HSBC 2012 Annual Report Download - page 59

Download and view the complete annual report

Please find page 59 of the 2012 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

|

|

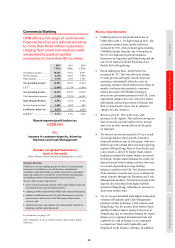

57

Overview Operating & Financial Review Corporate Governance Financial Statements Shareholder Information

possible that the outcomes in the next financial year

could differ from the assumptions used, and this

could result in a material adjustment to the carrying

amount of financial instruments measured at fair

value.

Deferred tax assets

Our accounting policy for the recognition of deferred

tax assets is described in Note 2s on the Financial

Statements. The recognition of a deferred tax asset

relies on an assessment of the probability and

sufficiency of future taxable profits, future reversals

of existing taxable temporary differences and

ongoing tax planning strategies.

The most significant judgements concern the US

deferred tax asset, given the recent history of losses

in our US operations. The net US deferred tax asset

amounted to US$4.6bn or 61% (2011: US$5.2bn;

68%) of deferred tax assets recognised on the

Group’s balance sheet. These judgements take into

consideration the reliance placed on the use of tax

planning strategies.

The most significant tax planning strategy is the

retention of capital in our US operations to ensure

the realisation of the deferred tax assets. The

principal strategy involves generating future taxable

profits through the retention of capital in the US in

excess of normal regulatory requirements in order

to reduce deductible funding expenses or otherwise

deploy such capital or increase levels of taxable

income. Management expects that, with this strategy,

the US operations will generate sufficient future

profits to support the recognition of the deferred

tax assets. If HSBC Holdings were to decide not to

provide this ongoing support, the full recovery of the

deferred tax asset may no longer be probable and

could result in a significant reduction of the deferred

tax asset which would be recognised as a charge in

the income statement.

Provisions

The accounting policy for provisions is described in

Note 2w on the Financial Statements. Note 32 on the

Financial Statements discloses the major categories

of provisions recognised. The closing balance of

provisions amounted to US$5.3bn (2011:

US$3.3bn), of which US$1.7bn (2011: US$1.5bn)

relates to legal proceedings and regulatory matters

and US$2.4bn (2011: US$1.1bn) relates to customer

remediation.

Judgement is involved in determining whether

a present obligation exists, and in estimating the

probability, timing and amount of any outflows.

Professional expert advice is taken on litigation

provisions, property provisions (including onerous

contracts) and similar liabilities.

Provisions for legal proceedings and regulatory

matters typically require a higher degree of

judgement than other types of provisions. When

cases are at an early stage, accounting judgements

can be difficult because of the high degree of

uncertainty associated with determining whether a

present obligation exists, and estimating the

probability and amount of any outflows that may

arise. As matters progress through various stages

of development, management and legal advisers

evaluate on an ongoing basis whether provisions

should be recognised and their estimated amounts,

revising previous judgements and estimates as

appropriate. At more advanced stages, it is typically

possible to make judgements and estimates around

a better defined set of possible outcomes. However,

such judgements can be very difficult and the

amount of any provision can be very sensitive to

the assumptions used. There could be a wide range

of possible outcomes for any pending legal

proceedings, investigations or inquiries. As a result,

it is often not practicable to quantify a range of

possible outcomes for individual matters. It is also

not practicable to meaningfully quantify ranges

of potential outcomes in aggregate for these types

of provisions because of the diverse nature and

circumstances of such matters and the wide range of

uncertainties involved. For a detailed description of

the nature of uncertainties and assumptions and the

effect on the amount and timing of possible cash

outflows on material matters, see Note 43 on the

Financial Statements.

Provisions for customer remediation also require

significant levels of estimation and judgement. The

amounts of provisions recognised depend on a

number of different assumptions, for example, the

volume of inbound complaints, the projected period

of inbound complaint volumes, the decay rate of

complaint volumes, the population identified as

systemically mis-sold and the number of policies per

customer complaint.

In view of the inherent uncertainties and the

high level of subjectivity involved in the recognition

and measurement of provisions, it is possible that the

outcomes in the next financial year could differ from

those on which management’s estimates are based,

resulting in materially different amounts of

provisions recognised and outflows of economic

benefits from those estimated by management for

the purposes of the 2012 Financial Statements.