CVS 2008 Annual Report Download - page 54

Download and view the complete annual report

Please find page 54 of the 2008 CVS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

|

|

50 CVS CAREMARK

Notes to Consolidated Financial Statements

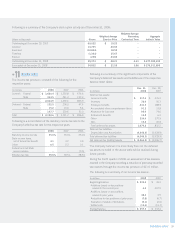

As of December 31, 2008, the Company had $202.3 million

of unrecognized tax benefi ts (after considering the federal benefi t

of state taxes) related to business combinations that would have

been treated as an adjustment to the purchase price allocation if

they had been recognized under SFAS 141. It is possible that a

signifi cant portion of these benefi ts will be recognized within the

next twelve months. To the extent these benefi ts are recognized

after the adoption of SFAS 141R, their recognition would affect

the Company’s effective income tax rate rather than being treated

as an adjustment to the purchase price allocation of the acquiree.

In February 2008, the FASB issued FASB Staff Position (“FSP”)

No. SFAS 157-2, “Effective Date of FASB Statement No. 157,”

which defers the effective date of SFAS 157 for nonfi nancial

assets and nonfi nancial liabilities, except those that are recog-

nized or disclosed at fair value in the fi nancial statements on

a recurring basis (at least annually), to fi scal years and interim

periods within those fi scal years, beginning after November 15,

2008. The Company does not believe the adoption of this

statement will have a material effect on its consolidated results

of operations, fi nancial position and cash fl ows.

In April 2008, the FASB issued FSP No. FAS 142-3, “Determining

the Useful Life of Intangible Assets,” which amends the factors

an entity should consider in developing renewal or extension

assumptions used in determining the useful lives of recognized

intangible assets. This statement is effective for fi scal years

beginning after December 15, 2008. The Company does not

believe the adoption of this statement will have a material effect

on its consolidated results of operations, fi nancial position and

cash fl ows.

In June 2008, the FASB reached consensus on EITF Issue

No. 08-3, “Accounting by Lessees for Nonrefundable

Maintenance Deposits” (“EITF 08-3”). Under EITF 08-3,

lessees should account for nonrefundable maintenance deposits

as deposit assets if it is probable that maintenance activities will

occur and the deposit is therefore realizable. Amounts on deposit

that are not probable of being used to fund future maintenance

activities should be expensed. EITF 08-3 is effective for fi scal

years beginning after December 15, 2008. Early application is

not permitted. The Company does not believe the adoption of

this statement will have a material effect on its consolidated

results of operations, fi nancial position and cash fl ows.

In December 2008, the FASB issued FSP No. FAS 132(R)-1,

“Employers’ Disclosures about Postretirement Benefi t Plan

Assets,” which enhances the required disclosures about plan

assets in an employer’s defi ned benefi t pension or other postre-

tirement plan, including investment allocations decisions, inputs

New accounting pronouncements. In the fi rst quarter of 2008,

the Company adopted EITF Issue No. 06-4, “Accounting for

Deferred Compensation and Postretirement Benefi t Aspects of

Endorsement Split-Dollar Life Insurance Arrangements” (“EITF

06-4”). EITF 06-4 requires the application of the provisions

of SFAS No. 106, “Employers’ Accounting for Postretirement

Benefi ts Other Than Pensions” (“SFAS 106”) (if, in substance,

a postretirement benefi t plan exists), or Accounting Principles

Board Opinion No. 12 (if the arrangement is, in substance, an

individual deferred compensation contract) to endorsement

split-dollar life insurance arrangements. SFAS 106 requires the

recognition of a liability for the discounted value of the future

premium benefi ts that will be incurred through the death of

the underlying insureds. The adoption of this statement did not

have a material effect on the Company’s consolidated results

of operations, fi nancial position and cash fl ows.

In the fi rst quarter of 2008, the Company adopted EITF

No. 06-10 “Accounting for Collateral Assignment Split-Dollar

Life Insurance Agreements” (“EITF 06-10”) effective fi scal

2008. EITF 06-10 provides guidance for determining a liability

for the postretirement benefi t obligation as well as recognition and

measurement of the associated asset on the basis of the terms of

the collateral assignment agreement. The adoption of this state-

ment did not have a material effect on the Company’s consolidated

results of operations, fi nancial position and cash fl ows.

In the fi rst quarter of 2008, the Company adopted Financial

Accounting Standards Board (“FASB”) Staff Position No. FAS

157-3, “Determining the Fair Value of a Financial Asset When

the Market for That Asset Is Not Active,” which clarifi es the

application of SFAS No. 157 in a market that is not active. The

adoption of this statement did not have a material impact on the

Company’s consolidated results of operations, fi nancial position

and cash fl ows.

In December 2007, the FASB issued SFAS No. 141 (revised

2007), Business Combinations (“SFAS 141R”), which replaces

SFAS 141. SFAS 141R establishes the principles and require-

ments for how an acquirer recognizes and measures in its

fi nancial statements the identifi able assets acquired, the liabilities

assumed, any noncontrolling interest in the acquiree and the

goodwill acquired. The Statement also establishes disclosure

requirements which will enable users to evaluate the nature and

fi nancial effects of business combinations. SFAS 141R is effective

for fi scal years beginning after December 15, 2008.