Honeywell 2013 Annual Report Download - page 48

Download and view the complete annual report

Please find page 48 of the 2013 Honeywell annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

|

|

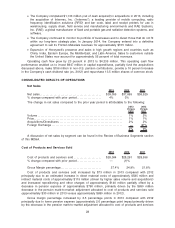

Commercial original equipment (OE) sales increased by 3 percent in 2013 compared to 2012.

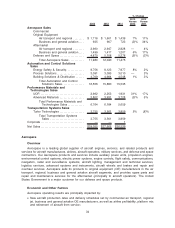

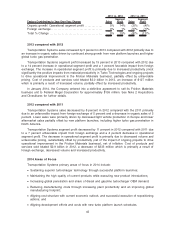

•Air transport and regional OE sales increased by 7 percent in 2013 driven by higher air transport

volumes, consistent with the OE Manufacturers’ (OEM) higher production rates, partially offset

by lower regional jet sales.

•Business and general aviation OE sales decreased by 3 percent in 2013 driven by an increase

in OEM Payments to business and general aviation customers, partially offset by strong demand

in the business jet mid to large cabin segment.

Commercial aftermarket sales increased by 2 percent in 2013 compared to 2012.

•Air transport and regional aftermarket sales were flat for 2013 primarily due to higher repair and

overhaul activities related to utilization, offset by lower spares volumes.

•Business and general aviation aftermarket sales increased by 6 percent in 2013 primarily due to

higher sales for retrofit, modifications and upgrades, partially offset by fewer repair and overhaul

activities.

Defense and space sales decreased by 5 percent in 2013 primarily due to U.S. government

program ramp downs and lower defense budget, partially offset by a royalty gain in the fourth

quarter.

Aerospace segment profit increased by 4 percent in 2013 compared with 2012 primarily due to an

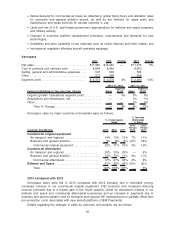

increase in operational segment profit driven by commercial sales growth, as discussed above,

including favorable pricing and productivity, net of inflation, partially offset by lower defense and space

sales, as discussed above. The segment margin impact from other factors was flat, which reflects the

net effect of a royalty gain in the fourth quarter, offset by the unfavorable impact from an increase in

OEM Payments. Cost of products and services sold totaled $8.8 billion in 2013, a decrease of

approximately $101 million from 2012 which is primarily a result of the factors discussed above

(excluding price).

2012 compared with 2011

Aerospace sales increased by 5 percent in 2012 compared with 2011 primarily due to an increase

in organic growth of 3 percent primarily due to increased commercial sales volume, a 1 percent

increase from acquisitions, net of divestitures, and a 1 percent increase in revenue related to an $88

million reduction in payments to business and general aviation OE manufacturers to partially offset

their pre-production costs associated with new aircraft platforms (OEM Payments).

Details regarding the changes in sales by customer end-markets are as follows:

Commercial original equipment (OE) sales increased by 19 percent (12 percent organic) in 2012

compared to 2011.

•Air transport and regional OE sales increased by 11 percent (11 percent organic) in 2012

primarily driven by higher sales to our OE customers, consistent with higher production rates,

and a favorable platform mix.

•Business and general aviation OE sales increased by 34 percent (15 percent organic) in 2012

driven by strong demand in the business jet end-market, favorable platform mix, growth from

acquisitions and the favorable 12 percent impact of the OEM Payments discussed above.

Commercial aftermarket sales increased by 8 percent in 2012 compared to 2011.

•Air transport and regional aftermarket sales increased by 4 percent for 2012 primarily due to

increased sales of spare parts and higher maintenance activity driven by an approximate 2

percent increase in global flying hours in 2012, increased sales of avionics upgrades, and

changes in customer buying patterns relating to maintenance activity in the first half of 2012.

•Business and general aviation aftermarket sales increased by 17 percent in 2012 primarily due

to increased sales of spare parts and revenue associated with maintenance service agreements

and a higher penetration in retrofit, modifications, and upgrades.

36