CarMax 2003 Annual Report Download - page 35

Download and view the complete annual report

Please find page 35 of the 2003 CarMax annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

-

47

-

48

-

49

-

50

-

51

-

52

|

|

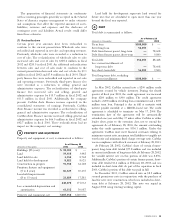

CARMAX 2003 33

undivided ownership interest in the receivables securitized

through the warehouse facility. Retained interests are

carried at fair value and changes in fair value are included

in earnings. See Notes 11 and 12 for additional discussion

on securitizations.

(D) Fair Value of Financial Instruments

The carrying value of the company’s cash and cash

equivalents, receivables including automobile loan

receivables, accounts payable, short-term borrowings and

long-term debt approximates fair value. The company’s

retained interests in securitized receivables and derivative

financial instruments are recorded on the consolidated

balance sheets at fair value.

(E) Trade Accounts Receivable

Trade accounts receivable, net of allowance for doubtful

accounts, include certain amounts due from finance

companies and customers, as well as from manufacturers for

incentives and warranty reimbursements, and for other

miscellaneous receivables. The estimate for doubtful

accounts is based on historical experience and trends.

(F) Inventory

Inventory is comprised primarily of vehicles held for sale

or for reconditioning and is stated at the lower of cost or

market. Vehicle inventory cost is determined by specific

identification. Parts and labor used to recondition vehicles,

as well as transportation and other incremental expenses

associated with acquiring and reconditioning vehicles, are

included in inventory. Certain manufacturer incentives and

rebates for new car inventory, including holdbacks, are

recognized as a reduction to new car inventory when

CarMax purchases the vehicles. Volume-based incentives

are recognized as a reduction to new car inventory cost

when achievement of volume thresholds are determined

to be probable.

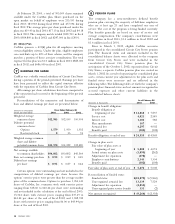

(G) Property and Equipment

Property and equipment is stated at cost less accumulated

depreciation and amortization. Depreciation and

amortization are calculated using the straight-line method

over the assets’ estimated useful lives.

(H) Computer Software Costs

External direct costs of materials and services used in the

development of internal-use software and payroll and payroll-

related costs for employees directly involved in the

development of internal-use software are capitalized.

Amounts capitalized are amortized on a straight-line basis

over a period of five years.

(I) Goodwill and Intangible Assets

Effective March 1, 2002, the company adopted SFAS No.

142, “Goodwill and Other Intangible Assets,” which

establishes accounting and reporting standards for

intangible assets and goodwill. SFAS No. 142 requires that

goodwill and intangible assets with indefinite useful lives

no longer be amortized, but rather tested for impairment at

least annually. The company performed the required

transition impairment tests of goodwill and other

intangible assets as of March 1, 2002, and determined that

no impairment existed. Additionally, as of February 28,

2003, no impairment of goodwill or intangible assets

resulted from the annual impairment test. Prior to March 1,

2002, goodwill was amortized on a straight-line basis over

15 years. The carrying amount of goodwill was $19.7

million as of February 28, 2003, and $20.1 million as of

February 28, 2002.

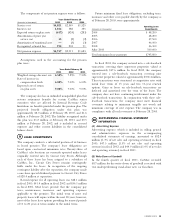

(J) Defined Benefit Plan and Insurance Liabilities

Defined benefit retirement plan obligations and insurance

liabilities are included in accrued expenses and other

current liabilities on the company's consolidated balance

sheets. The defined benefit retirement plan obligations are

determined by independent actuaries using a number of

assumptions provided by the company. Key assumptions in

measuring the plan obligations include the discount rate,

the rate of salary increases and the estimated future return

on plan assets. Insurance liability estimates for workers'

compensation, general liability and employee-related

health care benefits are determined by considering

historical claims experience, demographic factors and other

actuarial assumptions.

(K) Impairment or Disposal of Long-Lived Assets

The company reviews long-lived assets for impairment when

circumstances indicate the carrying amount of an asset may

not be recoverable. Impairment is recognized when the sum

of undiscounted estimated future cash flows expected to

result from the use of the asset is less than the carrying value.

(L) Store Opening Expenses

Costs relating to store openings, including preopening costs,

are expensed as incurred.

(M) Income Taxes

Deferred income taxes reflect the impact of temporary

differences between the amounts of assets and liabilities

recognized for financial reporting purposes and the amounts

recognized for income tax purposes, measured by applying

currently enacted tax laws. A deferred tax asset is recognized

if it is more likely than not that a benefit will be realized.