Air New Zealand 2013 Annual Report Download - page 15

Download and view the complete annual report

Please find page 15 of the 2013 Air New Zealand annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

|

|

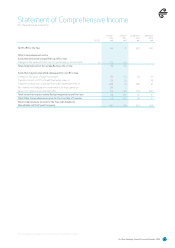

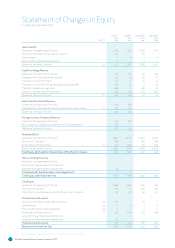

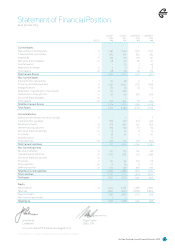

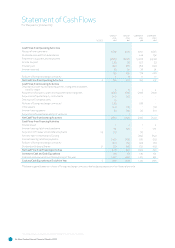

Air New Zealand Annual Financial Results 13

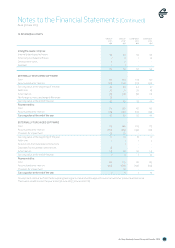

Manufacturers’ credits

The Group receives credits and other contributions from manufacturers in connection with the acquisition of certain aircra and engines.

Depending on the reason for which the amounts are received, the credits and other contributions are either recorded as a reduction to the

cost of the related aircra and engines, or offset against the associated operating expense. When the aircra are held under operating

leases, the amounts are deferred and deducted from the operating lease rentals on a straight-line basis over the period of the related

lease as deferred credits.

DEPRECIATION

Aircra

Depreciation of the aircra fleet is calculated to write down the cost of these assets on a straight line basis to an estimated residual value

over their economic lives. The aircra and related engines, simulators and spares are being depreciated on a straight line basis

as follows:

Airframe 10 – 22 years

Engines 5 – 17 years

Engine overhauls period to next overhaul

The residual values of aircra are reviewed annually by reference to external projected values.

Non-aircra

Non-aircra assets are depreciated on a straight line basis using the following estimated economic lives:

Buildings 50 – 100 years

Aircra specific plant and equipment 10 – 20 years

Non-aircra specific leasehold improvements, plant, equipment, furniture and vehicles 2 – 10 years

Gains and losses on disposal are determined by comparing proceeds with carrying amounts. These are included in the Statement of

Financial Performance.

INTANGIBLE ASSETS

Goodwill

Goodwill represents the cost of an acquisition over and above the fair value of the Group’s share of the net identifiable assets acquired.

Goodwill arising on acquisition of a subsidiary is included in intangible assets. Goodwill arising on acquisition of an associate or joint

venture is included in the carrying value of the investment in that associate or joint venture. Goodwill is tested annually for impairment

and carried at cost less accumulated impairment losses. Gains and losses on the disposal of an entity include the carrying amount of

goodwill relating to the entity sold.

Computer soware and licences

Computer soware acquired, which is not an integral part of a related hardware item, is recognised as an intangible asset. The costs

incurred internally in developing computer soware are also recognised as intangible assets where the Group has a legal right to use the

soware and the ability to obtain future economic benefits from that soware. Acquired soware licences are capitalised on the basis of

the costs incurred to acquire and bring to use the specific soware.

These assets have a finite life and are amortised on a straight-line basis over their estimated useful lives of three to six years.

Expenditure on research activities is recognised as an expense in the period in which it is incurred.

Development costs

Expenditure related to development costs which is applied to external customer products and services is recognised as an asset and

stated at cost. The assets are amortised on a straight line basis over the period of the expected benefits. All other development costs are

recognised in the Statement of Financial Performance as incurred.

IMPAIRMENT

Impairment of financial assets at amortised cost

Financial assets carried at amortised cost are assessed each reporting date for impairment. If there is objective evidence of impairment,

the difference between the asset’s carrying amount and the present value of estimated future cash flows, discounted at the financial

asset’s original effective interest rate, where appropriate, is recognised in the Statement of Financial Performance.

Statement of Accounting Policies (Continued)

For the year to 30 June 2013