HSBC 2012 Annual Report Download - page 43

Download and view the complete annual report

Please find page 43 of the 2012 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

|

|

41

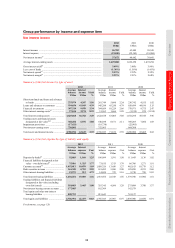

Overview Operating & Financial Review Corporate Governance Financial Statements Shareholder Information

contracts and investment and insurance contracts

with DPF.

The higher investment returns were largely the

result of positive equity market movements in 2012

compared with losses experienced during 2011

notably in Hong Kong, France and the UK. The gains

or losses on the financial assets designated at fair

value held to support these insurance and investment

contract liabilities are reported in ‘Net income from

financial instruments designated at fair value’.

The increase in liabilities to policyholders also

reflected the increase in new business written,

notably in Hong Kong and Brazil as explained under

‘Net earned insurance premiums’. This was partly

offset by a lower increase in reserves in France

attributable to the decline in net earned premiums,

and a decrease in Argentina due to the sale of the

general insurance business in May 2012.

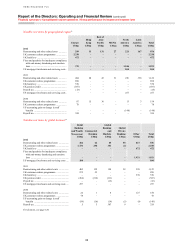

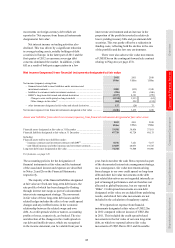

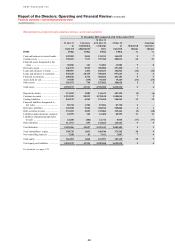

Loan impairment charges and other credit risk provisions

2012

US$m

2011

US$m

2010

US$m

Loan impairment charges

New allowances net of allowance releases ............................................................ 9,306 12,931 14,568

Recoveries of amounts previously written off ....................................................... (1,146) (1,426) (1,020)

8,160 11,505 13,548

Individually assessed allowances ............................................................................... 2,139 1,915 2,625

Collectively assessed allowances ............................................................................... 6,021 9,590 10,923

Impairment of available-for-sale debt securities ........................................................ 99 631 472

Other credit risk provisions/(recoveries) .................................................................... 52 (9) 19

Loan impairment charges and other credit risk provisions ........................................ 8,311 12,127 14,039

Reported loan impairment charges and other credit

risk provisions (‘LIC’s) fell from US$12bn to

US$8.3bn, a decrease of 31% compared with

2011. On an underlying basis they reduced from

US$10bn to US$8.0bn.

On a constant currency basis, they declined by

US$3.5bn or 30% compared with 2011. Collectively

assessed allowances were down by US$3.3bn and

credit risk provisions fell by US$456m, partly offset

by higher individually assessed impairment charges

of US$258m.

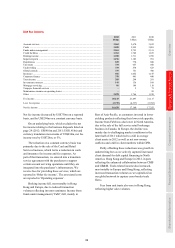

At 31 December 2012, the aggregate balance

of customer loan impairment allowances was

US$16bn. This represented 2% of gross loans

and advances to customers (net of reverse repos and

settlement accounts) in line with 31 December 2011.

The fall in collectively assessed impairment

allowances was most significant in RBWM in North

America due to the continued reduction in the CML

portfolios in run-off, and the sale of the Card and

Retail Services business. In addition, lower loan

impairment charges in Europe in RBWM were due

to improved credit quality as we continued to pro-

actively identify and monitor customers facing

financial hardship and focused our lending growth

on higher quality assets, notably in the UK. These

factors were partly offset by higher loan impairment

charges and other credit risk provisions in Latin

America which were driven by increased delinquency

rates in RBWM and CMB, mainly in Brazil.

Impairment of available-for-sale debt securities

reduced, mainly in Europe, due to lower charges on

available-for-sale ABSs and on Greek sovereign

debt, partly offset by an increase in Rest of Asia-

Pacific due to a charge on an available-for-sale debt

security in GB&M.

Individually assessed impairment allowances

increased by 14%, primarily in Europe in CMB,

reflecting challenging economic conditions in the

UK, Greece, Spain and Turkey. In addition, higher

individually assessed impairments in Latin America

mainly related to a single exposure in Brazil.

LICs declined in North America, primarily in

the CML portfolio, as well as in Europe, Hong Kong

and the Middle East and North Africa. The decrease

was partly offset by an increase in Latin America

and Rest of Asia-Pacific.

In North America, LICs fell by 51% to

US$3.5bn. Within this, loan impairment charges

fell by US$1.3bn following the sale of the Card

and Retail Services business. Loan impairment

charges in our CML business in the US fell by 48%

to US$2.6bn, driven by lower lending balances, as

we continued to run off the portfolio, and lower

delinquency levels. Loan impairment charges

continued to be adversely affected by delays in

expected cash flows from mortgage loans due, in

part, to delays in foreclosure processing, although

the effects were less pronounced than in 2011. These

decreases were partly offset by an adjustment made