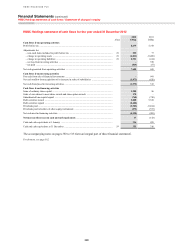

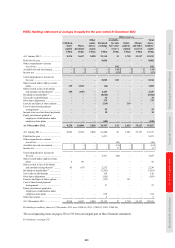

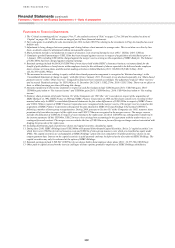

HSBC 2012 Annual Report Download - page 388

Download and view the complete annual report

Please find page 388 of the 2012 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

378 -

379

379 -

380

380 -

381

381 -

382

382 -

383

383 -

384

384 -

385

385 -

386

386 -

387

387 -

388

388 -

389

389 -

390

390 -

391

391 -

392

392 -

393

393 -

394

394 -

395

395 -

396

396 -

397

397 -

398

398 -

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

|

|

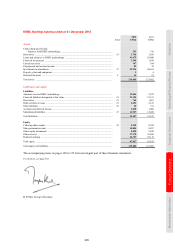

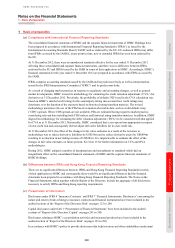

HSBC HOLDINGS PLC

Notes on the Financial Statements (continued)

1 – Basis of preparation / 2 – Summary of significant accounting policies

386

In May 2011, the IASB also issued IFRS 13 ‘Fair Value Measurement.’ This standard is effective for annual

periods beginning on or after 1 January 2013 with early adoption permitted. IFRS 13 is required to be applied

prospectively from the beginning of the first annual period in which it is applied. The disclosure requirements of

IFRS 13 do not require comparative information to be provided for periods prior to initial application.

IFRS 13 establishes a single source of guidance for all fair value measurements required or permitted by IFRSs.

The standard clarifies the definition of fair value as an exit price, which is defined as a price at which an orderly

transaction to sell the asset or to transfer the liability would take place between market participants at the

measurement date under current market conditions, and enhances disclosures about fair value measurement.

The effect of IFRS 13 is not expected to be material to HSBC.

In June 2011, the IASB issued amendments to IAS 19 ‘Employee Benefits’ (‘IAS 19 revised’). The revised

standard is effective for annual periods beginning on or after 1 January 2013 with early adoption permitted.

IAS 19 revised is required to be applied retrospectively.

The most significant amendment for HSBC is the replacement of interest cost and expected return on plan assets

by a finance cost component comprising the net interest on the net defined benefit liability or asset. This finance

cost component is determined by applying the same discount rate used to measure the defined benefit obligation

to the net defined benefit liability or asset. The difference between the actual return on plan assets and the return

included in the finance cost component in the income statement will be presented in other comprehensive

income. The effect of this change is to increase the pension expense by the difference between the current

expected return on plan assets and the return calculated by applying the relevant discount rate.

Based on our estimate of the effect of this particular amendment on the 2012 consolidated financial statements,

the change would have an immaterial effect on pre-tax profit and total operating expenses, with no effect on the

pension liability. Therefore, the effect at the date of adoption on 1 January 2013 was not material to HSBC.

In December 2011, the IASB issued amendments to IFRS 7 ‘Disclosures – Offsetting Financial Assets and

Financial Liabilities’ which requires the disclosures about the effect or potential effects of offsetting financial

assets and financial liabilities and related arrangements on an entity’s financial position. The amendments are

effective for annual periods beginning on or after 1 January 2013 and interim periods within those annual

periods. The amendments are required to be applied retrospectively.

Standards applicable in 2014

In December 2011, the IASB issued amendments to IAS 32 ‘Offsetting Financial Assets and Financial

Liabilities’ which clarify the requirements for offsetting financial instruments and address inconsistencies

in current practice when applying the offsetting criteria in IAS 32 ‘Financial Instruments: Presentation’. The

amendments are effective for annual periods beginning on or after 1 January 2014 and are required to be applied

retrospectively.

Based on our initial assessment, we do not expect the amendments to IAS 32 to have a material effect on

HSBC’s financial statements.

In October 2012, the IASB issued amendments to IFRS 10, IFRS 12 and IAS 27 ‘Investment Entities’, which

introduced an exception to the principle that all subsidiaries shall be consolidated. The amendments require a

parent that is an investment entity to measure its investments in particular subsidiaries at fair value through

profit or loss instead of consolidating all subsidiaries in its consolidated and separate financial statements. The

amendments are effective from 1 January 2014 with early adoption permitted. Based on our initial assessment,

we do not expect the amendments to have a material effect on HSBC’s consolidated financial statements.

Standards applicable in 2015

In November 2009, the IASB issued IFRS 9 ‘Financial Instruments’ which introduced new requirements for the

classification and measurement of financial assets. In October 2010, the IASB issued an amendment to IFRS 9

incorporating requirements for financial liabilities. Together, these changes represent the first phase in the

IASB’s planned replacement of IAS 39 ‘Financial Instruments: Recognition and Measurement.’

Following the IASB’s decision in December 2011 to defer the effective date, the standard is effective for annual

periods beginning on or after 1 January 2015 with early adoption permitted. IFRS 9 is required to be applied

retrospectively but prior periods need not be restated.