HSBC 2012 Annual Report Download - page 16

Download and view the complete annual report

Please find page 16 of the 2012 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

|

|

HSBC HOLDINGS PLC

Report of the Directors: Overview (continued)

HSBC Values / Business and operating models

14

Ensuring our conduct matches our values

In line with our ambition to be recognised as the

world’s leading international bank, we aspire to

lead the industry in our standards of conduct. As

international markets become more interconnected

and complex and, as threats to the global financial

system grow, we are strengthening further the

policies and practices which govern how we do

business and with whom.

Like any business, we greatly value our

reputation. HSBC’s success over the years is due in

no small part to our reputation for trustworthiness

and integrity. In April 2012, as part of this effort, we

committed to adopting and enforcing the highest

compliance standards across HSBC. Doing so will

help us to achieve three key objectives:

• strengthen our capabilities to combat the

ongoing threat of financial crime;

• make consistent – and therefore simplify –

how we monitor and enforce high standards

at HSBC; and

• ensure that we consistently apply our values so as

to serve positively the customers and societies

who entrust their financial needs to HSBC.

Under the supervision of HSBC’s Global

Standards Steering Meetings of the Group

Management Board (‘GMB’), we are already

strengthening policies and processes in a number of

important areas, described on the right.

We are also reinforcing the status of compliance

and standards as an important element of how we

assess and reward senior executives, and rolling out

communication, training and assurance programmes

to ensure that our staff understand and meet their

responsibilities.

We have adopted the UK Code of Practice for

the Taxation of Banks and seeks to apply the spirit

as well as the letter of the law in all the territories in

which it operates. We deal with tax authorities in an

open and honest manner. We are strengthening our

policies and controls with the objective of ensuring

our services are not used by clients seeking to evade

their tax obligations.

A new committee of the HSBC Holdings Board,

the Financial System Vulnerabilities Committee, will

provide governance, oversight and policy guidance

over the framework of controls and procedures

designed to identify areas where HSBC may become

exposed and through that exposure, expose the

financial system more broadly to financial crime or

system abuse.

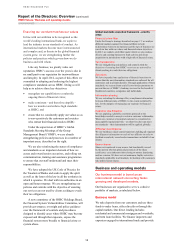

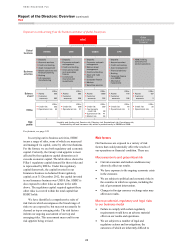

Global standards execution framework – priority

areas

Financial crime filter

Under the Group’s strategy described on page 17, we analyse

different markets against five financial filters to help

us determine where to do business and the type of business we

can do in line with our values and financial return objectives.

In 2012, we added a sixth filter under which we also analyse

all new and existing business to limit activity and client

acquisition in jurisdictions with a high risk of financial crime.

Tax transparency

We are strengthening our policies and controls with the

objective of ensuring that HSBC’s services are not used by

clients seeking to evade their tax obligations.

Sanctions

We have expanded our application of financial sanctions to

ensure that the most demanding standards are enforced for all

currencies and in all jurisdictions. Through application of these

standards, we screen clients and all cross-border payments to

prevent the use of HSBC’s banking services for the benefit of

blacklisted countries, companies and individuals.

Information sharing

We are extending the sharing of key compliance information

between different parts of HSBC, to the extent permitted by

law, for the purpose of managing our exposure to financial

crime.

Customer due diligence

We are applying a globally consistent approach to the

knowledge needed to accept or retain a customer relationship.

When any customer or potential customer is considered an

unacceptable reputational risk – or otherwise does not meet

our standards – that determination will be applied globally.

Affiliates’ due diligence

We are building a single central repository holding all required

due diligence information on each of our affiliates in order to

facilitate seamlessly cross-border transactions on behalf of our

clients.

Bearer shares

Shares not registered to any owner, but beneficially owned

by the person who has physical possession of the share

certificates, carry inherent risks relating to money laundering

and tax evasion. We have set out minimum, highly restrictive

standards, applicable in all markets, for dealing with customers

who utilise bearer shares.

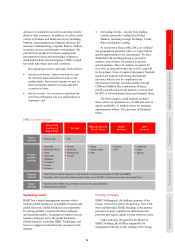

Business and operating models

Our business model is based on an

international network connecting faster-

growing and developed markets.

Our businesses are organised to serve a cohesive

portfolio of markets, as tabulated below.

Business model

We take deposits from our customers and use these

funds to make loans, either directly or through the

capital markets. Our direct lending includes

residential and commercial mortgages and overdrafts,

and term loan facilities. We finance importers and

exporters engaged in international trade and provide