HSBC 2012 Annual Report Download - page 152

Download and view the complete annual report

Please find page 152 of the 2012 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

|

|

HSBC HOLDINGS PLC

Report of the Directors: Operating and Financial Review (continued)

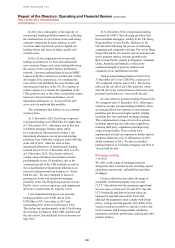

Risk > Credit risk > Personal lending

150

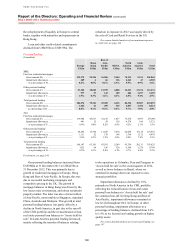

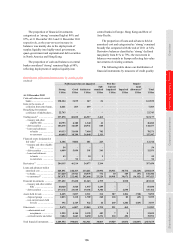

rental. Almost all lending was originated through our

own sales force, and the self-certification of income

was not permitted. The majority of our mortgage

lending in the UK was to existing customers who

held current or savings accounts with HSBC. The

average LTV ratio for new business was 59% during

December 2012, while loan impairment charges and

delinquency levels in our UK mortgage book

remained stable, aided by the continued low levels

of interest rates.

Interest-only mortgage products in the UK

totalled US$50bn or 39% of the UK mortgage

portfolio, US$23bn or (47%) of which related to the

first direct offset product where customers may

adopt a capital repayment profile or make significant

regular or one-off repayments, but are able to redraw

additional funds within the agreed limit.

Our affordability underwriting criteria for

interest-only products are consistent with those

for equivalent capital repayment mortgages, and

such products are typically originated at more

conservative LTV ratios. We monitor specific risk

characteristics within the interest-only portfolio,

such as current LTV ratio, age at expiry, current

income levels and credit bureau scores. There

are currently no concentrations of higher risk

characteristics that cause the interest-only portfolio

to be considered as carrying unduly high credit

risk, and delinquency and impairment charges

remain low, demonstrating similar performance

characteristics to our capital repayment products.

We run contact programmes to ensure we build an

informed relationship with customers whereby they

receive the appropriate support in meeting the final

repayment of principal and understand the

alternative repayment options available.

In Hong Kong, mortgage lending was US$52bn,

an increase of 11% compared with the end of 2011.

The quality of our mortgage book was strong with

loan impairment charges at very low levels. The

average LTV ratio on new mortgage lending was

48% and the average LTV for the overall portfolio

was 32%.

Mortgage balances in Rest of Asia-Pacific grew

by 10% to US$37bn, mainly in Singapore, mainland

China, Australia and Malaysia reflecting the

continued strength of property markets and

expansion of our distribution networks.

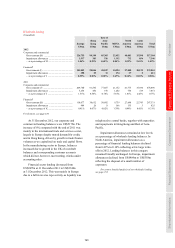

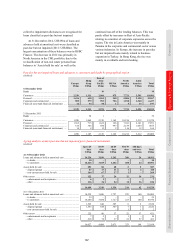

Mortgage lending in the US

(Unaudited)

In the US, total mortgage lending balances were

US$55bn at 31 December 2012, a decline of

7% compared with the end of 2011. Overall, US

mortgage lending represented 13% of our total

personal lending and 18% of our total mortgage

lending, compared with 15% and 20%, respectively,

at 31 December 2011.

HSBC Finance

At 31 December 2012, mortgage lending balances

at HSBC Finance were US$39bn, a decline of 12%

compared with the end of 2011 due to the continued

run-off of the CML portfolio.

Our CML portfolio continued to be affected

by high unemployment levels and a housing market

that is slow to recover. In addition, our loan

modification programmes, which are designed

to manage customer relationships, improve cash

collections and avoid foreclosure, contributed to

slower loan repayment rates.

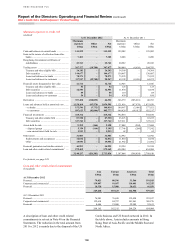

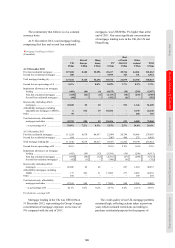

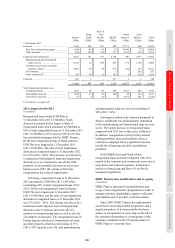

HSBC Finance US CML6 – residential mortgages

(Unaudited)

At 31 December

2012 2011

US$m US$m

Residential mortgages

First lien ....................................... 35,092 39,608

Second lien ................................... 3,651 4,520

Total (A) ...................................... 38,743 44,128

Impairment allowances ................ 4,480 5,088

– as a percentage of (A) ........... 11.6% 11.5%

For footnote, see page 249.

HSBC Bank USA

In HSBC Bank USA, we continued to sell a

substantial portion of new originations to the

secondary market as a means of managing our

interest rate risk and improving structural liquidity.

Mortgage lending balances of US$17bn at

31 December 2012 remained broadly unchanged

compared with the end of 2011, despite an increase

in first lien residential mortgages, driven by

increased origination to our Premier customers

including higher balances of adjustable-rate

mortgages. This was offset by a decline in other

mortgages.