Cigna 2012 Annual Report Download - page 126

Download and view the complete annual report

Please find page 126 of the 2012 Cigna annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

|

|

PART II

ITEM 8 Financial Statements and Supplementary Data

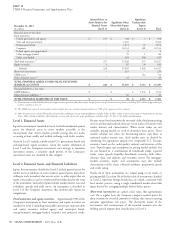

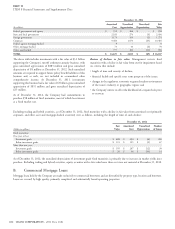

December 31, 2011

Debt Service Coverage Ratio

Loan-to-Value Ratios

(In millions)

1.30x or Greater 1.20x to 1.29x 1.10x to 1.19x 1.00x to 1.09x Less than 1.00x Total

Below 50% $ 225 $ 55 $ 3 $ 50 $ 9 $ 342

50% to 59% 444 47 26 - 53 570

60% to 69% 646 140 42 - 77 905

70% to 79% 117 132 120 159 33 561

80% to 89% 99 81 79 72 71 402

90% to 99% 36 35 30 58 116 275

100% or above - 10 50 51 135 246

TOTAL $ 1,567 $ 500 $ 350 $ 390 $ 494 $ 3,301

The Company’s annual in-depth review of its commercial mortgage During 2011, the Company restructured a $65 million potential

loan investments is the primary mechanism for identifying emerging problem loan into two notes carried at $55 million and $10 million.

risks in the portfolio. The most recent review was completed by the This modification was considered a troubled debt restructuring

Company’s investment professionals in the second quarter of 2012 because the borrower was experiencing financial difficulties and an

and included an analysis of each underlying property’s most recent interest rate concession was granted. No valuation reserve was

annual financial statements, rent rolls, operating plans, budgets, a required because the fair value of the underlying property exceeded

physical inspection of the property and other pertinent factors. Based the carrying value of the outstanding loan. As a part of this

on historical results, current leases, lease expirations and rental restructuring, the borrowers and the Company have committed to

conditions in each market, the Company estimates the current year fund additional capital for leasing and capital requirements.

and future stabilized property income and fair value, and categorizes Other loans were modified during 2012 and 2011, but were not

the investments as loans in good standing, potential problem loans or considered troubled debt restructures. The impact of modifications to

problem loans. Based on property valuations and cash flows estimated these loans was not material to the Company’s results of operations,

as part of this review, and considering updates for loans where material financial condition or liquidity.

changes were subsequently identified, the portfolio’s average

loan-to-value ratio improved to 65% at December 31, 2012, Potential problem mortgage loans are considered current (no payment

decreasing from 70% as of December 31, 2011. The portfolio’s more than 59 days past due), but exhibit certain characteristics that

average debt service coverage ratio was estimated to be 1.56 at increase the likelihood of future default. The characteristics

December 31, 2012, a significant improvement from 1.40 at management considers include, but are not limited to, the

December 31, 2011. deterioration of debt service coverage below 1.0, estimated

loan-to-value ratios increasing to 100% or more, downgrade in

Quality ratings are adjusted between annual reviews if new property quality rating and request from the borrower for restructuring. In

information is received or events such as delinquency or a borrower’s addition, loans are considered potential problems if principal or

request for restructure cause management to believe that the interest payments are past due by more than 30 but less than 60 days.

Company’s estimate of financial performance, fair value or the risk Problem mortgage loans are either in default by 60 days or more or

profile of the underlying property has been impacted. have been restructured as to terms, which could include concessions

During 2012, the Company restructured a $119 million problem on interest rate, principal payment or maturity date. The Company

mortgage loan, net of a valuation reserve, into two notes carried at monitors each problem and potential problem mortgage loan on an

$100 million and $19 million. The $100 million note was reclassified ongoing basis, and updates the loan categorization and quality rating

to impaired commercial mortgage loans with no valuation reserves when warranted.

and the $19 million note was classified as another long-term Problem and potential problem mortgage loans, net of valuation

investment. This modification was considered a troubled debt reserves, totaled $215 million at December 31, 2012 and

restructuring because the borrower was experiencing financial $336 million at December 31, 2011. At December 31, 2012,

difficulties and an interest rate concession was granted. No valuation mortgage loans located in the South Atlantic region represented the

reserve was required because the fair value of the underlying property most significant component of problem and potential problem

equaled the carrying value of the outstanding loan. Following the mortgage loans, with no significant concentration by property type.

restructuring, the $100 million note was paid down by $46 million At December 31, 2011, mortgage loans collateralized by industrial

with the remaining $54 million note reclassified to good standing due properties represent the most significant component of problem and

to an improved quality rating based on significant improvements in its potential problem mortgage loans, with no significant concentration

loan-to-value and debt service coverage ratios resulting from the by geographic region.

annual loan review.

104 CIGNA CORPORATION - 2012 Form 10-K