Cigna 2012 Annual Report Download - page 97

Download and view the complete annual report

Please find page 97 of the 2012 Cigna annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

|

|

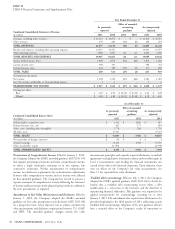

PART II

ITEM 8 Financial Statements and Supplementary Data

In addition, for the more recent months, the Company also relies on postemployment benefits (see Note 10), the loss position of certain

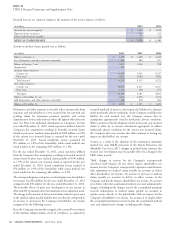

medical cost trend analysis, which reflects expected claim payment derivatives, primarily for GMIB contracts (see Note 13), self-insured

patterns and other relevant operational considerations. Medical cost exposures, management compensation and various insurance-related

trend is primarily impacted by medical service utilization and unit items, including experience rated refunds, the minimum medical loss

costs, which are affected by changes in the level and mix of medical ratio rebate accrual under Health Care Reform, amounts related to

benefits offered, including inpatient, outpatient and pharmacy, the reinsurance contracts and insurance-related assessments that

impact of copays and deductibles, changes in provider practices and management can reasonably estimate. Accounts payable, accrued

changes in consumer demographics and consumption behavior. expenses and other liabilities also include certain overdraft positions.

Legal costs to defend the Company’s litigation and arbitration matters

Despite reflecting both historical and emerging trends in setting are expensed when incurred in cases that the Company cannot

reserves, it is possible that the actual medical trend for the current reasonably estimate the ultimate cost to defend. In cases that the

period will develop differently from expectations, which could have a Company can reasonably estimate the cost to defend, these costs are

material impact on the Company’s medical claims payable and recognized when the claim is reported.

shareholders’ net income.

For each reporting period, the Company evaluates key assumptions by

R. Translation of Foreign Currencies

comparing the assumptions used in establishing the medical claims

payable to actual experience. When actual experience differs from the The Company generally conducts its international business through

assumptions used in establishing the liability, medical claims payable foreign operating entities that maintain assets and liabilities in local

are increased or decreased through current period shareholders’ net currencies, which are generally their functional currencies. The

income. Additionally, the Company evaluates expected future Company uses exchange rates as of the balance sheet date to translate

developments and emerging trends which may impact key assets and liabilities into U.S. dollars. Translation gains or losses on

assumptions. The estimation process involves considerable judgment, functional currencies, net of applicable taxes, are recorded in

reflecting the variability inherent in forecasting future claim accumulated other comprehensive income (loss). The Company uses

payments. These estimates are highly sensitive to changes in the average monthly exchange rates during the year to translate revenues

Company’s key assumptions, specifically completion factors, and and expenses into U.S. dollars.

medical cost trends.

S. Premiums and Fees, Revenues and

O. Unearned Premiums and Fees Related Expenses

Premiums for life, accident and health insurance are recognized as Premiums for group life, accident and health insurance and managed

revenue on a pro rata basis over the contract period. Fees for mortality care coverages are recognized as revenue on a pro rata basis over the

and contract administration of universal life products are recognized contract period. Benefits and expenses are recognized when incurred.

ratably over the coverage period. The unrecognized portion of these Premiums and fees include revenue from experience-rated contracts

amounts received is recorded as unearned premiums and fees. that is based on the estimated ultimate claim, and in some cases,

administrative cost experience of the contract. For these contracts,

premium revenue includes an adjustment for experience-rated refunds

P. Redeemable Noncontrolling Interest

which is calculated according to contract terms and using the

The redeemable noncontrolling interest comprises the preferred and customer’s experience (including estimates of incurred but not

common stock interests not purchased by the Company in its reported claims). Beginning in 2011, premium revenue also includes

acquisition of Finans Emeklilik in 2012 (see Note 3A for further an adjustment to reflect the estimated effect of rebates due to

information.) This redeemable noncontrolling interest relates to the customers under the minimum medical loss ratio provisions of Health

right of the holder to require the Company to purchase the holder’s Care Reform.

49% interest at a redemption value equal to its net assets in Finans

Premiums for individual life, accident and supplemental health

Emklilik and the value of its inforce business in 15 years. Cigna also

insurance and annuity products, excluding universal life and

has the right to require the holder to sell its 49% interest to Cigna for

investment-related products, are recognized as revenue when due.

the same value in 15 years. The redeemable noncontrolling interest

Benefits and expenses are matched with premiums.

was recorded at fair value on the date of purchase. Subsequently, if the

estimated redemption value exceeds the recorded value for the Premiums and fees received for the Company’s Medicare Advantage

redeemable noncontrolling interest, an adjustment to increase the Plans and Medicare Part D products from customers and the Centers

redeemable noncontrolling interest will be recorded and impact for Medicare and Medicaid Services (CMS) are recognized as revenue

income available to common shareholders. ratably over the contract period. CMS provides risk adjusted premium

payments for the Medicare Advantage Plans and Medicare Part D

products, based on the demographics and health severity of enrollees.

Q. Accounts Payable, Accrued Expenses

The Company recognizes periodic changes to risk adjusted premiums

and Other Liabilities

as revenue when the amounts are determinable and collection is

Accounts payable, accrued expenses and other liabilities consist reasonably assured. Additionally, Medicare Part D includes payments

principally of liabilities for pension, other postretirement and from CMS for risk sharing adjustments. The risk sharing adjustments,

CIGNA CORPORATION - 2012 Form 10-K 75