HSBC 2007 Annual Report Download - page 99

Download and view the complete annual report

Please find page 99 of the 2007 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

|

|

97

staffing to support business growth initiatives. Also

contributing was US$70 million of one-off costs

arising from the indemnification agreement with

Visa ahead of the company’s planned IPO.

Marketing costs to support the growth in

Personal Financial Services lending increased in

2007, but in the second half expenditure on credit

cards, co-branded credit cards and personal non-

credit card marketing declined following the

decision to slow loan growth in these portfolios. In

HSBC Bank USA, marketing costs rose as a result of

campaigns promoting the online savings product and

investment in the HSBC brand, including the

Newark Airport branding and the HSBC Premier

relaunch. The expansion of the bank branch network

in existing and new geographical areas also

increased premises and other branch operating costs.

In Canada, operating expenses increased by

13 per cent due to the strategic growth of the branch

network, marketing to support new products, related

investment in systems, and higher transaction costs

caused by the rise in customer numbers. Staff

numbers, premises and equipment costs rose, partly

due to the opening of five new branches. Marketing

costs rose too, principally due to direct savings and

brand awareness campaigns. The Canadian

consumer finance business restructured its business

model to align with changes in the US consumer

finance operations, reducing lending through its

branch network and closing the correspondent

mortgage business. A total of 29 consumer finance

branches were closed.

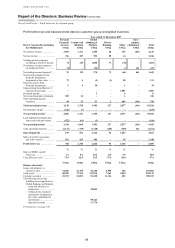

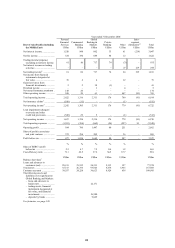

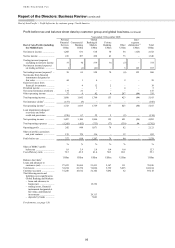

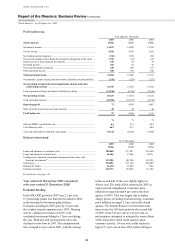

Commercial Banking’s pre-tax profits of

US$920 million declined by 6 per cent compared

with 2006. In the US, loan and deposit balances

grew with the continuing expansion of the branch

network outside its traditional base into 16 of the

top 25 business centres by the end of the year,

complemented by a restructuring of the branch sales

force. Despite this growth, overall performance

declined as business expansion costs, restructuring

costs, lower gains on asset disposals, a slowdown

in commercial and real estate activity and a

deterioration in the credit environment more

than offset the benefit of higher volumes.

In Canada, profit before tax was broadly flat at

US$466 million, driven by strong balance sheet

growth, notwithstanding the wider funding and

liquidity pressures which arose from the freezing of

the non-bank ABCP market in Canada in August.

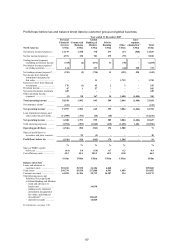

In the US, net interest income rose by 10 per

cent to US$804 million, driven by average deposit

growth of 20 per cent and loan growth of 6 per cent.

Organic expansion underpinned the increase, with

recently opened offices in Chicago, Washington DC

and the West Coast contributing to growth. Net

interest income growth slowed as a result of

declining commercial real estate activity, with higher

repayments and slower replacement business

reflecting market conditions and credit appetite.

There were also narrower spreads on deposits, as

customers migrated to higher yielding products.

Average deposit balances in the US rose by

20 per cent, led by a 21 per cent increase in volumes

from small business customers. The expansion of the

network and targeted marketing initiatives were key

factors in the rise. Spreads narrowed as the product

mix changed towards higher yielding accounts,

particularly among small business customers, partly

offsetting the gains to income from higher balances.

Average loan balances in the US were 4 per cent

higher. Loan growth was primarily due to strong

activity in middle market lending, up 20 per cent,

with growth coming equally from existing branches

and geographic expansion. Overall loan growth was,

however, much lower as a result of a slowdown in

financing commercial real estate activity, where

lending volumes fell by 6 per cent. Competitive

pressures led to narrower spreads.

In Canada, net interest income rose by 14 per

cent, driven by strong loan growth, particularly in

Western Canada. Average deposit balances rose by

10 per cent, with volumes lifted by the success of the

payments and cash management business. Spreads

rose as repricing initiatives on key products offset

the effects of competitive pressures and increased

funding costs over the last four months of 2007, due

to the disruption caused to the ABCP market by

constrained liquidity, as described above.

Average lending balances rose by 17 per cent,

buoyed by the strong economic backdrop. There was

notable expansion in Western Canada, where the

resource economy continued to underpin

performance. Spreads were tighter due to spread

compression on floating rate loans.

In Bermuda, net interest income increased by

15 per cent. Average deposit balances fell by 6 per

cent, mainly due to lower than expected growth in

volumes of fixed term deposits.

Net fee income was broadly unchanged at

US$338 million. In the US, fee income was flat

compared with 2006. The growth in deposit accounts

and a focus on business debit cards for small and

micro businesses led to a rise in deposit service

charges and card fees. This was, however, offset by

lower fees on the syndication of commercial real

estate loans as balance activity declined. In Canada,