Costco 2012 Annual Report Download - page 52

Download and view the complete annual report

Please find page 52 of the 2012 Costco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

|

|

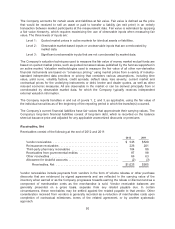

The Company accounts for certain asets and liabilities at fair value. Fair value is defined as the price

that would be received to sell an asset or paid to transfer a liability (an exit price) in an orderly

transaction between market participants at the measurement date. Fair value is estimated by applying

a fair value hierarchy, which requires maximizing the use of observable inputs when measuring fair

value. The three levels of inputs are:

Level 1: Quoted market prices in active markets for identical assets or liabilities.

Level 2: Observable market-based inputs or unobservable inputs that are corroborated by

market data.

Level 3: Significant unobservable inputs that are not corroborated by market data.

The Company’s valuation techniques used to measure the fair value of money market mutual funds are

based on quoted market prices, such as quoted net asset values published by the fund as supported in

an active market. Valuation methodologies used to measure the fair value of all other non-derivative

financial instruments are based on “consensus pricing,” using market prices from a variety of industry-

standard independent data providers or pricing that considers various assumptions, including time

value, yield curve, volatility factors, credit spreads, default rates, loss severity, current market and

contractual prices for the underlying instruments or debt, broker and dealer quotes, as well as other

relevant economic measures. All are observable in the market or can be derived principally from or

corroborated by observable market data, for which the Company typically receives independent

external valuation information.

The Company reports transfers in and out of Levels 1, 2, and 3, as applicable, using the fair value of

the individual securities as of the beginning of the reporting period in which the transfer(s) occurred.

The Company’s current financial liabilities have fair values that approximate their carrying values. The

Company’s long-term financial liabilities consist of long-term debt, which is recorded on the balance

sheet at issuance price and adjusted for any applicable unamortized discounts or premiums.

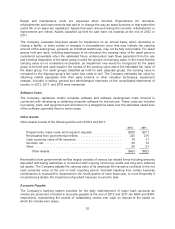

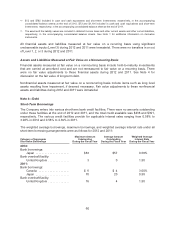

Receivables, Net

Receivables consist of the following at the end of 2012 and 2011:

2012 2011

Vendor receivables .......................................... $ 545 $520

Reinsurance receivables ...................................... 226 201

Third-party pharmacy receivables .............................. 104 86

Receivables from governmental entities ......................... 87 98

Other receivables ............................................ 66 63

Allowance for doubtful accounts ................................ (2) (3)

Receivables, Net ........................................ $1,026 $965

Vendor receivables include payments from vendors in the form of volume rebates or other purchase

discounts that are evidenced by signed agreements and are reflected in the carrying value of the

inventory when earned or as the Company progresses towards earning the rebate or discount and as a

component of merchandise costs as the merchandise is sold. Vendor receivable balances are

generally presented on a gross basis, separate from any related payable due. In certain

circumstances, these receivables may be settled against the related payable to that vendor. Other

consideration received from vendors is generally recorded as a reduction of merchandise costs upon

completion of contractual milestones, terms of the related agreement, or by another systematic

approach.

50