HSBC 2012 Annual Report Download - page 296

Download and view the complete annual report

Please find page 296 of the 2012 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

286 -

287

287 -

288

288 -

289

289 -

290

290 -

291

291 -

292

292 -

293

293 -

294

294 -

295

295 -

296

296 -

297

297 -

298

298 -

299

299 -

300

300 -

301

301 -

302

302 -

303

303 -

304

304 -

305

305 -

306

306 -

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

|

|

HSBC HOLDINGS PLC

Report of the Directors: Operating and Financial Review (continued)

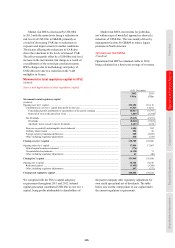

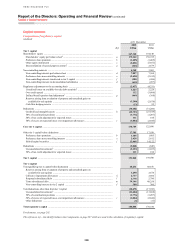

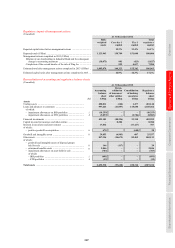

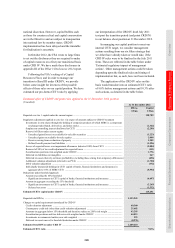

Capital > Appendix to Capital > Capital measurement and allocation

294

Risk-weighted asset targets

Top-down RWA targets are established for the global business lines, in accordance with the Group’s strategic

direction and risk appetite. As these targets are deployed to lower levels of management, action plans for

implementation are developed. These may include growth strategies; active portfolio management; restructuring;

business and/or customer-level reviews; RWA efficiency and optimisation initiatives and risk-mitigation. Our capital

management process is articulated in the annual Group capital plan which is approved by the Board.

RWA targets are approved by the GMB on an annual basis and business performance against them is monitored

through regular reporting to the Group ALCO. The management of capital deductions is also addressed in the RWA

monitoring framework through additional notional charges for these items.

A range of analysis is employed in the RWA monitoring framework to identify the key drivers of movements in

the position, such as book size and book quality. Particular attention is paid to identifying and segmenting items

within the day-to-day control of the business and those items that are driven by changes in risk models or regulatory

methodology.

Capital generation

HSBC Holdings is the primary provider of equity capital to its subsidiaries and also provides them with non-equity

capital where necessary. These investments are substantially funded by HSBC Holdings’ own capital issuance and

profit retention. As part of its capital management process, HSBC Holdings seeks to maintain a prudent balance

between the composition of its capital and its investment in subsidiaries.

Capital measurement and allocation

(Unaudited)

The FSA supervises HSBC on a consolidated basis and therefore receives information on the capital adequacy of,

and sets capital requirements for, the Group as a whole. Individual banking subsidiaries are directly regulated by their

local banking supervisors, who set and monitor their capital adequacy requirements. In 2012, we calculated capital at

a Group level using the Basel II framework as amended for CRD III, commonly known as Basel 2.5.

Our policy and practice in capital measurement and allocation at Group level is underpinned by the Basel II rules and

Basel III proposals. However, local regulators are at different stages of implementation and some local reporting,

notably in the US, is still on a Basel I basis. In most jurisdictions, non-banking financial subsidiaries are also subject

to the supervision and capital requirements of local regulatory authorities.

Basel II is structured around three ‘pillars’: minimum capital requirements, supervisory review process and market

discipline. The CRD implemented Basel II in the EU and the FSA then gave effect to the CRD by including the

latter’s requirements in its own rulebooks.

Regulatory capital

For regulatory purposes, our capital base is divided into three main categories, namely core tier 1, other tier 1 and tier

2, depending on the degree of permanency and loss absorbency exhibited.

• core tier 1 capital comprises shareholders’ equity and related non-controlling interests. The book values of

goodwill and intangible assets are deducted from core tier 1 capital and other regulatory adjustments are made

for items reflected in shareholders’ equity which are treated differently for the purposes of capital adequacy;

• qualifying capital instruments such as non-cumulative perpetual preference shares and hybrid capital securities

are included in other tier 1 capital; and

• tier 2 capital comprises qualifying subordinated loan capital, related non-controlling interests, allowable

collective impairment allowances and unrealised gains arising on the fair valuation of equity instruments held as

available for sale. Tier 2 capital also includes reserves arising from the revaluation of properties.

To ensure the overall quality of the capital base, the FSA’s rules set restrictions on the amount of hybrid capital

instruments that can be included in tier 1 capital relative to core tier 1 capital, and limits overall tier 2 capital to no

more than tier 1 capital.