Frontier Communications 2008 Annual Report Download - page 75

Download and view the complete annual report

Please find page 75 of the 2008 Frontier Communications annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

|

|

For the year ended December 31, 2006, we retired an aggregate principal amount of $251.0 million of

debt, including $15.9 million of EPPICS that were converted into our common stock.

During the first quarter of 2006, we entered into two debt-for-debt exchanges of our debt securities. As a

result, $47.5 million of our 7.625% notes due 2008 were exchanged for approximately $47.4 million of our

9.00% notes due 2031. During the fourth quarter of 2006, we entered into four debt-for-debt exchanges and

exchanged $157.3 million of our 7.625% notes due 2008 for $149.9 million of our 9.00% notes due 2031. The

9.00% notes are callable on the same general terms and conditions as the 7.625% notes exchanged. No cash

was exchanged in these transactions. However, with respect to the first quarter debt exchanges, a non-cash pre-

tax loss of approximately $2.4 million was recognized in accordance with EITF No. 96-19, “Debtor’s

Accounting for a Modification or Exchange of Debt Instruments,” which is included in other income (loss), net,

for the year ended December 31, 2006.

On June 1, 2006, we retired at par our entire $175.0 million principal amount of 7.60% Debentures due

June 1, 2006.

On June 14, 2006, we repurchased $22.7 million of our 6.75% Senior Notes due August 17, 2006 at a

price of 100.181% of par.

On August 17, 2006, we retired at par the $29.1 million remaining balance of the 6.75% Senior Notes.

On December 22, 2006, we issued in a private placement, an aggregate $400.0 million principal amount of

7.875% Senior Notes due January 15, 2027. Proceeds from the sale were used to partially finance the

Commonwealth acquisition.

In December 2006, we borrowed $150.0 million under a senior unsecured term loan agreement. The loan

matures in 2012 and bears interest based on an average prime rate or London Interbank Offered Rate or LIBOR

plus 1

3

⁄

8

%, at our election. Proceeds were used to partially finance the Commonwealth acquisition.

As of December 31, 2008 we were in compliance with all of our debt and credit facility covenants.

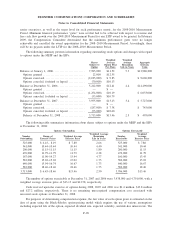

Our principal payments for the next five years are as follows:

($ in thousands)

Principal

Payments

2009 ........................................................................... $ 3,857

2010 ........................................................................... $ 7,236

2011 ........................................................................... $1,125,143

2012 ........................................................................... $ 180,366

2013 ........................................................................... $ 829,131

(12) Derivative Instruments and Hedging Activities:

Interest rate swap agreements were used to hedge a portion of our debt that is subject to fixed interest

rates. Under our interest rate swap agreements, we agreed to pay an amount equal to a specified variable rate of

interest times a notional principal amount, and to receive in return an amount equal to a specified fixed rate of

interest times the same notional principal amount. The notional amounts of the contracts were not exchanged.

No other cash payments are made unless the agreement is terminated prior to maturity, in which case the

amount paid or received in settlement is established by agreement at the time of termination and represents the

market value, at the then current rate of interest, of the remaining obligations to exchange payments under the

terms of the contracts.

On January 15, 2008, we terminated all of our interest rate swap agreements representing $400.0 million

notional amount of indebtedness associated with our Senior Notes due in 2011 and 2013. Cash proceeds on the

swap terminations of approximately $15.5 million were received in January 2008. The related gain has been

deferred on the consolidated balance sheet, and is being amortized into interest expense over the term of the

associated debt. For the year ended December 31, 2008, we recognized $5.0 million of deferred gain and

anticipate recognizing $3.4 million during 2009.

F-24

FRONTIER COMMUNICATIONS CORPORATION AND SUBSIDIARIES

Notes to Consolidated Financial Statements