HSBC 2012 Annual Report Download - page 164

Download and view the complete annual report

Please find page 164 of the 2012 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

|

|

HSBC HOLDINGS PLC

Report of the Directors: Operating and Financial Review (continued)

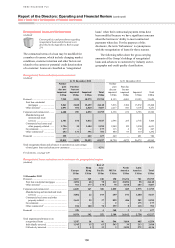

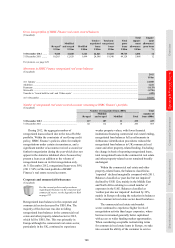

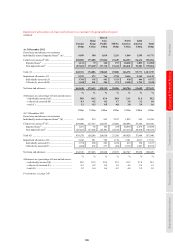

Risk > Credit risk > Credit quality of financial instruments / Collateral

162

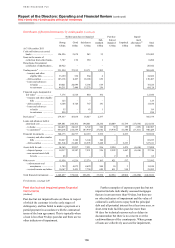

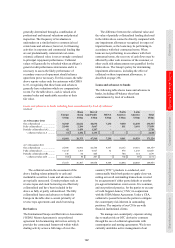

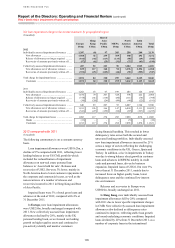

the revised interest payments as a prerequisite.

Similarly, for principal payment modifications,

we require the customer to be capable of complying

with the revised terms as a necessary pre-condition.

When principal payments are modified and

permanent forgiveness results, or when it is

otherwise considered that there is no longer a

realistic prospect of recovering outstanding

principal, the affected balances are written off.

When principal repayments are postponed, the

customer is expected to be able to pay in line with

the renegotiated terms, including meeting the

postponed principal repayment if due from

refinancing. In all cases, a loan renegotiation is

only granted when it is expected that the customer

will be able to meet the revised terms.

Renegotiated loan balances in the manufacturing

and international trade services sector increased in

2012, mainly in Latin America from the restructuring

of a small number of loans in Mexico. In the Middle

East and North Africa, renegotiated loan balances

decreased, partly due to the repayment of a significant

loan in the UAE.

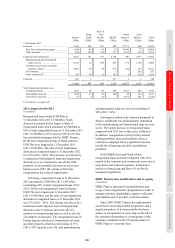

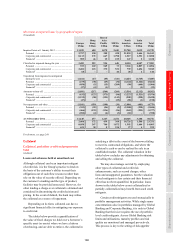

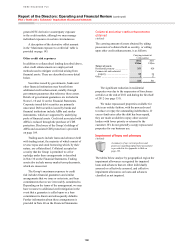

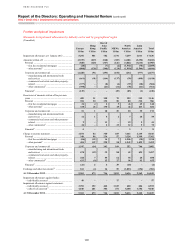

Impaired loans

(Audited)

Impaired loans and advances are those that meet

any of the following criteria:

• loans and advances classified as CRR 9,

CRR 10, EL 9 or EL 10 (a description of our

internal credit rating grades is provided on

page 253);

• retail exposures 90 days or more past due,

unless individually they have been assessed

as not impaired; or

• renegotiated loans and advances that have been

subject to a change in contractual cash flows as

a result of a concession which the lender would

not otherwise consider, and where it is probable

that without the concession the borrower would

be unable to meet its contractual payment

obligations in full, unless the concession is

insignificant and there are no other indicators

of impairment. Renegotiated loans remain

classified as impaired until there is sufficient

evidence to demonstrate a significant reduction

in the risk of non-payment of future cash flows,

and there are no other indicators of impairment.

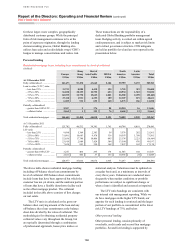

For loans that are assessed for impairment

on a collective basis, the evidence to support

reclassification as no longer impaired typically

comprises a history of payment performance against

the original or revised terms, depending on the

nature and volume of forbearance and the credit

risk characteristics surrounding the renegotiation.

For loans that are assessed for impairment on an

individual basis, all available evidence is assessed

on a case by case basis.

In HSBC Finance, where a significant majority

of HSBC’s loan forbearance activity occurs, the

history of payment performance is assessed with

reference to the original terms of the contract,

reflecting the higher credit risk characteristics of

this portfolio. The payment performance periods are

monitored to ensure they remain appropriate to the

levels of recidivism observed within the portfolio.

Further disclosure about loans subject to

forbearance is provided on page 254. Renegotiated

loans and forbearance disclosures are subject to

evolving industry practice and regulatory guidance.