HSBC 2012 Annual Report Download - page 300

Download and view the complete annual report

Please find page 300 of the 2012 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

290 -

291

291 -

292

292 -

293

293 -

294

294 -

295

295 -

296

296 -

297

297 -

298

298 -

299

299 -

300

300 -

301

301 -

302

302 -

303

303 -

304

304 -

305

305 -

306

306 -

307

307 -

308

308 -

309

309 -

310

310 -

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

|

|

HSBC HOLDINGS PLC

Report of the Directors: Operating and Financial Review (continued)

Capital > Appendix to Capital > CRD IV end point

298

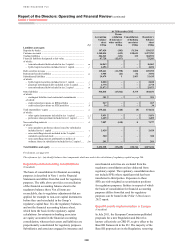

Market risk drivers – definitions and quantification

The RWA movement by key driver for market risk combines the credit risk drivers 5 and 6 into a single driver called

‘Movements in risk levels’. The market risk RWA driver called ‘Foreign exchange movements and other’ includes

foreign exchange movements and additional items which can not be reasonably assigned to any of the other drivers.

Basis of preparation of the estimated effect of the CRD IV end point applied to the 31 December

2012 position.

(Unaudited)

The table on page 289 presents a reconciliation of our reported core tier 1 and RWA position at 31 December 2012 to

the pro-forma estimated CET1 and estimated RWAs based on the Group’s interpretation of the draft July 2011

CRD IV legislation and/or guidance provided by the FSA and, in lieu of guidance, our current expectation of how

these draft 2011 rules will be updated by subsequent EU deliberations.

CRD IV has not yet become law and its provisions are subject to on-going negotiation and amendment. In addition,

formal Implementing Technical Standards (‘ITS’) due for issue by the EBA are still to be drafted and finalised,

leaving the CRD IV rules subject to significant interpretation. Despite the uncertainty around a number of areas

in the rules, our disclosures are based on the draft July 2011 CRD IV text. Pending finalisation of CRD IV, we have

not definitively upgraded the models and systems used to calculate capital numbers in a CRD IV environment which,

as a consequence, are subject to change. Consequently, the final CRD IV impact on the Group’s CET1 and RWAs

may be different from our current estimates.

The detailed basis of preparation is described below for items that are different from our current treatment under

Basel II. For individual immaterial holdings in banks, financial institutions and insurance that are, in aggregate,

above 10% of the Group’s CET1 capital, we have included specific short term management actions that could be

taken to negate the capital deduction. For other CRD IV proposals, additional management actions could also be

taken dependent upon the finalised rules and timing of implementation but, as such, have not been included.

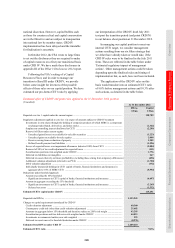

Regulatory adjustments applied to core tier 1 in respect of amounts subject to CRD IV treatment

Investments in own shares through the holding of composite products of which HSBC is a component

(exchange traded funds, derivatives, and index stock): the value of our holdings of own CET1 instruments,

where it is not already deducted under IFRSs, is deducted from CET1. Under CRD IV, deduction comprises not only

direct but also indirect, actual and contingent, banking and trading book gross long positions. Trading book positions

are calculated net of short positions only where there is no counterparty credit risk on these short positions (this

restriction does not apply to index positions). We have not recognised the benefit of non-index short positions, even

where they are executed with central counterparties or are fully collateralised. Under current rules, there is no

regulatory adjustment made on the amounts already deducted under IFRS rules.

Surplus non-controlling interest disallowed in CET1: non-controlling interests arising from the issue of common

shares by our banking subsidiaries receive limited recognition. The excess over a minimum of 7% of the CET1 of the

relevant subsidiary is not allowable in the Group’s CET1 to the extent it is attributable to minority shareholders.

Under current rules, there is no regulatory restriction applied to these items.

Unrealised gains/(losses) on available-for-sale debt securities: under CRD IV, there is no adjustment to remove

from CET1 capital unrealised gains and losses on available-for-sale debt securities. Under current FSA rules, these

are removed from capital (net of tax).

Unrealised gains on available-for-sale equities and reserves arising from revaluation of property: there is no

adjustment for unrealised gains and losses on reserves arising from the revaluation of property and on available-for-

sale equities. Under current FSA rules, unrealised net gains on these items are included in tier 2 capital (net of

deferred tax) and net losses are deducted from tier 1 capital.

Defined benefit pension fund liabilities: the amount of retirement benefit liabilities as reported on the balance sheet

is fully recognised in CET1 rather than being replaced by any committed funding plans as current FSA rules permit.

Excess of expected losses over impairment allowances deducted 100% from CET1: the amount of excess

expected loss over impairment allowance is deducted 100% from CET1. Under current FSA rules, this amount is

deducted 50% from core tier 1 (‘CT1’) and 50% from total capital.