Cigna 2012 Annual Report Download - page 80

Download and view the complete annual report

Please find page 80 of the 2012 Cigna annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

|

|

PART II

ITEM 7 Management’s Discussion and Analysis of Financial Condition and Results of Operations

Commercial real estate capital markets remain most active for well leased, quality commercial real estate located in strong institutional investment

markets. The vast majority of properties securing the mortgages in the Company’s mortgage portfolio possess these characteristics. While

commercial real estate fundamentals continued to improve, the improvement has varied across geographies and property types. A broad recovery

is dependent on continued improvement in the national economy.

The following table reflects the commercial mortgage loan portfolio as of December 31, 2012, summarized by loan-to-value ratio based on the

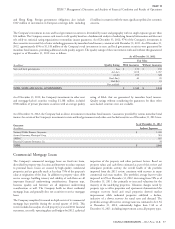

annual loan review completed during the second quarter of 2012.

LOAN-TO-VALUE DISTRIBUTION

Amortized Cost

Loan-to-Value Ratios Senior Subordinated Total % of Mortgage Loans

Below 50% $ 293 $ 62 $ 355 12%

50% to 59% 795 - 795 28%

60% to 69% 679 24 703 25%

70% to 79% 475 14 489 17%

80% to 89% 267 27 294 10%

90% to 99% 102 - 102 4%

100% or above 113 - 113 4%

TOTALS $ 2,724 $ 127 $ 2,851 100%

As summarized above, $127 million or 4% of the commercial the capital structure of these underlying entities, the Company

mortgage loan portfolio is comprised of subordinated notes that were assumes a higher level of risk for higher expected returns. To mitigate

fully underwritten and originated by the Company using its standard risk, investments are diversified across approximately 80 separate

underwriting procedures and are secured by first mortgage loans. partnerships, and approximately 50 general partners who manage one

Senior interests in these first mortgage loans were then sold to other or more of these partnerships. Also, the funds’ underlying investments

institutional investors. This strategy allowed the Company to are diversified by industry sector or property type, and geographic

effectively utilize its origination capabilities to underwrite high quality region. No single partnership investment exceeds 7% of the

loans, limit individual loan exposures, and achieve attractive risk Company’s securities and real estate partnership portfolio.

adjusted yields. In the event of a default, the Company would pursue Although the total fair values of investments exceeded their carrying

remedies up to and including foreclosure jointly with the holders of values as of December 31, 2012, the fair value of the Company’s

the senior interest, but would receive repayment only after satisfaction ownership interest in certain funds that are carried at cost was less

of the senior interest. than carrying value by $39 million. Fund investment values continued

In the table above, there are two loans in the ‘‘100% or above’’ to improve, but remained at depressed levels reflecting the impact of

category with an aggregate carrying value of $47 million that exceed declines in value experienced predominantly during 2008 and 2009

the value of their underlying properties by $5 million. Both of these due to economic weakness and disruption in the capital markets,

loans have current debt service coverage of 1.0 or greater, along with particularly in the commercial real estate market. The Company

significant borrower commitment. expects to recover its carrying value over the average remaining life of

these investments of approximately 5 years. Given the current

The commercial mortgage portfolio contains approximately 140 economic environment, future impairments are possible; however,

loans. Four impaired loans with a carrying value of $125 million are management does not expect those losses to have a material effect on

classified as problem or potential problem loans, including two loans the Company’s results of operations, financial condition or liquidity.

totaling $60 million that are current based on restructured terms and

two loans totaling $65 million, net of reserves, that are current but full

collection of principal is not expected. All of the remaining loans

Problem and Potential Problem Investments

continue to perform under their contractual terms. The Company has ‘‘Problem’’ bonds and commercial mortgage loans are either

$419 million of loans maturing in the next twelve months. Given the delinquent by 60 days or more or have been restructured as to terms,

quality and diversity of the underlying real estate, positive debt service which could include concessions by the Company for modification of

coverage and significant borrower cash investment averaging nearly interest rate, principal payment or maturity date. ‘‘Potential problem’’

30%, the Company remains confident that the vast majority of bonds and commercial mortgage loans are considered current (no

borrowers will continue to perform as expected under the contract payment more than 59 days past due), but management believes they

terms. have certain characteristics that increase the likelihood that they may

become problems. The characteristics management considers include,

Other Long-term Investments

but are not limited to, the following:

The Company’s other long-term investments include $1,166 million request from the borrower for restructuring;

in security partnership and real estate funds as well as direct principal or interest payments past due by more than 30 but fewer

investments in real estate joint ventures. The funds typically invest in than 60 days;

mezzanine debt or equity of privately held companies (securities

partnerships) and equity real estate. Given its subordinate position in downgrade in credit rating;

58 CIGNA CORPORATION - 2012 Form 10-K

•

•

•