HSBC 2012 Annual Report Download - page 67

Download and view the complete annual report

Please find page 67 of the 2012 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

|

|

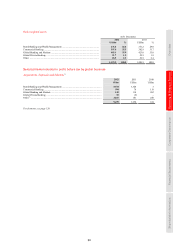

65

Overview Operating & Financial Review Corporate Governance Financial Statements Shareholder Information

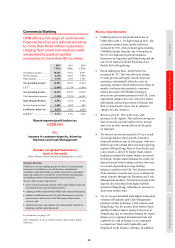

Commercial Banking

CMB offers a full range of commercial

financial services and tailored solutions

to more than three million customers

ranging from small and medium-sized

enterprises to publicly quoted

companies in more than 60 countries.

2012 2011 2010

US$m US$m US$m

Net interest income .......... 10,361 9,931 8,487

Net fee income ................. 4,470 4,291 3,964

Other income ................... 1,720 1,389 1,383

Net operating income21 .. 16,551 15,611 13,834

LICs76 ............................... (2,099) (1,738) (1,805)

Net operating income .... 14,452 13,873 12,029

Total operating expenses .. (7,598) (7,221) (6,831)

Operating profit/(loss) ... 6,854 6,652 5,198

Income from associates77 . 1,681 1,295 892

Profit/(loss) before tax ... 8,535 7,947 6,090

RoRWA66 ......................... 2.2% 2.2% 2.0%

Record reported profit before tax

US$8.5bn

9%

increase in customer deposits, driven by

Payments and Cash Management

Number one global trade finance

bank in the world

(Oliver Wyman Global Transaction Banking Survey 2012)

Strategic direction

CMB aims to be the banking partner of choice for international

businesses by building on our rich heritage, international

capabilities and relationships to enable connectivity and support

trade and capital flows around the world, thereby strengthening

our leading position in international business and trade.

We have four strategic imperatives:

• focus on faster-growing markets while connecting revenue and

investment flows with developed markets;

• capture growth in international SMEs and corporate businesses;

• enhance collaboration across all global businesses to provide

our customers with access to the full range of the Group’s

services; and

• simplify processes and enhance risk management controls by

adopting a global operating model.

For footnotes, see page 120.

The commentary is on a constant currency basis unless stated

otherwise.

Review of performance

• CMB reported a record profit before tax of

US$8.5bn in 2012, 7% higher than in 2011. On

a constant currency basis, profit before tax

increased by 10%. This included gains totalling

US$468m mainly from the sale of branches in

the US, the disposal of general insurance

businesses in Argentina and Hong Kong and the

sale of our shares in Global Payments Asia-

Pacific Ltd in Hong Kong.

• On an underlying basis, profit before tax

increased by 3%. This was driven by strong

revenue growth and higher income from our

associates, substantially offset by a rise in

operating expenses which reflected the effect of

notable cost items that included a customer

redress provision of US$268m relating to

interest rate protection products in the UK. Loan

impairment charges also rose, driven by higher

individually assessed provisions in Europe and

Rest of Asia-Pacific, and a rise in collective

charges in Latin America.

• Revenue grew by 10% in the year, with

increases in all regions. This reflected strong net

interest income growth, higher net fee income

and a rise in other income driven by the gains

on disposals.

• Net interest income increased by 8% as a result

of average balance sheet growth. Customer

loans and advances rose in all regions, with over

half this growth coming from our faster growing

regions of Hong Kong, Rest of Asia-Pacific and

Latin America, driven by higher trade-related

lending as demand for export finance increased.

In Europe, despite muted demand for credit, net

interest income from lending activities also rose

as a result of growth in average lending

balances, notably in the UK. Net interest income

from customer accounts rose as we continued to

attract deposits through our Payments and Cash

Management products. Net interest income from

deposits also benefited from higher liability

spreads in Hong Kong, reflecting an increase in

short-term interest rates.

• Net fee income benefited from higher transaction

volumes of Payments and Cash Management

products, mainly in Europe, Latin America and

Hong Kong. Net fee income from Global Trade

and Receivables Finance products also rose in

Hong Kong, due to continued demand for export

finance as we captured international trade and

capital flows, and in Europe as we continued

to expand our Trade and Commodity and

Structured Trade Finance offerings. In addition,