Frontier Communications 2008 Annual Report Download - page 69

Download and view the complete annual report

Please find page 69 of the 2008 Frontier Communications annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

|

|

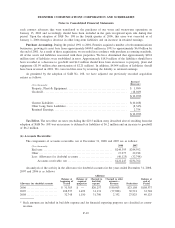

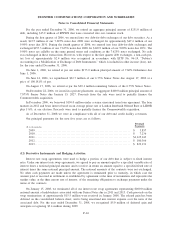

Summary of SAB No. 108 entry recorded January 1, 2006:

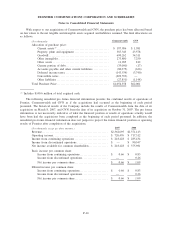

($ in thousands)

Increase/

(Decrease)

Property, Plant & Equipment ............................................... $ 1,990

Goodwill .................................................................. (3,716)

Other Assets............................................................... (20,081)

$(21,807)

Current Liabilities ......................................................... $ (2,922)

Deferred Taxes . ........................................................... (17,339)

Other Long-Term Liabilities ................................................ (13,037)

Long-Term Debt ........................................................... (24,901)

Retained Earnings. ......................................................... 36,392

$(21,807)

Deferred Tax Accounting. As a result of adopting SAB No. 108 in the fourth quarter of 2006 we

recorded a decrease in deferred income tax liabilities in the amount of approximately $23.5 million and an

increase in retained earnings of approximately $23.5 million as of January 1, 2006. The change in deferred tax

and retained earnings is a result of excess deferred tax liabilities that built up in periods prior to 2004

(approximately $4 million in 2003, $5.4 million in 2002 and $14.1 million in 2001 and prior), resulting

primarily from differences between actual state income tax rates and the effective composite state rate utilized

for estimating the Company’s book state tax provisions.

Goodwill. During 2002, we estimated and booked impairment charges (pre-tax) of $1.07 billion. We

subsequently discovered that the impairment charge recorded was overstated as it exceeded the underlying book

value by approximately $8.1 million. The result was an understatement of goodwill. We corrected this error by

reversing the negative goodwill balance of $8.1 million with an offset to increase retained earnings.

Unrecorded Liabilities. The Company changed its accounting policies associated with the accrual of

utilities and vacation expense. Historically, the Company’s practice was to expense utility and vacation costs in

the period these items were paid, which generally resulted in a full year of utilities and vacation expense in the

consolidated statements of operations. The utility costs are now accrued in the period used and vacation costs

are accrued in the period earned. The cumulative amount of these changes as of the beginning of fiscal 2006

was approximately $3.0 million and, as provided in SAB No. 108, the impact was recorded as a reduction of

retained earnings as of the beginning of fiscal 2006.

We established an accrual of $4.5 million for advance billings associated with certain revenue at two

telephone properties that the Company operated since the 1930’s. For these two properties, the Company’s

records have not reflected the liability. This had no impact on the revenue reported for any of the five years

reported in this Form 10-K.

We recorded a long-term liability of $2.5 million to recognize a postretirement annuity payment obligation

for two former executives of the Company. The liability should have been established in 1999 at the time the

two employees elected to exchange their death benefit rights for an annuity payout in accordance with the

terms of their respective split-dollar life insurance agreements. We established the liability effective January 1,

2006 in accordance with SAB No. 108 by reducing retained earnings by a like amount.

Long-Term Debt. We recorded a reclassification of $20.1 million from other assets to long-term debt.

The amount represents debt discounts which the Company historically accounted for as a deferred asset. For

certain debt issuances the Company amortized the debt discount using the straight line method instead of the

effective interest method. We corrected this error by increasing the debt discount by $4.8 million and increasing

retained earnings by a like amount.

Customer Advances for Construction. Amounts associated with “construction advances” remaining on

the Company’s balance sheet ($92.4 million at December 31, 2005) included approximately $7.3 million of

F-18

FRONTIER COMMUNICATIONS CORPORATION AND SUBSIDIARIES

Notes to Consolidated Financial Statements