Air New Zealand 2013 Annual Report Download - page 24

Download and view the complete annual report

Please find page 24 of the 2013 Air New Zealand annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

|

|

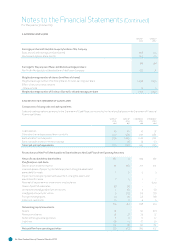

Air New Zealand Annual Financial Results

22

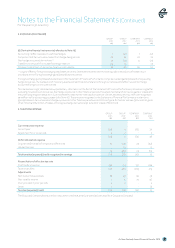

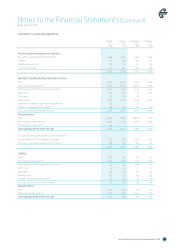

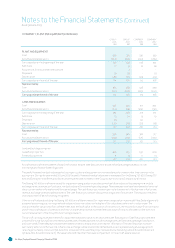

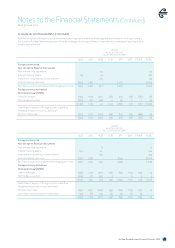

. PROPERTY, PLANT AND EQUIPMENT CONTINUED

GROUP

M

GROUP

M

COMPANY

M

COMPANY

M

PLANT AND EQUIPMENT

Cost 368 375 330 339

Accumulated depreciation (242) (253) (222) (235)

Carrying value at the beginning of the year 126 122 108 104

Additions 17 31 16 28

Acquisitions from business combinations - 2 - -

Disposals (1) (2) - (1)

Depreciation

(28) (27) (25) (23)

Carrying value at the end of the year 114 126 99 108

Represented by:

Cost 365 368 328 330

Accumulated depreciation (251) (242) (229) (222)

Carrying value at the end of the year

114 126 99 108

LAND AND BUILDINGS

Cost 346 326 317 302

Accumulated depreciation (114) (98) (104) (90)

Carrying value at the beginning of the year 232 228 213 212

Additions 13 24 13 19

Disposals (2) - (2) -

Depreciation (26) (20) (23) (18)

Carrying value at the end of the year 217 232 201 213

Represented by:

Cost 350 346 322 317

Accumulated depreciation (133) (114) (121) (104)

Carrying value at the end of the year 217 232 201 213

Land and buildings comprise:

Leasehold properties 206 219 190 200

Freehold properties 11 13 11 13

217 232 201 213

Aircra and aircra related assets of $1,916 million as at 30 June 2013 (30 June 2012: $1,923 million) are pledged as security over

borrowings and finance lease obligations.

The useful lives and residual values applied to property, plant and equipment are reviewed annually to ensure that they continue to be

appropriate. During the year ended 30 June 2013 the useful lives and residual values were reassessed for the Boeing 737-300, Boeing 767-

300 and Boeing 747-400 fleets and depreciation expense was increased in the Group by $27 million and Company by $6 million.

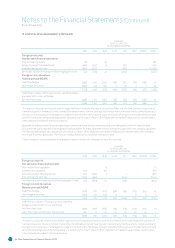

The Boeing 747-400 aircra were tested for impairment using a value in use discounted cash flow valuation. Key assumptions include

exchange rates, revenues, jet fuel costs, residual value and forecasted operating usage. These assumptions have been based on historical

data, current market information and forecasted usage. The cash flow projections are particularly sensitive to fluctuations in fuel prices,

revenue, exchange rates and sales proceeds. The cash flow projections are discounted using a rate of 9.0 percent. The valuation resulted

in an impairment of $5 million being recognised.

Other aircra values (excluding the Boeing 747-400 aircra) were tested for impairment using a value in use model. New Zealand generally

accepted accounting practice requires book values to be wrien down to the higher of fair value less costs to sell or value in use. The

indicative market valuations of aircra were less than the book value. In the opinion of the directors, the recoverable value from continued

use of the aircra as part of a network and their ultimate sale proceeds exceeded the book value of the aircra, based on the directors’

current assessment of the Group’s future trading prospects.

The aircra carrying values were tested for impairment based on a value in use discounted cash flow valuation. Cash flow projections were

prepared for 5 years using Board reviewed business plans. Key assumptions include exchange rates, jet fuel costs, passenger load factors

and route yields. These assumptions have been based on historical data and current market information. The cash flow projections are

particularly sensitive to fluctuations in fuel prices, exchange rates and economic demand and are extrapolated using an average growth

rate of approximately 2.0 percent (30 June 2012: 2.0 percent). The cash flow projections are discounted using rates of 8.0 and 10.0 percent

(30 June 2012: 8.0 and 10.0 percent). The valuations confirmed that there was no impairment to the aircra assets required.

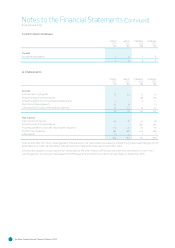

Notes to the Financial Statements (Continued)

As at 30 June 2013