HSBC 2012 Annual Report Download - page 531

Download and view the complete annual report

Please find page 531 of the 2012 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

521 -

522

522 -

523

523 -

524

524 -

525

525 -

526

526 -

527

527 -

528

528 -

529

529 -

530

530 -

531

531 -

532

532 -

533

533 -

534

534 -

535

535 -

536

536 -

537

537 -

538

538 -

539

539 -

540

540 -

541

541 -

542

-

543

-

544

-

545

-

546

|

|

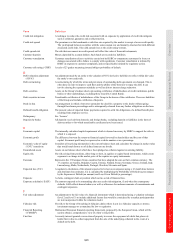

529

Overview Operating & Financial Review Corporate Governance Financial Statements Shareholder Information

Glossary

Term Definition

A

Adjustable-rate mortgages

(‘ARM’s)

Mortgage loans in the US on which the interest rate is periodically changed based on a reference price.

These are included within ‘affordability mortgages’.

Affordability mortgages Mortgage loans where the customer’s monthly payments are set out at a low initial rate, either variable or

fixed, before resetting to a higher rate once the introductory period is over.

Agency exposures Exposures to near or quasi-government agencies including public sector entities fully owned by

government carrying out non-commercial activities, provincial and local government authorities,

development banks and funds set up by government.

Alt-A A US description for loans regarded as lower risk than sub-prime, but with higher risk characteristics than

lending under normal criteria.

Arrears Customers are said to be in arrears (or in a state of delinquency) when they are behind in fulfilling their

obligations, with the result that an outstanding loan is unpaid or overdue. When a customer is in

arrears, the total outstanding loans on which payments are overdue are described as delinquent.

Asset-backed securities

(‘ABS’s)

Securities that represent an interest in an underlying pool of referenced assets. The referenced pool can

comprise any assets which attract a set of associated cash flows but are commonly pools of residential

or commercial mortgages.

B

Back-testing A statistical technique used to monitor and assess the accuracy of a model, and how that model would

have performed had it been applied in the past.

Bail-inable debt Bail-in refers to imposition of losses at the point of non viability (but before insolvency) on bank

liabilities (bail-inable debt) that are not exposed to losses while the institution remains a viable, going

concern. Whether by way of write-down or conversion into equity, this has the effect of recapitalising

the bank (although it does not provide any new funding).

Bank levy A levy that applies to UK banks, building societies and the UK operations of foreign banks from 1

January 2011. The amount payable is based on a percentage of the group’s consolidated liabilities and

equity as at 31 December 2011 after deducting certain items the most material of which are those

related to insured deposit balances, tier 1 capital, insurance liabilities, high quality liquid assets and

items subject to a legally enforceable net settlement agreement.

Basel II The capital adequacy framework issued by the Basel Committee on Banking Supervision in June 2006 in

the form of the ‘International Convergence of Capital Measurement and Capital Standards’, amended

by subsequent changes to the capital requirements for market risk and re-securitisations, commonly

known as Basel 2.5, which took effect 31 December 2011.

Basel III In December 2010, the Basel Committee issued ‘Basel III rules: A global regulatory framework for more

resilient banks and banking systems’ and ‘International framework for liquidity risk measurement,

standards and monitoring’. Together these documents present the Basel Committee’s reforms to

strengthen global capital and liquidity rules with the goal of promoting a more resilient banking sector.

In June 2011, the Basel Committee issued a revision to the former document setting out the finalised

capital treatment for counterparty credit risk in bilateral trades. The Basel III requirements will be

phased in starting on 1 January 2013 with full implementation by 1 January 2019.

Basis point (‘Bps’) One hundredth of a per cent (0.01%), so 100 basis points is 1%. Used in quoting movements in interest

rates or yields on securities.

C

Capital conservation buffer A capital buffer, prescribed by regulators under Basel III, and designed to ensure banks build up capital

buffers outside periods of stress which can be drawn down as losses are incurred. Should a bank’s

capital levels fall within the capital conservation buffer range, capital distributions will be constrained

by the regulators.

Capital planning buffer A capital buffer, prescribed by the FSA under Basel II, and designed to ensure banks build up capital

buffers outside periods of stress which can be drawn down as losses are incurred. Should a bank’s

capital levels fall within the capital planning buffer range, a period of heightened regulatory interaction

would be triggered.

Capital requirements directive

(‘CRD’)

A capital adequacy legislative package issued by the European Commission and adopted by member

states. The first CRD legislative package gave effect to the Basel II proposals in the EU and came into

force on 20 July 2006. CRD II, which came into force on 31 December 2010, subsequently updated

the requirements for capital instruments, large exposure, liquidity risk and securitisation. A further

amendment, CRD III updated market risk capital and additional securitisation requirements and came

into force on 31 December 2011.

CRD IV package comprises a recast Capital Requirements Directive and a new Capital Requirements

Regulation. The package implements the Basel III capital proposals together with transitional

arrangements for some of its requirements. CRD IV proposals are in draft and yet to have legal effect.

Central counterparty (‘CCP’) An intermediary between a buyer and a seller (generally a clearing house).

Collateralised debt obligation

(‘CDO’)

A security issued by a third-party which references ABSs and/or certain other related assets purchased by

the issuer. CDOs may feature exposure to sub-prime mortgage assets through the underlying assets.