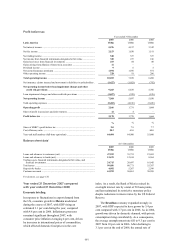

HSBC 2007 Annual Report Download - page 117

Download and view the complete annual report

Please find page 117 of the 2007 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

|

|

115

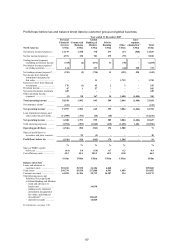

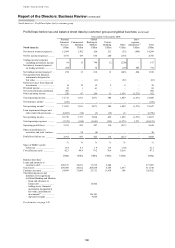

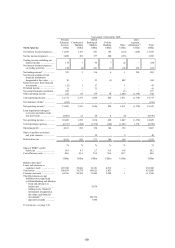

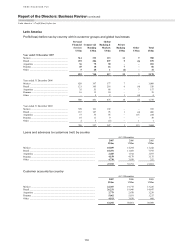

HSBC’s two-pronged objective to become the

leading international bank and the best bank for small

businesses delivered results as regional customer

numbers grew by over 14 per cent. Income from

payments and cash management rose by 8 per cent,

while the network of International Banking Centres

in Argentina, Brazil and Mexico was extended to

improve regional coverage. Other developments

included the launch of electronic account opening

facilities in Mexico and BusinessDirect in Brazil.

Operating income showed an improvement on

2006, although this was partly offset by an increase

in costs driven by expansion. As a result, the cost

efficiency ratio improved by 0.4 percentage points to

54.3 per cent.

Net interest income rose by 17 per cent, mainly

from an increase in both deposits and loans.

In Mexico, net interest income rose by 21 per

cent to US$496 million, reflecting volume growth in

deposits, commercial real estate lending, increased

support for larger local and global commercial

customers and strong volume growth in trade and

factoring. Average lending balances rose by 37 per

cent, primarily on large corporates, while spreads

widened on small business loans. Spreads on deposit

accounts narrowed. Customer relationship

management campaigns resulted in new customer

acquisition and increased cross-sales to existing

customers.

In Brazil, net interest income increased by

10 per cent, mainly due to higher income from small

and mid-market enterprises in the favourable

economic environment. Increases in volumes were

notable in the guaranteed account, giro facil, working

capital facilities and rural loans.

Net interest income increased by 86 per cent

in Argentina, due both to strong organic loan and

deposit growth, and the inclusion of four additional

months of Banca Nazionale revenues. Corporate and

mid-market business grew significantly, reflecting

the successful integration of the Banca Nazionale

network, while the targeting of small and micro

enterprises coupled with the launching of new

products also helped drive portfolio growth.

Customer loans and advances rose by 50 per cent

while customer deposits increased by 33 per cent.

Net fee income was 14 per cent higher, driven

by robust growth throughout the region.

In Mexico, fee income grew by 13 per cent

across a broad product portfolio. Following a strategy

to migrate more transactions to internet-based

services, payment and cash management transactions

increased by 11 per cent and active customers by

19 per cent, resulting in higher income generation. A

growth in the number of ATMs led to higher income

from ATM interbank charges. Increased use of credit

cards at point of sale also increased fee income. Trust

fees increased significantly, mainly due to market

share gains in the structured products market. Growth

in trade services was driven by the Group’s

geographical presence and enhanced product

capabilities, as market share and cross-selling

activities increased. International factoring was also

successfully launched during 2007.

In Brazil, fee income rose by 11 per cent, mainly

on small and micro enterprises. Payments and cash

management income increased, mainly on higher

volumes. Current account income increased as a

result of a re-pricing exercise and a rise in volumes.

Fees from loans and funds under management also

grew on higher volumes. More than 110,000 products

were sold over e-channels, a significant increase on

the previous year.

In Argentina, HSBC increased fee income by

48 per cent, primarily due to an additional four

months of Banca Nazionale revenues combined with

higher transaction volumes. The main product drivers

behind the increase were current accounts, which rose

by 38 per cent, and trade services, which grew by

39 per cent on higher volumes, placing HSBC among

the top three banks in imports and exports

in Argentina.

Trading income rose on the back of higher

volumes of foreign exchange transactions and sales

of treasury products in Brazil, which reflected higher

market share and favourable market conditions.

Foreign exchange trading income also increased in

Argentina.

Net gains from financial investments rose by

US$47 million, driven by a gain of US$45 million

following a sale of shares held in a credit bureau, a

stock exchange and a derivatives exchange in Brazil.

Loan impairment charges were 28 per cent lower

at US$212 million.

In Mexico, HSBC recorded a net decrease in

loan impairment charges as increased delinquency

rates in the small and medium-sized business

portfolios were offset by impairment allowance

releases. Regular reviews aimed at strengthening

consumer credit management and collections were

put in place to better manage delinquency rates as the

portfolio matures. Credit models were updated during

2007 to adjust to credit behaviour in underlying

portfolios. Products with high credit losses were

discontinued or restructured.