HSBC 2012 Annual Report Download - page 268

Download and view the complete annual report

Please find page 268 of the 2012 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

258 -

259

259 -

260

260 -

261

261 -

262

262 -

263

263 -

264

264 -

265

265 -

266

266 -

267

267 -

268

268 -

269

269 -

270

270 -

271

271 -

272

272 -

273

273 -

274

274 -

275

275 -

276

276 -

277

277 -

278

278 -

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

|

|

HSBC HOLDINGS PLC

Report of the Directors: Operating and Financial Review (continued)

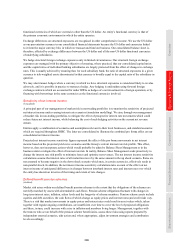

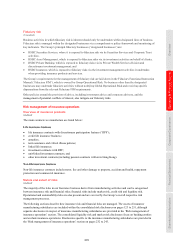

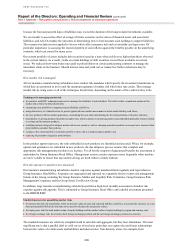

Risk > Appendix – Risk policies and practices > Market risk

266

Market risk is managed and controlled through limits approved by the GMB for HSBC Holdings and our

various global businesses. These limits are allocated across business lines and to the Group’s legal entities.

The management of market risk is principally undertaken in Global Markets, where 85% of the total value at risk of

HSBC Holdings (excluding Insurance) and almost all trading VAR resides, using risk limits approved by the GMB.

Limits are set for portfolios, products and risk types, with market liquidity being a primary factor in determining the

level of limits set. Group Risk, an independent unit within Group Head Office, is responsible for our market risk

management policies and measurement techniques. Each major operating entity has an independent market risk

management and control function which is responsible for measuring market risk exposures in accordance with the

policies defined by Group Risk, and monitoring and reporting these exposures against the prescribed limits on a

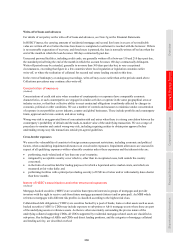

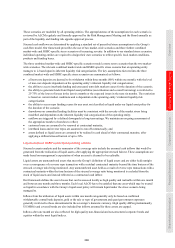

daily basis. The risk appetite is governed according to the framework illustrated below.

Chairman / CEO

Group Management Board

Risk Management Meeting

HSBC Holdings Board

Entity Risk

Management Committee

Principal Office Manager

Business / Desk / Trader

Group Traded Risk

General measures

Specific measures

Each operating entity is required to assess the market

risks arising on each product in its business and to

transfer them to either its local Global Markets unit

for management, or to separate books managed under

the supervision of the local ALCO. Our aim is to

ensure that all market risks are consolidated within

operations that have the necessary skills, tools,

management and governance to manage them

professionally. In certain cases where the market risks

cannot be fully transferred, we identify the impact of

varying scenarios on valuations or on net interest

income resulting from any residual risk positions.

Further details on the control and management

process for residual risks are provided on pages 268

to 269.

Sensitivity analysis

(Unaudited)

We use sensitivity measures to monitor the market

risk positions within each risk type, for example, the

present value of a basis point movement in interest

rates for interest rate risk. Sensitivity limits are set for

portfolios, products and risk types, with the depth of

the market being one of the principal factors in

determining the level of limits set.

Value at risk and stressed value at risk

(Audited)

VAR is a technique that estimates the potential losses on risk positions as a result of movements in market rates and

prices over a specified time horizon and to a given level of confidence. Stressed VAR is primarily used for

Regulatory Capital purposes but is integrated into the risk management process to facilitate efficient capital

management and to highlight possible high-risk positions based on previous market volatility.

Both the VAR and Stressed VAR models we use are based predominantly on historical simulation. These models

derive plausible future scenarios from past series of recorded market rates and prices, taking into account inter-

relationships between different markets and rates such as interest rates and foreign exchange rates. The models also

incorporate the effect of option features on the underlying exposures.

The historical simulation models used incorporate the following features:

• historical market rates and prices are calculated with reference to foreign exchange rates and commodity prices,

interest rates, equity prices and the associated volatilities;

• potential market movements utilised for VAR are calculated with reference to data from the past two years,

• (unaudited) potential market movements employed for stressed VAR calculations are based on a continuous one-

year period of stress for the trading portfolio; the choice of period (March 2008 to February 2009) is based on

the assessment at the Group level of the most volatile period in recent history; and