Honeywell 2013 Annual Report Download - page 101

Download and view the complete annual report

Please find page 101 of the 2013 Honeywell annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

|

|

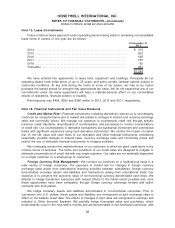

currency forward contracts. Changes in the forecasted non-functional currency cash flows due to

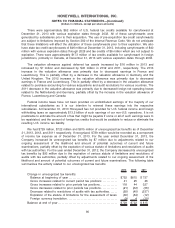

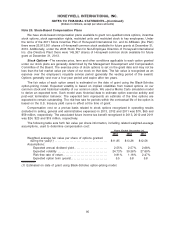

movements in exchange rates are substantially offset by changes in the fair value of the currency

forward contracts designated as hedges. Market value gains and losses on these contracts are

recognized in earnings when the hedged transaction is recognized. Open foreign currency exchange

forward contracts mature predominantly in the next twelve months. At December 31, 2013 and 2012,

we had contracts with notional amounts of $7,298 million and $8,506 million, respectively, to exchange

foreign currencies, principally the U.S. Dollar, Euro, Canadian Dollar, British Pound, Mexican Peso,

Indian Rupee, Chinese Renminbi, Czech Koruna, Hong Kong Dollar, Korean Won, Singapore Dollar,

Swiss Franc, United Arab Emirates Dirham, Swedish Krona, Thai Baht and Romanian Leu.

Commodity Price Risk Management—Our exposure to market risk for commodity prices can

result in changes in our cost of production. We primarily mitigate our exposure to commodity price risk

through the use of long-term, fixed-price contracts with our suppliers and formula price agreements

with suppliers and customers. We also enter into forward commodity contracts with third parties

designated as hedges of anticipated purchases of several commodities. Forward commodity contracts

are marked-to-market, with the resulting gains and losses recognized in earnings when the hedged

transaction is recognized. At December 31, 2013 and 2012, we had contracts with notional amounts of

$1 million and $17 million, respectively, related to forward commodity agreements, principally base

metals and natural gas.

Interest Rate Risk Management—We use a combination of financial instruments, including long-

term, medium-term and short-term financing, variable-rate commercial paper, and interest rate swaps

to manage the interest rate mix of our total debt portfolio and related overall cost of borrowing. At

December 31, 2013 and 2012, interest rate swap agreements designated as fair value hedges

effectively changed $1,700 million and $1,400 million, respectively, of fixed rate debt at rates of 3.96

and 4.09, respectively, to LIBOR based floating rate debt. Our interest rate swaps mature at various

dates through 2023.

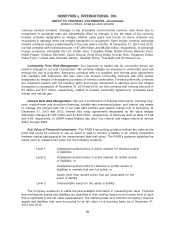

Fair Value of Financial Instruments—The FASB’s accounting guidance defines fair value as the

price that would be received to sell an asset or paid to transfer a liability in an orderly transaction

between market participants at the measurement date (exit price). The FASB’s guidance classifies the

inputs used to measure fair value into the following hierarchy:

Level 1 Unadjusted quoted prices in active markets for identical assets

or liabilities

Level 2 Unadjusted quoted prices in active markets for similar assets

or liabilities, or

Unadjusted quoted prices for identical or similar assets or

liabilities in markets that are not active, or

Inputs other than quoted prices that are observable for the

asset or liability

Level 3 Unobservable inputs for the asset or liability

The Company endeavors to utilize the best available information in measuring fair value. Financial

and nonfinancial assets and liabilities are classified in their entirety based on the lowest level of input

that is significant to the fair value measurement. The following table sets forth the Company’s financial

assets and liabilities that were accounted for at fair value on a recurring basis as of December 31,

2013 and 2012:

89

HONEYWELL INTERNATIONAL INC.

NOTES TO FINANCIAL STATEMENTS—(Continued)

(Dollars in millions, except per share amounts)