's 2015 Annual Report Download - page 27

Download and view the complete annual report

Please find page 27 of the 2015 Kohl's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

|

|

Table of Contents

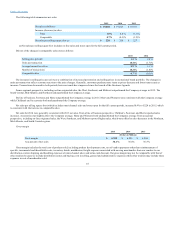

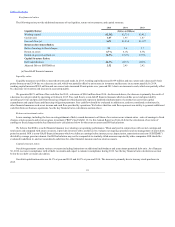

Retail Inventory Method and Inventory Valuation

We value our inventory at the lower of cost or market with cost determined on the first-in, first-out (“FIFO”) basis using the retail inventory method

(“RIM”). Under RIM, the valuation of inventories at cost and the resulting gross margins are calculated by applying a cost-to-retail ratio to the retail value of

the inventories. Inherent in the retail inventory method are certain management estimates that may affect the ending inventory valuation as well as gross

margin.

The use of RIM will generally result in inventories being valued at the lower of cost or market as permanent markdowns are taken as a reduction of the

retail value of inventories. Management estimates the need for an additional markdown reserve based on a review of historical clearance markdowns, current

business trends, expected vendor funding and discontinued merchandise categories.

We also record a reserve for estimated inventory shrink between the last physical inventory count and the balance sheet date. Shrink is the difference

between the recorded amount of inventory and the physical inventory. Shrink may occur due to theft, loss, inaccurate records for the receipt of inventory or

deterioration of goods, among other things. We generally perform an annual physical inventory count at the majority of our stores and distribution centers.

The shrink reserve is based on sales and actual shrink results from previous inventories.

We did not make any material changes in the methodologies used to value our inventory or to estimate the markdown and shrink reserves during 2015,

2014 or 2013. We believe that we have sufficient current and historical knowledge to record reasonable estimates for our inventory reserves. Though

historical reserves have approximated actual markdowns and shrink adjustments, it is possible that future results could differ from current recorded reserves.

We routinely record permanent markdowns for potentially obsolete merchandise, and, therefore, did not have a markdown reserve as of January 30,

2016. Changes in the assumptions used to estimate our markdown reserve requirement would not have had a material impact on our financial statements. A

10 basis point change in estimated inventory shrink would also have had an immaterial impact on our financial statements.

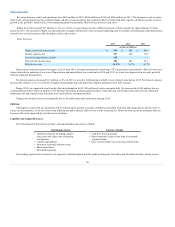

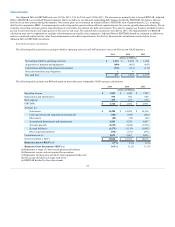

Vendor Allowances

We receive allowances from many of our merchandise vendors. These allowances often are reimbursements for markdowns that we have taken in order

to sell the merchandise and/or to support the gross margins earned in connection with the sales of merchandise. The allowances generally relate to sold

inventory or permanent markdowns and, accordingly, are reflected as reductions to cost of merchandise sold. Allowances related to merchandise that has not

yet been sold are recorded in inventory.

We also receive vendor allowances which represent reimbursements of costs (primarily marketing) that we have incurred to promote the vendors’

merchandise. These allowances are netted against marketing or the other related costs as the costs are incurred. Marketing allowances in excess of costs

incurred are recorded as a reduction of merchandise costs.

Most of our vendor allowance agreements are supported by signed contracts which are binding, but informal in nature. The terms of these arrangements

vary significantly from vendor to vendor and are influenced by, among other things, the type of merchandise to be supported. Vendor allowances will

fluctuate based on the amount of promotional and clearance markdowns necessary to liquidate the inventory as well as marketing and other reimbursed costs.

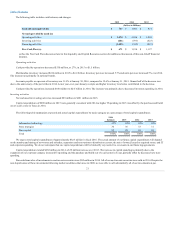

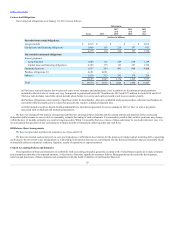

Insurance Reserve Estimates

We use a combination of insurance and self-insurance for a number of risks.

We retain the initial risk of $500,000 per occurrence in workers’ compensation claims and $250,000 per occurrence in general liability claims. We

record reserves for workers’ compensation and general liability claims which include the total amounts that we expect to pay for a fully developed loss and

related expenses, such as fees paid to attorneys, experts and investigators. The fully developed loss includes amounts for both reported claims and incurred,

but not reported losses.

We use a third-party actuary to estimate the liabilities associated with these risks. The actuary considers historical claims experience, demographic and

severity factors and actuarial assumptions to estimate the liabilities associated with these risks. As of January 30, 2016, estimated liabilities for workers’

compensation and general liability claims were approximately $45 million.

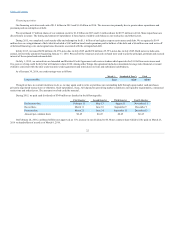

27