HSBC 2012 Annual Report Download - page 156

Download and view the complete annual report

Please find page 156 of the 2012 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

|

|

HSBC HOLDINGS PLC

Report of the Directors: Operating and Financial Review (continued)

Risk > Credit risk > Wholesale lending / Credit quality of financial instruments

154

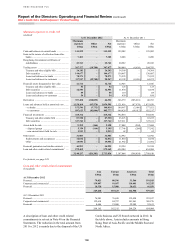

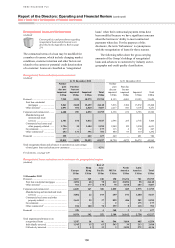

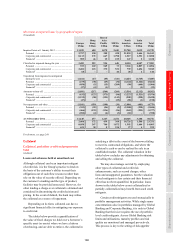

Corporate and commercial

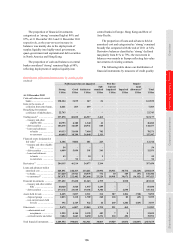

Corporate and commercial lending, excluding

commercial real estate and other property-related

lending, increased from US$365bn at 31 December

2011 to US$400bn at 31 December 2012.

At 31 December 2012, this represented 39%

of total gross loans and advances to customers,

compared with 38% at 31 December 2011. The

growth was mainly in the international trade and

services sector, where balances mainly increased

in Europe despite muted demand for credit and, in

Hong Kong, driven by growth in trade finance

volumes as we capitalised on trade and capital flows.

In the manufacturing sector, balances increased in

Europe due to growth in the UK of overdraft balances

and corresponding customer accounts which did not

meet netting criteria under accounting rules.

The aggregate of our commercial real estate

and other property-related lending was US$117bn

at 31 December 2012, 3% higher than at 31 December

2011, representing 12% of total loans and advances to

customers. This growth was mainly in Hong Kong,

where demand for funds remained strong despite a

degree of market stabilisation after a sustained period

of buoyancy in the property investment and property

development sectors. Commercial real estate and

other property-related lending also grew in North

America due to an increase in originations in

commercial mortgages, which reflected our continued

focus on expanding our core offering to gain a larger

presence in key growth markets, including the West

Coast, Southeast and Midwest of the US.

For information on refinancing in commercial

real estate lending, see page 128.

Financial (non-bank)

Financial (non-bank) lending decreased from

US$86bn at 31 December 2011 to US$81bn at

31 December 2012. This was mainly in Europe due

to a decline in reverse repo activity, partly offset

by higher balances in North America, due to an

increase in reverse repo balances in Canada, and

in Hong Kong and Rest of Asia-Pacific, driven by

an increase in loans drawn by financial planning

companies, leasing companies and insurance

companies reflecting higher demand for funds

from a small number of corporates.

Loans and advances to banks

Loans and advances to banks decreased from

US$181bn at 31 December 2011 to US$153bn at

31 December 2012. This was mainly driven by

maturities and repayments in Hong Kong together

with a decline in reverse repos in Europe reflecting, in

part, the redeployment of liquidity to central banks.

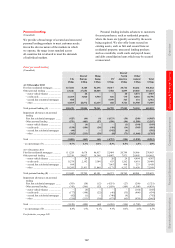

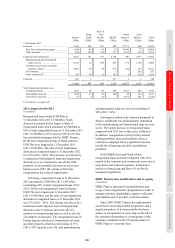

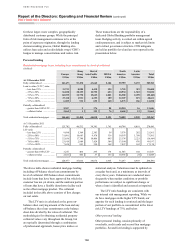

Credit quality of financial instruments

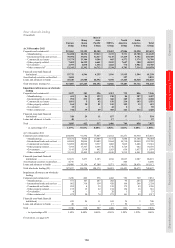

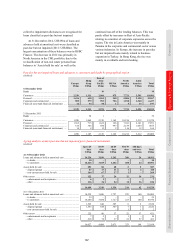

(Audited)

A summary of our current policies and

p

ractices regarding the credit quality of

f

inancial instruments is provided in the

Appendix to Risk on page 253.

The five classifications describing the credit

quality of our lending, debt securities portfolios

and derivatives are defined on page 253. Additional

credit quality information in respect of our

consolidated holdings of ABSs is provided

on page 259.

For the purpose of the following disclosure,

retail loans which are past due up to 89 days and are

not otherwise classified as impaired in accordance

with our disclosure convention (see page 253), are

not disclosed within the expected loss (‘EL’) grade

to which they relate, but are separately classified as

past due but not impaired.

2012 compared with 2011

(Unaudited)

We assess credit quality on all financial instruments

which are subject to credit risk, as shown in the table

on page 155. The balance of these financial

instruments was US$2,516bn at 31 December 2012,

an increase of 4% over 2011, of which US$1,690bn

or 67% was classified as ‘strong’. This percentage

declined marginally compared with 68% at

31 December 2011. The proportion of financial

instruments classified as ‘good’ remained broadly

stable at 16% and the proportion of ‘satisfactory’

balances increased marginally from 12% to 14%.

The proportion of ‘sub-standard’ financial

instruments remained low at 2% in both 2012

and 2011.

The proportion of trading assets classified as

‘strong’ declined from 75% to 65%. Overall trading

assets rose, largely in Europe, due to an increase in

holdings of debt securities from 2011’s subdued

levels which, coupled with the downgrading of

certain eurozone countries, resulted in an absolute

and relative increase in debt securities classified as

‘good’. In addition, holdings of ‘strong’ treasury and

other eligible bills fell both absolutely and relative to

the rest of trading assets primarily in Hong Kong due

to maturities without replacement of government

bonds, while increased levels of reverse repo and

stock lending balances with customers increased

the proportion of ‘good’ and ‘satisfactory’

classifications compared with ‘strong’.