HSBC 2012 Annual Report Download - page 252

Download and view the complete annual report

Please find page 252 of the 2012 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

256 -

257

257 -

258

258 -

259

259 -

260

260 -

261

261 -

262

262 -

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

|

|

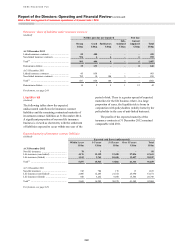

HSBC HOLDINGS PLC

Report of the Directors: Operating and Financial Review (continued)

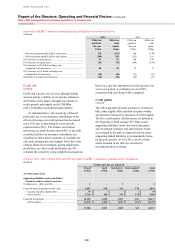

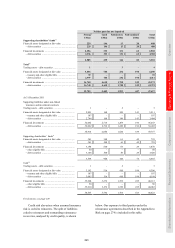

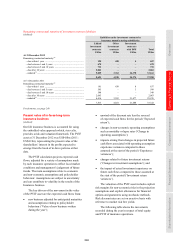

Risk > Footnotes

250

13 Included in this category are loans of US$2.3bn (2011: US$2.9bn) that have been re-aged once and were less than 60 days past due at

the point of re-age. These loans are not classified as impaired following re-age due to the overall expectation that these customers will

perform on the original contractual terms of their borrowing in the future.

14 ‘Impaired loans and advances’ are those classified as CRR 9, CRR 10, EL 9 or EL 10, retail loans 90 days or more past due, unless

individually they have been assessed as not impaired (see page 156, ‘Past due but not impaired gross financial instruments’) and

renegotiated loans and advances meeting the criteria to be disclosed as impaired (see page 162).

15 ‘Collectively assessed loans and advances’ comprise homogeneous groups of loans that are not considered individually significant, and

loans subject to individual assessment where no impairment has been identified on an individual basis, but on which a collective

impairment allowance has been calculated to reflect losses which have been incurred but not yet identified.

16 ‘Collectively assessed loans and advances not impaired’ are those classified as CRR1 to CRR8 and EL1 to EL8 but excluding retail

loans 90 days past due and renegotiated loans and advances meeting the criteria to be disclosed as impaired.

17 ‘Collectively assessed impairment allowances’ are allocated to geographical segments based on the location of the office booking the

allowances or provisions. Consequently, the collectively assessed impairment allowances booked in Hong Kong may cover assets

booked in branches located outside Hong Kong, principally in Rest of Asia-Pacific, as well as those booked in Hong Kong.

18 Included within ‘Exchange and other movements’ is US$0.8bn of impairment allowances reclassified to held for sale (2011: US$1.6bn).

19 Net of repo transactions, settlement accounts and stock borrowings.

20 As a percentage of loans and advances to banks and loans and advances to customers, as applicable.

21 ‘Currency translation’ is the effect of translating the results of subsidiaries and associates for the previous year at the average rates of

exchange applicable in the current year.

22 Negative numbers are favourable: positive numbers are unfavourable.

23 Equity securities not included.

24 ‘First lien residential mortgages’ include Hong Kong Government Home Ownership Scheme loans of US$3.2bn at 31 December 2012

(2011: US$3.3bn). Where disclosed, earlier comparatives were 2010: US$3.5bn; 2009: US$3.5bn; 2008: US$3.9bn.

25 The impairment allowances on loans and advances to banks in 2012 relate to the geographical regions, Europe, North America, and

Middle East and North Africa. (2011: Europe and North America).

26 Carrying amount of the net principal exposure.

27 Total includes holdings of ABSs issued by The Federal Home Loan Mortgage Corporation (‘Freddie Mac’) and The Federal National

Mortgage Association (‘Fannie Mae’).

28 ‘Directly held’ includes assets held by Solitaire where we provide first loss protection and assets held directly by the Group.

29 ‘Effect of impairments’ represents the reduction or increase in the reserve on initial impairment and subsequent reversal of impairment

of the assets.

30 The gross principal is the redemption amount on maturity or, in the case of an amortising instrument, the sum of the future redemption

amounts through the residual life of the security.

31 Credit default swap (‘CDS’) gross protection is the gross principal of the underlying instrument that is protected by CDSs.

32 Net principal exposure is the gross principal amount of assets that are not protected by CDSs. It includes assets that benefit from

monoline protection, except where this protection is purchased with a CDS.

33 Net exposure after legal netting and any other relevant credit mitigation prior to deduction of the credit valuation adjustment.

34 Cumulative fair value adjustment recorded against exposures to OTC derivative counterparties to reflect their creditworthiness.

35 Funded exposures represent the loan amount advanced to the customer, less any fair value write-downs, net of fees held on deposit.

36 Unfunded exposures represent the contractually committed loan facility amount not yet drawn down by the customer, less any fair value

write-downs, net of fees held on deposit.

Eurozone exposures

37 Our available-for-sale holdings in sovereign and agency debt of Italy and Spain include debt held to support insurance contracts which

provide discretionary profit participation to policyholders. For such contracts, unrealised movements in liabilities are recognised in

other comprehensive income, following the treatment of the unrealised movements on related available-for-sale assets. To the extent

that the movements are matched, no movement in the available-for-sale reserve is recognised. For those available-for-sale debt

instruments described above that are not held to support insurance contracts which provide discretionary profit participation to

policyholders, the available-for-sale reserves at 31 December 2012 were insignificant.

38 ‘In-country liabilities’ in Italy include liabilities issued under local law but booked outside the country.

Liquidity and funding

39 The most favourable metrics are a smaller advances to core funding and larger stressed one-month and three-month coverage ratios.

40 The HSBC UK entity shown comprises three legal entities; HSBC Bank plc (including SPEs consolidated by HSBC Bank plc for

Financial Statement purposes, HFC Bank Ltd, and all overseas branches), Marks and Spencer Financial Services Limited and HSBC

Trust Company (UK) Limited, managed as a single operating entity, in line with the application of UK liquidity regulation as agreed

with the UK FSA.

41 The Hongkong and Shanghai Banking Corporation represents the bank in Hong Kong including all overseas branches. Each branch is

monitored and controlled for liquidity and funding risk purposes as a stand-alone operating entity.

42 The HSBC USA principal entity shown represents the HSBC USA Inc consolidated group; predominantly HSBC USA Inc and HSBC

Bank USA, NA. The HSBC USA Inc consolidated group is managed as a single operating entity.

43 The total shown for other principal HSBC operating entities represents the combined position of all the other operating entities

overseen directly by the Risk Management Meeting of the GMB.

44 Estimated liquidity value represents the expected realisable value of assets prior to management assumed haircuts.

45 The undrawn balance for the five largest committed liquidity facilities provided to customers other than facilities to conduits.

46 The undrawn balance for the total of all committed liquidity facilities provided to the largest market sector, other than facilities to

conduits.

47 As a result of the significant level of disposal groups held for sale at 31 December 2012, the financial liabilities of the disposal groups

held for sale has been separately shown in the table. For further details of the disposal groups held for sale, refer to Note 30 on the

Financial Statements.