HSBC 2012 Annual Report Download - page 12

Download and view the complete annual report

Please find page 12 of the 2012 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

|

|

HSBC HOLDINGS PLC

Report of the Directors: Overview (continued)

Group Chief Executive’s Business Review

10

and Cash Management products. In addition,

Retail Banking and Wealth Management

experienced revenue growth across all faster-

growing regions, in particular Hong Kong and

Latin America. These factors were partially

offset by lower revenue in Global Private

Banking, as we focused on repositioning our

business model and target client base.

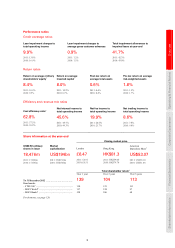

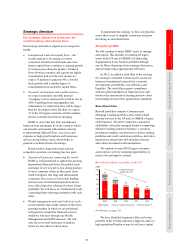

• We achieved growth in reported loans and

advances to customers of more than US$57bn

during the year, notably in residential mortgages

and term and trade-related lending. Customer

deposits increased by over US$86bn, allowing

us to maintain a strong ratio of customer

advances to customer accounts of 74.4%.

• Underlying costs were US$4.3bn higher than in

2011 including payments of US$1.9bn made as

part of the settlement of the investigations into

past inadequate compliance with anti-money

laundering and sanctions laws, additional

provisions in respect of UK customer redress

programmes of US$1.4bn, and a credit in 2011

of US$0.6bn relating to defined benefit pension

obligations in the UK which did not recur.

Operating expenses also increased due to

inflationary pressures, for example, on wages

and salaries, in certain of our Latin American

and Asian markets. Other increases arose from

investment in strategic initiatives including

certain business expansion projects, enhanced

processes and technology capabilities, and

increased investment in regulatory and

compliance infrastructure primarily in the US.

• The reported cost efficiency ratio deteriorated

from 57.5% to 62.8% and from 63.4% to 66.0%

on an underlying basis, as a result of higher

notable cost items, as described above.

• Return on equity was 8.4%, down from

10.9% in 2011, primarily reflecting the adverse

movement in fair value of own debt attributable

to movements in credit spreads, a higher tax

charge and higher average shareholders’ equity.

Similarly, the Group’s pre-tax return on average

risk-weighted assets (‘RoRWA’) for 2012 was

1.8% or 1.5% on an underlying basis. Adjusting

for the negative returns on US consumer finance

business and legacy credit in Global Banking

and Markets, the remainder of the Group

achieved a RoRWA of 1.9% in 2012 and 2.1%

in 2011.

• The core tier 1 ratio increased during the year

from 10.1% at the end of 2011 to 12.3%. This

increase was driven by capital generation and a

reduction in risk-weighted assets following

business disposals.

• The Basel III capital rules began their staged

6-10 year implementation in some parts of the

world in January 2013. Nevertheless, the FSA

has set our 2013 capital target calculation on

a Basel III end point basis. This effectively

accelerates our implementation of Basel III

by several years relative to European regulations

and other global banks. Consistent with this, we

now operate to an internal capital target set on a

Basel III end point basis of 9.5%-10.5%.

• Profit attributable to ordinary shareholders was

US$13.5bn, of which US$8.3bn was declared in

dividends in respect of the year. This compared

with US$2.9bn of variable pay awarded (net of

tax) to our employees for 2012.

• Dividends per ordinary share declared in respect

of 2012 were US$0.45, an increase of 10%

compared with 2011, with a fourth interim

dividend for 2012 of US$0.18 per ordinary share.

Global standards

As a global organisation which trades on its

international connectivity, we recognise that we

have a responsibility to play a part in protecting

the integrity of the financial system. In order to

do this effectively, in April 2012 we committed to

implementing industry-leading controls to increase

our ability to combat financial crime.

The highest compliance standards are being

adopted and enforced across HSBC and our

Compliance function has already been strengthened

considerably. More than 3,500 people are now

employed globally to work on compliance and the

cost of the Compliance function has approximately

doubled since 2010 to more than US$500m. We

have created and recruited externally for two new

Compliance leadership roles – Global Head of

Regulatory Compliance and Head of

Group Financial Crime Compliance – and appointed

a number of senior staff with extensive experience of

handling relevant international legal and financial

issues. A review of ‘Know Your Customer’ files is

under way across the entire Group and an enhanced

global sanctions policy has been devised to ensure

that we do not do business with key illicit actors

anywhere, in any currency. In addition, we have

moved to protect HSBC from the risks inherent in

bearer shares by curtailing the ability of clients using

bearer share companies to open accounts or transact

with HSBC.