HSBC 2012 Annual Report Download - page 150

Download and view the complete annual report

Please find page 150 of the 2012 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

|

|

HSBC HOLDINGS PLC

Report of the Directors: Operating and Financial Review (continued)

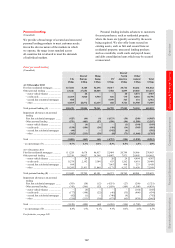

Risk > Credit risk > Personal lending

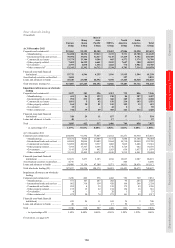

148

In 2012, the credit quality of the majority of

our personal lending portfolios improved, reflecting

the continued low levels of interest rates and strong

customer repayments in many markets, as well

as actions taken in previous years to tighten our

lending criteria and focus on higher quality and

secured assets.

In the US, the origination of new personal

lending was limited as we have discontinued all

new consumer finance real estate lending following

the closure of the consumer finance distribution

network. Customer lending balances across HSBC

Finance portfolios continued to decline and, in May

and August 2012 respectively, we completed the

sales of the Card and Retail Services business and

non-strategic branches, in the US. We continue to

explore options to accelerate the liquidation of the

CML portfolio and, to this effect, reclassified certain

non-real estate personal loan balances, net of

impairment allowances, to ‘Assets held for sale’

as we actively marketed this portfolio.

The commentary that follows is on a constant

currency basis.

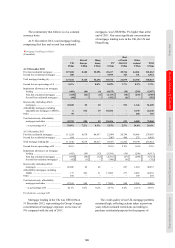

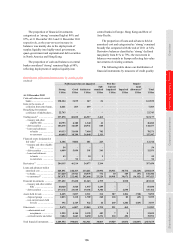

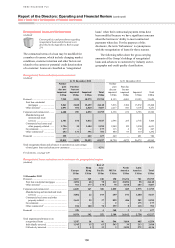

At 31 December 2012, the Group’s exposure

to personal lending was US$415bn, 3% higher than

at 31 December 2011, reflecting a rise in first lien

residential mortgage lending, partly offset

by a reduction in other personal lending. Loan

impairment allowances on our personal lending

portfolios were US$8.2bn compared with US$9.8bn

at the end of 2011, while the ratio of loan

impairment allowances to total personal lending

reduced from 2.4% at 31 December 2011 to 2.0%

at 31 December 2012. This decline reflected

volume and performance-based improvements,

predominantly in our US portfolios, due to the

continued run-off of the CML portfolio as well as

the reclassification of impairment allowances on

non-real estate personal loan balances to ‘Assets

held for sale’. We also continued to focus on

growing our lower-risk residential mortgage

portfolios in the UK, Hong Kong and rest of Asia-

Pacific, where our loss experience and impairment

allowance requirements are typically lower.

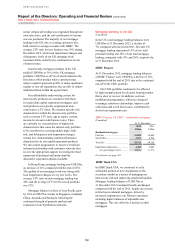

Loan impairment charges in our personal

lending portfolios were US$5.4bn in 2012,

US$3.8bn or 41% lower than in 2011 and

representing 66% of the overall Group’s LICs.

The decline was predominantly in the US reflecting

the reduction in balances in the CML portfolio and

the sale of the Card and Retail Services business in

May 2012.

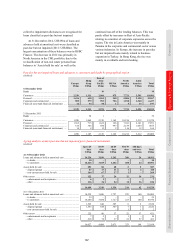

At 31 December 2012, total personal lending

increased by US$13.7bn reflecting growth in first

lien residential mortgages, notably in the UK, Hong

Kong and Rest of Asia-Pacific. Balances in the

UK increased following the success of marketing

campaigns and competitive pricing. The rise in Hong

Kong reflected the low interest rate environment and

active property market, whereas growth in the

Rest of Asia-Pacific, mainly in Singapore, mainland

China, Australia and Malaysia, reflected the

continued strength of property markets and

expansion of our distribution network.

Total personal lending balances in the US at

31 December 2012 were US$57bn, a decrease of

15% compared with the end of 2011. The decline

reflected the run-off of our CML portfolio, which

also fell due to the reclassification of non-real estate

personal loan balances to ‘Assets held for sale’.

In Latin America, personal lending decreased by

4% compared with 31 December 2011, following a

reduction in other personal lending in Brazil, where

we managed down our exposure to non-strategic

portfolios and focused on higher quality lending

including first lien residential mortgage lending.

This complemented a range of corrective actions,

including improving our collections capabilities,

reducing third party originations and improving

credit scoring models. These actions were

implemented to limit our exposure to further market

weakness following a rise in delinquency in 2011

which continued in 2012. We also reclassified

lending balances in Colombia, Paraguay and Peru to

‘Assets held for sale’.

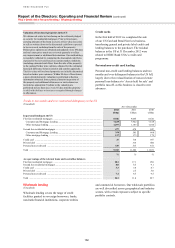

Mortgage lending

(Unaudited)

We offer a wide range of mortgage products

designed to meet customer needs, including capital

repayment, interest-only, affordability and offset

mortgages.

Group credit policy prescribes the range of

acceptable residential property loan-to-value

(‘LTV’) thresholds with the maximum upper limit

for new loans set between 75% and 95%. Specific

LTV thresholds and debt-to-income ratios are

managed at regional and country levels and,

although the parameters must comply with Group

policy, strategy and risk appetite, they differ in the

various locations in which we operate to reflect the

local economic and housing market conditions,

regulations, portfolio performance, pricing and other

product features.