HSBC 2012 Annual Report Download - page 108

Download and view the complete annual report

Please find page 108 of the 2012 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

|

|

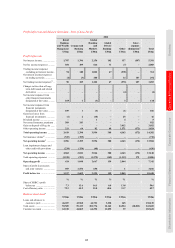

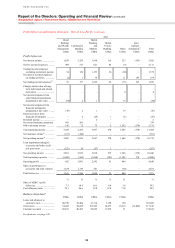

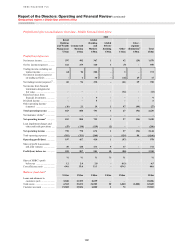

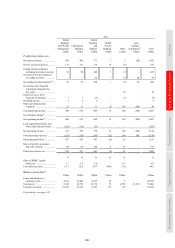

HSBC HOLDINGS PLC

Report of the Directors: Operating and Financial Review (continued)

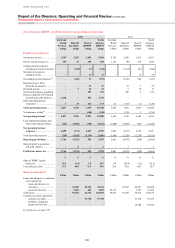

Geographical regions > North America

106

existing infrastructure. We also completed the sale of

the retail branches, principally in upstate New York,

recognising gains of US$586m in RBWM and

US$278m in CMB.

In Canada, we completed the sale of the full

service retail brokerage business. We also

announced the closure of our consumer finance

business, which had net customer loan balances

of US$1.5bn at 31 December 2012, and ceased the

origination of loans as this business did not fit with

our core strategy.

We continued to manage the run-off of lending

balances in our CML portfolio and, in the third

quarter of 2012, we reclassified non-real estate

personal loan balances of US$3.7bn, net of

impairment allowances, from our CML portfolio

to ‘Assets held for sale’ as we actively marketed the

portfolio. We also identified real estate secured loan

balances, with a carrying amount of US$3.8bn,

which, as part of our strategy, we have announced

we plan to actively market in multiple transactions

over the next two years. At 31 December 2012, the

carrying value of the non-real estate and the real

estate secured loans which we intend to sell was

approximately US$1bn greater than their estimated

fair value. We expect to recognise a loss on sale for

these loans over the next few years, the actual

amount of which will depend on market conditions

at the time of the sales. It is expected that reduction

in these loans in our CML portfolio will be capital

accretive and will reduce funding requirements,

accelerate the winding down of the portfolio and also

alleviate some of the operational burdens, given that

these loans are servicing intensive and subject to

foreclosure delays.

At 31 December 2012, lending balances

in CML, including loans held for sale, were

US$43bn, a decline of 14% from December 2011, of

which 8% was attributable to the balances written

off.

We incurred costs of US$221m in 2012 (2011:

US$235m) as a result of restructuring activities in

the region. These costs were mainly related to the

business disposals, the closure of our consumer

finance operations in Canada and the continuation of

our organisational effectiveness initiatives. We also

achieved approximately US$230m of additional

sustainable cost savings in 2012, primarily derived

from operational efficiencies.

Following the disposals noted above, we are

reshaping our US operations to focus on core

activities and are continuing to reposition our

businesses in both the US and Canada towards

international customers.

In RBWM, we continued to develop our

Wealth Management capabilities across the region,

targeting internationally connected customers in key

US and Canadian urban centres. Our relationship-

based model offers a suite of wealth services

incorporating HSBC and third-party products,

enabling our internationally-minded customers to

invest in global markets. In the US, we launched a

renminbi fixed income fund to provide investors

with the opportunity to access mainland China’s

bond market.

In CMB, we increased the number of

relationship managers and specialist sales staff in

2012 in areas with strong international connectivity,

notably the West Coast, South East and Midwest of

the US, leading to higher lending balances than in

2011. In Canada, we introduced the first renminbi

currency account. We also established dedicated

sales teams to enhance CMB’s collaboration with

GB&M. In addition, in CMB and GB&M, we

continued to target companies with international

banking requirements, leading to a rise in Global

Trade and Receivables Finance revenues in both the

US and Canada.

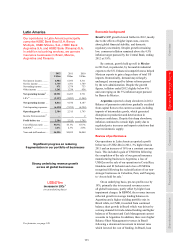

In GB&M, we continued to work on delivering

integrated solutions for our customers across the

region, increasing our lending to Latin American

corporates. In addition, we actively reduced our

legacy credit exposure in the US by exiting certain

positions. We will continue to reduce the size of this

portfolio as opportunities arise.

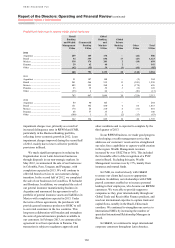

The following commentary is on a constant

currency basis.

Net interest income decreased by 29% to

US$8.1bn, due to the loss of income from the Card

and Retail Services business together with the

continued reduction of the CML portfolio in run-off.

Also contributing to the decrease was a change in

composition of our lending book towards higher

levels of lower yielding real estate loans.

Net fee income decreased by 24% to US$2.5bn,

primarily due to the sale of the Card and Retail

Services business, the retail branches and the full

service retail brokerage business in Canada. This

was partly offset by fees from the transition service

agreement with the purchaser of the Card and Retail

Services business and increased revenues from debt

capital markets origination activity due to the strong

debt issuance market.

Net trading income of US$507m was US$871m

higher than in 2011, primarily due to lower adverse

fair value movements on non-qualifying hedges in